Sachin PalMoneycontrol Research

Building materials players Everest Industries and Visaka Industries reported double-digit volume and topline growth in the second quarter of FY19. While the profitability of the former was boosted by a strong performance on the operational front, rising cost pressures hampered the margins of the latter.

Industry reforms and government policies have had a positive impact on the organised building material players. We look at the quarterly performance of these companies to understand the sector dynamics and the way forward.

Everest Industries

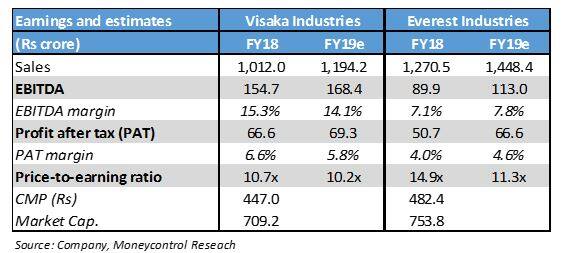

Revenues for the quarter increased 21 percent year-on-year (YoY) to Rs 313 crores. Operating profits increased from Rs 12 crores in Q2FY18 to Rs 18 crores in Q2FY19, a growth of 53 percent YoY. Profit after tax (PAT) nearly doubled to Rs 9 crores as a reduction in interest expenses and depreciation offset the higher tax outgo and lower other income.

Healthy growth across both its business lines resulted in a strong quarterly performance for the overall business. Building products segment witnessed a volume growth of 19 percent YoY on the back of rising demand for fibre-cement sheets and boards & panels. This was, however, offset by a slight dip in the realisation (down 3 percent YoY). Margins for the segment came in better as the company benefitted from stable raw material prices (mainly cement). Revenues of Steel building segment were aided by 16 percent increase in sales volumes and 11 percent rise in realisations. Lower steel prices in the quarter’s order book boosted the operational profits. However, the margins in the segment could witness some moderation on account of continuous rise in steel prices.

The company continues to expand its geographic footprint by increasing its distribution and dealer network. Everest continues to improvise its portfolio offering through the launch of new products. Everest Super, coloured waterproof roofing sheets launched earlier this year, is gaining traction among customers. On the cost front, the company continues to focus on internal business efficiencies through better working capital management and debt reduction.

Visaka Industries

Visaka Industries reported a strong growth in Q2FY19 revenues driven by healthy growth across both its business segments. Margins, however, declined as the import of raw materials kept the input costs at elevated levels.

Revenues increased 25 percent YoY to Rs 251 crores. Operating profit was flat at Rs 34 crore as the margins declined by over 350 basis points (bps). Profit after tax remained at the same levels as last year.

The revenues for building products segment grew 13 percent YoY primarily driven 11 percent increase in sales volumes. The price hikes undertaken in recent quarters also supported the topline. Despite the higher topline, the continuous rise in pulp prices (constituting around 40-45 percent of the raw material costs) adversely impacted the profitability.

Synthetic yarn segment continues to benefit from the cotton upcycle. Improved volumes, as well as realisations, boosted the performance of this segment. Going forward, the management expects the yarn division to witness double-digit volume growth in FY19 and margins to improve in a favourable demand environment.

The company is nearing the completion of its capex cycle and expects the new products to aid revenues from the second half of this fiscal year. The trial runs of its recent set-up roofing product ATUM (integrated solar panel with a cement base) plant have been successfully completed and the commercial production has started at the end of Q2. The new V-Boards plant (capacity 50,000 tons) at Jhajjar (Haryana) is also expected to come on-stream by Q3 FY19.

Outlook and recommendation

The performance of the business has benefitted from the stabilisation in industrial demand post the introduction of Goods and Services Tax (GST) last year. The demand in the first half of this fiscal year has also been boosted by a pick-up in the execution of infrastructure projects.

Visaka Industries is nearing the completion of its capex phase and the new, as well as existing capacities, provide the company with sufficient headroom to capture the growth in the building materials industry. The performance of it recently launched roofing product ATUM needs to be monitored closely. New product launches along with recovery in the yarn business should help the company post an earnings per share of Rs 48-50 for this financial year.

Everest Industries is working on value-added products to improve its margins and also focusing on brand development through marketing activities. The company is also looking to optimise its working capital and increase business efficiencies to offset the inflationary cost pressures. Overall, the management has guided to a topline growth of 20 percent on the back of a healthy order book which needs to be executed over the next 12-18 months.

From a valuation standpoint, Visaka trades at a discount to Everest due to the presence of cyclical yarn business in its portfolio. Everest remains our preferred pick among the two companies as the company is expected to grow faster than its peer.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.