2018 has been a difficult year so far for equities with the midcap index falling around 12 percent year-to-date. The fall in many midcap stocks is much sharper with prices eroding over 40-50 percent. Motilal Oswal Financial Services (MOFS) is one such stock which is down 47 percent from its 52-week high. Following the collapse, should investors nibble over this stock? The answer is yes.

We deep dive to decipher the reasons for the fall and understand the path of its future profitability.

Brief historyMOFS, one of the leading capital market player, witnessed a change in its fortunes after 2014. The group’s profit almost quadrupled from Rs 140 crore in FY15 to Rs 540 crore in FY18. Strong profit growth over these years was reflected in the stock’s performance. The stock surged 5 times in three years as of December-end, generating 65 percent compounded returns (CAGR).

FY08-14 was a tough phase for MOFS as its earnings declined 6 percent CAGR due to low cash volumes and retail participation. After 2014, it profited from a cyclical recovery in the retail broking business. The company reaped benefits of structural growth in the sector by positioning itself as a diversified capital market player, not just a broking entity.

MOFS enjoys strong market position in both the retail and institutional segments of the equity broking business. It ranked among the top 5 Indian brokers in FY18 with a market share of around 2 percent in both the cash and derivative segments. The group has 9.7 lakh retail broking clients, with 3 lakh active clients across 2,000 franchisees or sub-broker outlets.

In an extremely competitive institutional segment, it has a healthy market position with empanelment from close to 676 entities. Though the group has an established track record, performance in this segment depends on its strong execution capabilities supported by a well-recognised research team.

Blended yields in the broking segment stood at 2.8 basis points in FY18. Lower share in higher yielding cash segment and falling yields in both cash and derivatives segments are key concerns of this business.

MOFS delivered its highest ever broking revenue in FY18 led by robust volume growth. The broking segment is highly volatile and future growth can be adversely impacted by rising trend of retail investors preferring mutual funds over direct equity investments. We see this risk being mitigated to some extent as it ramps up its retail distribution business.

Retail distribution witnessed strong traction in FY18 with net sales of Rs 3,000 crore and assets under management of Rs 7,500 crore. Distribution income currently contributes around 17.5 percent of total retail revenue. We see significant scope for an increase in AUMs with cross-selling opportunity to broking clients.

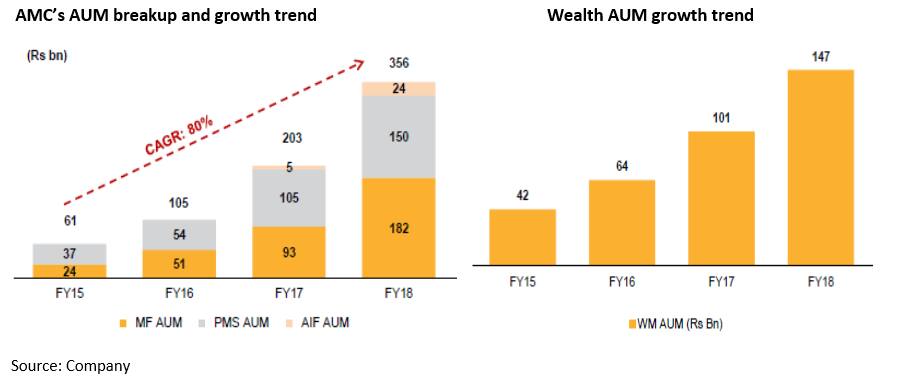

Asset and wealth businessMOFS’s fee based businesses includes asset management (AMC), wealth management and private equity. The company reported a healthy growth in the asset management segment (which includes mutual fund, portfolio management services and alternative investment fund), with AUM increasing to Rs 35,600 crore as on March 31 from Rs 20,300 crore YoY, driven by mutual fund and PMS segments. The group’s private equity assets at Rs 4,700 crore which includes three growth and three real estate funds each. The early funds have already witnessed some partial and full exits supporting earnings in FY18.

