Ruchi Agrawal

Moneycontrol Research

Highlights:

-Above average YoY uptick in volumes

-Domestic PNG demand strong

-Price hike helps improve realisations and protect margins

-Raigarh approvals in place, fast pace development of project expected-Capex guidance revised

-------------------------------------------------

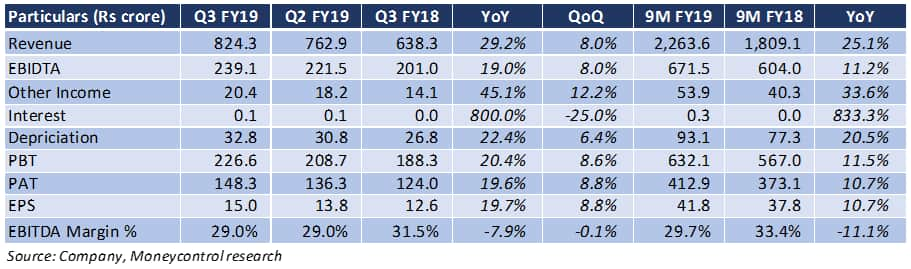

Mahanagar Gas (MGL) reported a healthy performance with a near 30 percent year-on-year (yoy) uptick in profits majorly led by improved volumes in the LNG segment and price upticks during the quarter.

Key positives

-Revenue grew 30 percent YoY on the back of improved volumes and realisations. Volumes saw an above average growth of 8 percent YoY with Domestic PNG volumes up 13 percent yoy, CNG up 8 percent YoY and Industrial plus commercial up 2.5 percent YoY.

-Gross margins improved on the back of price upticks in the CNG and Domestic consumer category in October 2018. Higher alternate fuel prices worked in favour of the company in taking price upticks.

-Strong gross margins helped to nullify some impact of higher operating expenses

-The company has received approvals from development authorities for laying down the pipelines in Raigarh and the project is now progressing as per the catch up development plan. With this the company has revised upwards its capex guidance for the year from Rs 300 crore to Rs 375 crore.

Key Negatives

-Upward revision of natural gas prices applicable from October 2018 resulted in higher cost of materials for the company.

-Ola and Uber strike in Mumbai during the quarter ate away a portion of the volumes uptick. It is however expected to normalise in Q4.

-Planned maintenance activity for Q3 and Q4 led to higher other expense charge.

Other notes

-There has been a noticeable decline in the BEST bus fleet over the last few months with which the volumes for this segment are now reducing. However there has been a parallel uptick in the demand from rapidly rising auto rickshaws (relaxed permit norms) where CNG is compulsory. Taxi aggregator companies like Ola and Uber are also contributing to volumes.

-The management highlighted that there is usually a one month lag in passing on market prices in the industrial segment.

-Despite an uptick in the performance the management remained conservative and has stuck to old guidance of a 5-6 percent growth in the year.

Outlook

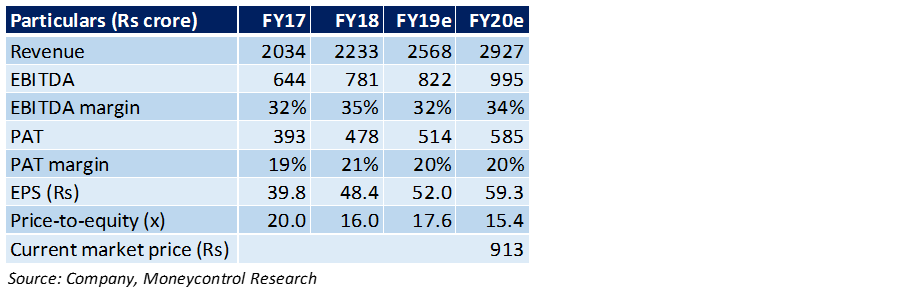

MGL has displayed a strong performance in the last few months and the stock has seen an uptick of 21 percent from its 52 week lows, but is still 19 percent below its 52 week high. MGL is now trading at the 2020e PE of 15.4x. It is priced at 4.3 times its book value.

We expect the good performance to continue with rising demand and deeper penetration in existing geographies.

The company is now witnessing a strong uptick in volumes. With new CNG stations planned for the current and upcoming year, we expect the volume growth to remain healthy.

The company is submitting bids in the 10th round and any allotment of new gas would be additional growth driver for the future.

While there is some probability of limited pricing power in coming months given the upcoming general elections, the recent correction in crude prices would keep the input cost side under control.

With the fundamental growth story intact, and a sector outlook positive, we believe in the long-term growth journey of this company.

For more research articles, visit our Moneycontrol Research Page.

(Moneycontrol Research analysts do not hold positions in the companies discussed here)

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.