Neha Dave

Moneycontrol Research

Rating agency ICRA downgraded long-term credit ratings of Aspire home finance, a housing finance subsidiary (HFC) of Motilal Oswal Financial Services (MOFS). The ratings of its outstanding debt instruments including bank lines were downgraded by a notch from AA- to A+. However, it continues to enjoy a top-notch rating on its short-term paper which remains unchanged as A1+.

In an effort to reduce its dependence on the capital markets, MOFS ventured into housing finance through Aspire which focusses on affordable housing segment catering to mostly self-employed customers with an average ticket size of Rs 9 lakh. Despite having infused Rs 650 crore as capital so far, the current performance of the housing finance subsidiary continues to be weak with low return on equity (RoE) and non-meaningful contribution to the group.

However, we believe the strategic decision to enter into the housing space will yield results in the long run. The diversification will help MOFS mitigate the cyclicality in capital market-related earnings. Further, given that most of MOFS' businesses are fee-based and have limited requirement for incremental capital, the housing finance business provides an avenue to deploy excess capital for creating long-term value.

Aspire’s margins to come under pressure

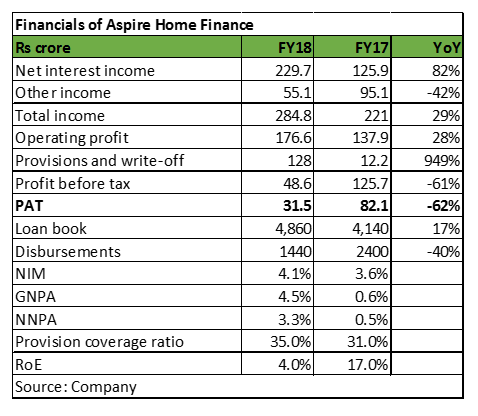

As on March 31, 2018, Aspire’s outstanding borrowing was Rs 3,940 crore. Term loans from banks constituted 46 percent of borrowings, while 54 percent came from non-convertible debentures (NCD). The lender had no short-term borrowing outstanding as on March 31.

Aspire’s cost of funds stood at 9.1 percent for FY18 which is now likely to inch up following the rating downgrade and also due to rising interest rate environment. The lender enjoys healthy net interest margins (NIM) as it operates in a relatively high yielding retail segment of self-employed customers. Its average lending rate has been stable over last four years at 13.4 percent. The improvement in net interest margins (NIM) to 4.1 percent in FY18 was mainly aided by the fall in the cost of borrowings. However, going forward, we expect NIMs to compress due to likely rise in the cost of borrowings and limited room to increase lending rates in highly competitive housing segment.

Worsening asset quality is a bigger concern

The steep deterioration in asset quality led to lender’s ratings downgrade. The lender’s gross non-performing assets (GNPA) increased sharply to 4.5 percent as at end-March 2018 as compared to 0.6 percent last year. The company also wrote off loans aggregating to Rs. 72 crore during the year. So, adjusting for the write-offs, the company’s GNPA increased to 6.3 percent as on March 31, 2018, from 4.6 percent as on December 31, 2017.

The fall in asset quality was mainly due to portfolio seasoning and the impact of external factors like demonetisation and roll out of GST. The delays in setting up of dedicated recovery and collections infrastructure further aggravated the situation.

Though the company is taking necessary corrective measures to address the challenge, the asset quality will continue to remain under pressure in H1FY19 mainly due to two reasons. First, Aspire’s loan book continues to remain relatively unseasoned. Second, there are inherent risks associated with the affordable housing segment and the limited ability of the borrowers to absorb income shocks. Overall, the industry is also witnessing a deterioration in the affordable segment.

Profitability to remain weak

As a consequence of deteriorating asset quality, a significant increase in provisions and write-offs impacted the lender’s profitability. RoE declined from 17 percent in FY17 to 4 percent in FY18.

Aspire witnessed a rapid growth in the loan book from Rs 359 crore as on March 31, 2015, to Rs 4,140 crore as on March 31, 2017. However, following the concerns on asset quality, the focus has now shifted to collections. As such, the top line will be subdued for FY19 as loan book growth is expected to moderate to 15 percent. Interest reversals due to rising NPAs would further weigh down the top line growth which along with increased provisions will restrict the profitability.

Hence, we expect FY19 to remain a year of consolidation for the lender and expect reported numbers to improve meaningfully from FY20.

Impact on MOFS’ stock

After a dream run till December 2017, the MOFS stock has corrected almost 46 percent from its 52- week high price on January 2018. The significant weakening in housing finance business was the key catalyst for the correction in stock price in addition to market factors. While asset quality concerns in housing book will continue to linger for at least next two quarters, it is important to note that the Aspire contributed only 6 percent to MOFS' profit in FY18.

Also Read: Motilal Oswal: Investors with an appetite for some volatility can accumulate for the long term.

In fact, after the correction, valuation has turned more reasonable with the stock trading at 21 times FY19 estimated earnings. We see a lot of value in MOFS’s other businesses. Expected buoyancy in the capital markets supported by the growth in the fee-based businesses such as asset and wealth management should support MOFS’ FY19 earnings. Given the franchise’s strength and future growth levers, long-term investors with an appetite for some volatility should consider the stock.

For more research articles, visit our Moneycontrol Research page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!