Nitin Agrawal

Moneycontrol Research

Factors such as delayed festive season, floods in Kerala and increasing ownership costs on rising interest rates and fuel prices have dampened demand for the automotive segment and impacted performance of Mahindra & Mahindra (M&M). The company posted meagre topline and realisation growth and saw operating margin contract due to rising raw material (RM) prices.

The stock is worth accumulating for the long term given its strong leadership in farm equipment segment (FES), revival in rural growth, a slew of new launches and reasonable valuations.

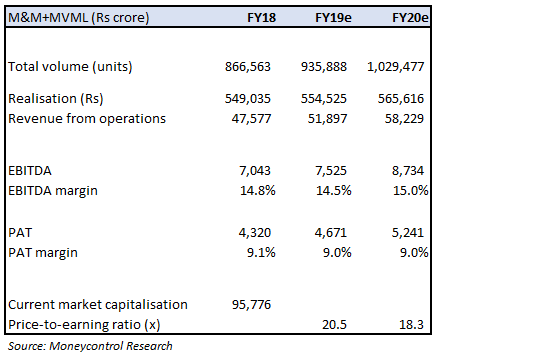

Quarter in a snapshot Revenue grew 6.4 percent year-on-year (YoY). Growth was impacted due to a 4.7 percent decline in FES volumes and subdued automotive volume growth (9.4 percent). Volume growth was impacted primarily due to multiple macro factors such as rising oil prices and interest rates and delayed festive season. Average realisation continues to be under pressure due to intensified competitive intensity.

Revenue grew 6.4 percent year-on-year (YoY). Growth was impacted due to a 4.7 percent decline in FES volumes and subdued automotive volume growth (9.4 percent). Volume growth was impacted primarily due to multiple macro factors such as rising oil prices and interest rates and delayed festive season. Average realisation continues to be under pressure due to intensified competitive intensity.

Earnings before interest, tax, depreciation and amortisation (EBITDA) margin contracted 154 basis points (100 bps = 1 percentage point) given the significant rise in RM prices and the cost involved in the launch of new models.

Following factors lend comfort

Outlook for FES positive

The company has been the market leader in tractors, with an over 40 percent share, on strong product innovation pipeline.

The management pegs FY19 industry volume growth at 12-14 percent on improving rural sentiment. It feels annual volume growth of 8-9 percent is sustainable for the industry in the long term.

M&M, being the leader, is in a sweet spot to take advantage of a growing industry. The management said it should be able to perform better than the industry on the back of its large exposure in rural and semi-urban areas.

Automotive segment seeing positive impact of GST

The auto segment has not been performing well for the past few months due to challenges on the macro front. However, with new launches, M&M continues to be on a strong footing. The commercial vehicle (CV) segment is expected to witness robust demand over the next one-to-two years given the government’s thrust on infrastructure and mining. It remains the numero uno player in the small commercial vehicle (SCV) segment, with a share of 47 percent, on the back of a wide range of offerings and would be able to capture demand accruing from industry opportunities.

Portfolio revamp is on

M&M has a portfolio of very successful products -- Scorpio and XUV500 -- in the utility vehicle (UV) segment. The response to its refresher Pulse XUV500 has also been very strong. Its recently launched Marazzo is seeing strong traction from customers and has a 6-8 weeks waiting period at present. In fact, Marazzo production is running at full capacity. For FY19, it product launch portfolio consist of: Jawa two-wheelers and electric three-wheeler (3W) Treo to be launched on November 15, Alturas G4 to be launched on November 24, S201 and intermediate CV Furio in Q4.

Focus on electric vehicles

The management continues to focus and invest heavily on EVs. It sells around 800-1,000 units of its electric 3W and expects growth for the 3W segment to be partially led by EVs. The company is also targeting fleet operators for expanding its reach.

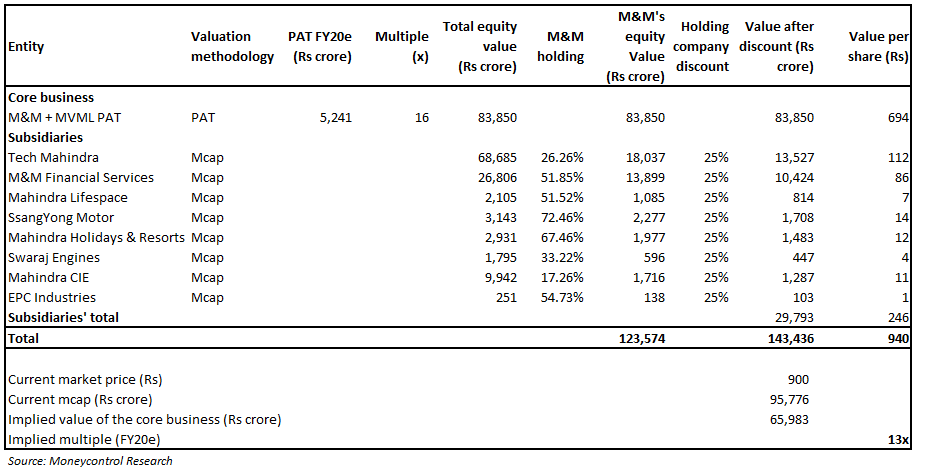

Undemanding valuationUnderperformance in the stock has rendered valuations attractive. If we follow a sum-of-the-parts (SoTP) valuation and exclude value of the subsidiaries, the core automobile business trades at close to 13 times FY20 projected earnings. The stock is trading at a steep discount to peers, which typically trade at a multiple of 17-20 times. We believe the company has enough headroom to grow on a rural recovery and product innovation. Long term value investors should accumulate M&M for the long term.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!