Nitin Agrawal

Moneycontrol Research

Mahindra CIE, the automobile component manufacturer, posted a strong set of earnings for Q3 CY18. On a year-on-year (YoY) basis, revenue in the domestic and Europe business grew significantly. Its earnings before interest, tax, depreciation and amortisation (EBITDA) margin remained flat, despite adverse raw material prices. New orders, strong demand outlook and reasonable valuations make it a business worth considering.

Quarter snapshot

Consolidated sales grew 23.3 percent year-on-year led by a 25.9 percent and 19.5 percent growth in Europe and India businesses, respectively.

Growth in India business came on the back of higher production in its big customers such as Mahindra & Mahindra (M&M) and Tata Motors, price hike taken by the management to pass on higher commodity prices and market share gains.

Europe business grew on the back of favourable currency movement, price hikes taken to pass on raw material prices and new order wins.

Earnings before interest, tax, depreciation and amortisation (EBITDA) grew 24.7 percent and EBITDA margin expanded a meagre 16.7 bps. Margin in the Europe business contracted 35.6 bps due to adverse commodity price, lower production by major original equipment manufacturers (OEMs) and pricing pressure due to competitive intensity.

Strong domestic demand outlook

Demand in the India business is strong as seen from new orders. It received orders for gears from TBK India, stampings from Ashok Leyland and crankshafts from Hyundai. The company has also bagged new orders from Hyundai and Kia Motors, which would add to 2019 revenues. New orders will help the company gain market share gains with its clients.

Mexico continues to see strong traction

The management highlighted that Bill Forge continues to win new orders on the back of very strong demand in Mexico. The second press line that it has added to cater to a new client will commence production from January next year. In order to fulfil new orders and cater to strong demand, the company plans to add third press line in Mexico by CY18-end.

Europe to recover

In its earnings call, the management highlighted the extended production shutdown by OEMs such as Renault and VW has impacted revenue, though marginally. Now, with production in full swing, the company is expected to benefit. Overall, there is a decent demand in European market and growth is recovering gradually.

Mahindra Forgings Europe (MFE) and Metalcastello continue to grow their revenue and are expected to aid margin of its European business.

The management continues to maintain its stance that it will outperform industry growth in Europe. This is on the back of execution of new orders, ramp-up of existing orders and demand for crankshaft from the forging business.

Valuation at reasonable levelsDespite higher market volatility, the stock witnessed only a 12 percent fall from its 52-week high, indicating strength in the core business and underlying fundamentals.

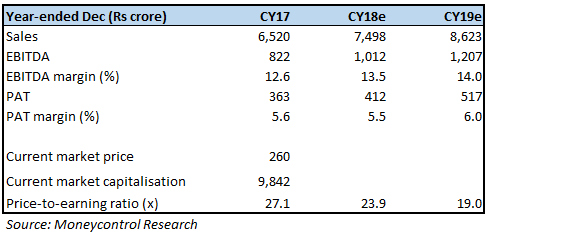

On a consolidated basis, the company is currently trading at 23.9 times and 19 times CY18 and CY19 projected earnings, respectively, which we believe are at reasonable levels and advise investors to accumulate for the long term.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.