We are enthused about certain aspects of its AMC business. First, it has positioned itself as an equity specialist. Hence, its entire AUM consists of high fee earning equity assets unlike the industry which has more than 50 percent of low yielding debt and liquid assets. Second, it has diverse sourcing mix with direct channel contributing 25 percent of its AUM. Third, 51 percent of its AUM consists of non- mutual fund assets (PMS and AIF), where fees can be higher driven by performance fees.

Though the current size of MOFS’s wealth is modest with assets around Rs 14,700 crore, we see enough potential in this segment. Also, increase in the vintage of existing 118 relationship managers will help sustain growth and drive further operating leverage.

Housing finance businessIn an effort to reduce its dependence on the capital markets, in May 2014, the group ventured into housing finance through Aspire, a subsidiary of MOFS. It focusses on the affordable housing segment, catering mostly to self-employed customers with an average ticket size of Rs 9 lakh.

Aspire witnessed a rapid growth in its loan book from Rs 359 core as on March 31, 2015 to Rs 4,141 crore as on March 31, 2017. However, its asset quality has sharply deteriorated with gross non-performing assets increasing to 4.5 percent at the end of March as compared to 0.6 percent last year. Consequently, a significant increase in provisions and write-offs impacted profitability with return on equity (RoE) declining from 17 percent in FY17 to 4 percent in FY18. The fall in asset quality was due to portfolio seasoning, impact of external factors like demonetisation and challenges on the collection front. The company is taking necessary corrective measures to address the challenge.

However, asset quality performance will be under pressure for a couple of more quarters. We expect FY19 to remain a year of consolidation for housing finance and reported numbers to improve meaningfully from FY20.

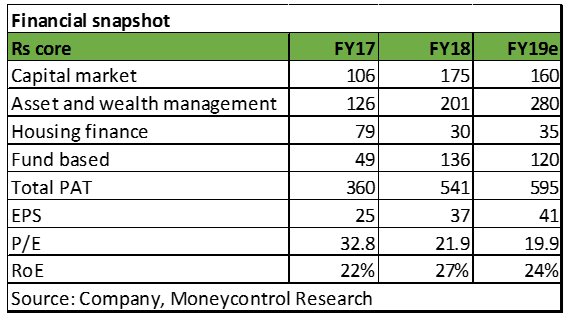

Outlook and valuationMOFS has reported strong growth in earnings in the past four years. Its earnings per share (EPS) has grown by 87 percent CAGR from FY14 to FY18, with RoE improving from 9 percent to 27% over the same period. While earnings have grown significantly, investors should be cognisant that capital market businesses are inherently volatile in nature.

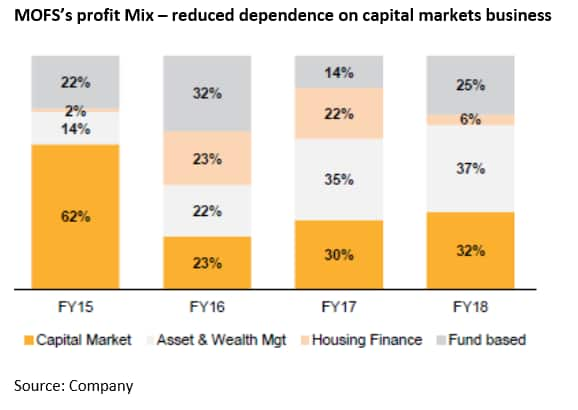

However, gradual diversification in the company’s revenues, supported by growth in fee based businesses such as asset and wealth management and foray into housing finance provides us comfort. These businesses have scaled up significantly over the last few years, with contribution from these to overall profits increasing to 68 percent in FY18 from 38 percent in FY15.

After a dream run till December last year, the stock has corrected almost 47 percent from its 52- week high in January. As such, valuation has turned more reasonable with the stock trading at 21.9 times it FY18 earnings and 19 times FY19e earnings. Deterioration in housing finance was the key catalyst for correction in the stock price in addition to market factors. We don’t see a quick pullback in the stock price as asset quality concerns in the housing book will continue to linger for at least the next two quarters. Nevertheless, given the franchise’s strength and future growth levers, long term investors with appetite for some volatility can look to accumulate the stock.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!