Madhuchanda Dey

Moneycontrol Research

Highlights:

- Significant rise in slippage in the recently reported quarter

- Guiding to large slippages in the coming five quarters

- Higher provision to keep near-term earnings subdued

- Management’s long-term strategic intent reassuring

- Another 15 percent stock downside likely

-------------------------------------------------

Karur Vysya Bank (KVB, CMP: Rs 69.10, M Cap: Rs 5511 crore) once considered the 'HDFC Bank of old generation banks', had a rough ride as the corporate credit cycle weakened, resulting in formation of toxic assets, very similar to what most peer group banks had witnessed. However, when the pain seemed to be abating for the system, KVB delivered a shocker with a very high slippage (assets turning non-performing) in Q3 FY19 and guided to significant pain ahead. While the stock has corrected by over 20 percent after its result, is it time for bargain hunting or should investors still exercise caution?

The difficult Q3

KVB reported lacklustre numbers in Q3, with weak core performance – net interest income (NII) growing by 3.6 percent as interest reversal on account of high slippages impacted earnings. Growth in core fees was muted and trading gains aided in maintaining a flat pre-provision profit. Operating costs went up on account of provision for retiral benefits and after-tax profit growth declined 71 percent.

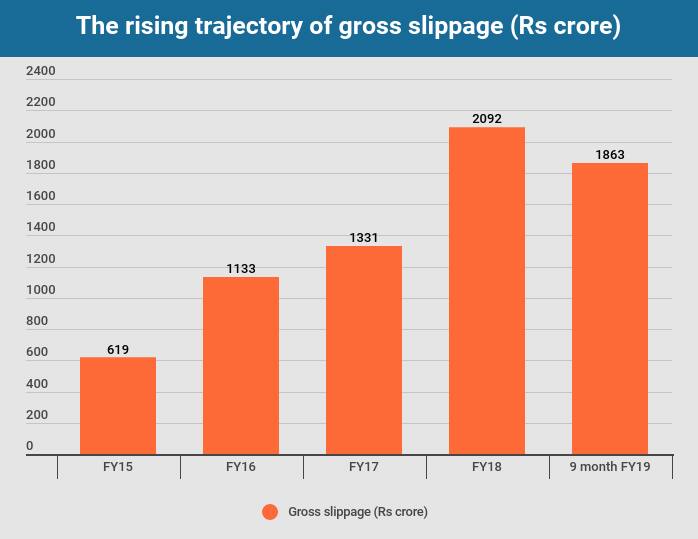

The asset quality shockerHowever, the bigger disappointment came from worsening of asset quality, with gross and net non-performing assets (NPAs) touching 8.49 percent and 4.99 percent, respectively. Slippage in the quarter gone by was exceptionally high at Rs 888 crore, thereby taking the total slippage in the first nine months of FY19 to Rs 1,863 crore. While the slippages in the quarter were dominated by corporate accounts, the commercial segment is also beginning to look shaky.

Source: Company

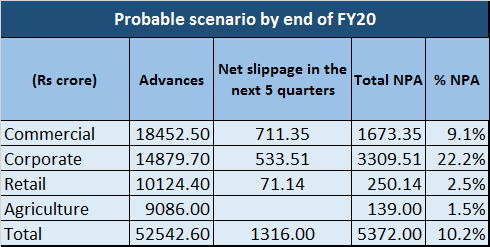

The slippage in Q3 may just be the tip of the iceberg as the bank has guided to significantly high level of slippage in the coming five quarters (till FY20-end). The management has guided to gross slippage of Rs 1,850 crore (Rs 750 crore from corporate, Rs 1,000 crore from commercial and Rs 100 crore from retail). With a decent recovery, net slippage is expected to be of the order of Rs 1,100 crore.

In addition to the identified pain, the bank expects some more from other quarters that could take the total net slippage to Rs 1,300 crore.

The moot point to take note of is the deterioration in the underlying quality of the book. Assuming that there is no further deterioration beyond what the management is indicating, even then the quality of the book is quite unnerving.

Source: Company, Moneycontrol Research

The guidance by KVB assumes importance in the context of warning signals highlighted by industry leaders like Uday Kotak, who feels that the pain in the small and medium enterprise (SME) segment can be substantial.

