Highlights

- Cement volumes up 14 percent YoY

- Margins improved despite subdued realisations

- Acquisition of Murli Industries to complete by Dec 2020

- Capacity expansion remains on track- Trading at 8.9 times FY20 estimated EV/EBITDA

-------------------------------------------------

Dalmia Bharat, India’s fourth-largest cement maker, delivered strong financial results in the December quarter. Volume-led top line growth and margin expansion gave a fillip to the operational performance. Its market share also improved as volumes grew considerably faster than those of the industry.

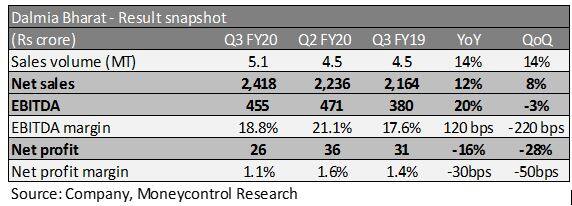

Key result highlights

Dalmia Bharat’s quarterly revenues rose 12 percent year-on-year (YoY) to Rs 2,418 crore on the back of 14 percent growth in cement volumes. However, subdued realisations (down 2 percent YoY) across its key operating markets had an adverse impact on top line. Decline in slag prices supported gross margins. Earnings before interest, taxes, depreciation and amortisation (EBITDA) margin got into shape as it improved 120 bps YoY to Rs 455 crore.

Dalmia’s strong volume play got a helping hand from the ramp-up of Kalyanpur Cements and robust demand across eastern markets. Persistent weakness in South India, mainly stalled projects in Andhra Pradesh, hurt cement offtake as well realisations.

Increase in EBITDA per tonne to Rs 892 was driven by declining cost pressures. Reduction in power and fuel costs and employee expenses resulted in 4 percent savings on the cost front.

The limestone mines and GST incentives of Murli Industries have been restored and Dalmia expects to complete the acquisition by December 2020. The upgradation of Murli Industries, having 3 million tonnes of capacity, will diversify Dalmia’s presence in the western market. To further strengthen its domestic footprint, the company is undertaking 8 million tonne capacity expansion in eastern India (across Bihar, Bengal and Odisha). These plants will be commissioned in phases during FY21 and FY22.

The capital expenditure for first nine months of FY20 stood at nearly Rs 1,000 crore, which was primarily directed towards capacity addition in the eastern market. For FY21, the company expects a capex of Rs 750-800 crore for completion of these investment projects. In addition, there will be a small capex (Rs 100-150 crore) for maintenance purposes.

During April-December of FY20, the company has repaid Rs 620 crore of debt through internal cash accruals. The balance sheet continues to build up and the net debt/EBITDA ratio reduced to 1.32x at the end of the December quarter. The leverage is expected to remain at current levels as the capacity expansion will be funded through a mix of debt and internal accruals.

Outlook and Recommendation

The company has churned out strong operational metrics in the quarter gone by. The uptick in volumes was quite impressive against a weak industrial backdrop. While cement demand has come off marginally in FY20, the management is hopeful of a demand recovery and expects volumes to grow on the back of infrastructure spending in eastern and north eastern markets. Softening pet coke and oil prices should lend support to margins.

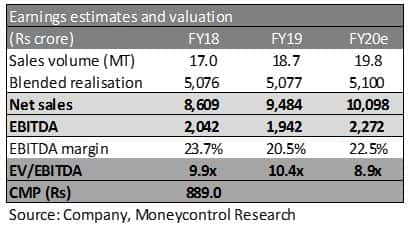

Dalmia continues to turn out quarterly numbers that show stability and has consistently outperformed larger peers both on the volumes as well as margin front. The current capacity utilisation levels of 70-75 percent provide sufficient headroom to capture incremental market demand. The valuations (8.9 times FY20 estimated EV/EBITDA) are at a discount to sector leaders and the stock appears a promising pick for investors having a long-term horizon.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!