Impact of the mess on earnings

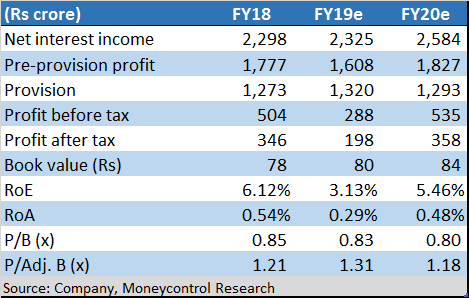

For KVB, the other area of concern is a far lower provision coverage (provision held against NPA) compared to corporate focused banks in general and peer private sector banks in particular. The provision coverage ratio at the end of December 2018 stood at 43.4 percent. With the management intending to step up the provision coverage to 60 percent by FY19-end, reported earnings will be under pressure.

Business on a slow lane

If we look at some of the other business parameters, they fail to enthuse and are unlikely to show positive surprise in the near term as the stressed asset portfolio will largely consume management bandwidth.

As per the latest reported numbers, for the quarter-ended December, KVB’s deposits and advances grew by 3.3 percent 7 percent, respectively, much lower than the system. The bank has close to 0.5 percent share of system’s advance and deposits and has been losing market share with its incremental share in advances at 0.2 percent and deposits at 0.1 percent.

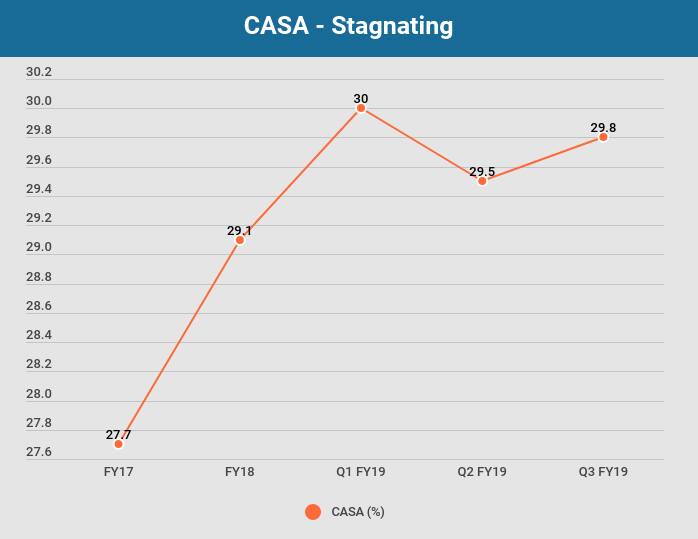

The bank has a lot of catching up to do to get its liability profile right. The share of low-cost deposits (CASA) has been hovering around the 30 percent mark, much inferior to the best in class in the market. We feel, cost of funds would be key differentiator in accruing incrementally better quality assets in a competitive landscape where everyone seems to be chasing high-rated assets.

Source: Company

In the absence of significant improvement in the cost of funds side, large baggage of bad assets restricts margin improvement.

Why investors should not write off KVB?

The initiatives on technology implementation is gathering steam and the new CEO PR Seshadri (former Citi banker) appears to be guiding the bank in the right direction, although the overt results aren’t fully visible yet.

As of now, home loan, loans against property, unsecured personal loan and working capital renewal is on the digital platform and the bank is putting commercial banking on this platform, which will enable better pricing of risk.

The bank is strengthening risk management processes and consciously reducing the ticket size of corporate loans. It is introducing new scorecard method of underwriting that will reduce the judgemental element in decision making. The effort is also to centralise key decision making.

There is no need to raise capital in the near term (CAR 14.59 percent) and with the weakening competitive landscape (thanks to the weakness from the PSU pack), there is headroom for growth.

However, the ongoing efforts of the management might bear fruit only gradually. Numbers are likely to remain uninspiring in the near term. So, while we do not rule out a better FY21, should all bad asset recognition gets complete in FY20, investors with a long-term horizon should get in only at a level where the downside looks limited.

Post correction, the stock trades at 1.2 times FY20 estimated adjusted book. Given the challenges that confront the bank, a further correction of close to 15 percent bringing the valuation to one-time FY20 estimated book cannot be ruled out. We advise investors to wait for this downside to play out.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.