Sachin PalMoneycontrol Research

Sanitaryware companies reported a decent volume and topline growth in a challenging FY18 as the sector witnessed multiple disruptions throughout the year. Rising cost pressures hampered the margins across industry. Despite muted performance, the players remain optimistic on demand pick-up in FY19 as industry reforms and government policies should have a positive impact on the organised players. We look at the performance of market leaders in this sector — Cera Sanitaryware and HSIL to understand the sector dynamics and the way forward.

Cera Sanitaryware

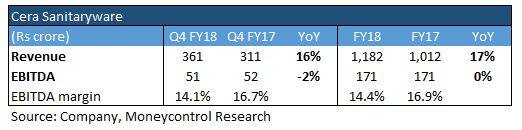

Revenue for the quarter increased 16 percent year-on-year to Rs 361 crore. Operating margins contracted on the back of higher power & fuel costs. The revenue growth was driven by strong performance of tiles and faucet segments.

For the full year, revenues increased 17 percent to Rs 1,182 crores but the EBITDA (earnings before interest, tax, depreciation and amortization) remained flat amid rising cost pressures.

Rising raw material prices and input costs are impacting the margins across the industry. Gas is an important constituent of manufacturing process for Cera and constitutes around 18-20 percent of the total cost basket. The prices of gas have increased from Rs 15 per cubic meter to Rs 18.5 per cubic meter. Increase in prices of other raw materials such as brass (used in faucets) is also putting pressure on margins.

The usual price hikes in FY18 were skipped on account of industry and market disruptions. However, the company has increased the prices in the month of May-June 2018 to mitigate cost pressures.

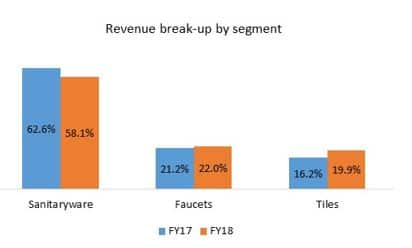

On a segmental basis, the sanitaryware revenues grew around 8 percent, faucets revenues grew by 22 percent and tiles revenues jumped 44 percent on account of low base. Cera is a leader in sanitaryware market with a share of around 23-24 percent, while that in faucet, the share stands at around 4 percent. Its share in the tiles segment is negligible as it contributes a small portion to revenue.

To further strengthen its market presence, Cera plans to expand its dealer network by 10 percent per annum. Currently, it has around 15,000 dealers across the country.

The company continues to focus on product premiumisation and incurred an advertising spend around 4 percent of sales in FY18 for sales and branding. It expects to maintain the same levels going forward. In March 2018, the company unveiled a new brand “Senator” offering a premium range of sanitaryware, faucets, wellness and mirrors.

Cera expects 15-18% revenue growth in FY19 led by double digit growth in faucets and tiles segments. Growth in faucets will be higher due to shorter replacement cycle. Sanitaryware is expected grow at high single digits. Management has guided to 100-150 bps margin improvement for FY19 on account of product premiumisation and price hikes.

HSIL (Hindustan Sanitaryware & Industries)

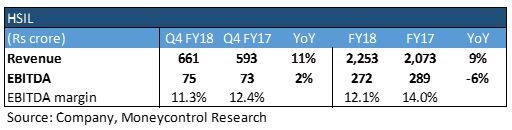

HSIL, vastly recognised by its brand hindware, reported 11 percent year-on-year (YoY) growth in revenue to Rs 661 crores. EBITDA remained flat as the margins declined in an inflationary cost environment. For the full year, HSIL posted a topline growth of 9 percent and 6 percent decline in operating profits.

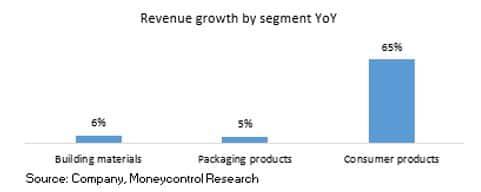

On a segmental basis, the building products segment (sanitaryware, faucets, tiles etc.) and packaging products (recyclable glass) grew at mid-single digits. The consumer products segment gained strong market traction and witnessed a supernormal growth rate in FY18. HSIL offers premium home interiors & solutions in the consumer products segment through its retail chain – EVOK. The company is expanding further retail presence by expanding its retail footprint in Tier I & Tier II cities through franchise route.

On a segmental basis, the building products segment (sanitaryware, faucets, tiles etc.) and packaging products (recyclable glass) grew at mid-single digits. The consumer products segment gained strong market traction and witnessed a supernormal growth rate in FY18. HSIL offers premium home interiors & solutions in the consumer products segment through its retail chain – EVOK. The company is expanding further retail presence by expanding its retail footprint in Tier I & Tier II cities through franchise route.

HSIL, in an effort to offer integrated home building solutions to its customers has forayed into the household plumbing pipes segment with the inauguration of their 160-crore 30,000 metric tonnes pipe manufacturing facility in Telangana. The manufacturing plant was commissioned in January and the company is undertaking trial-runs before market entry.

HSIL, in an effort to offer integrated home building solutions to its customers has forayed into the household plumbing pipes segment with the inauguration of their 160-crore 30,000 metric tonnes pipe manufacturing facility in Telangana. The manufacturing plant was commissioned in January and the company is undertaking trial-runs before market entry.

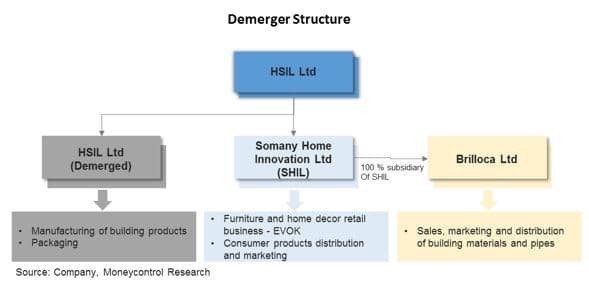

In order to have a sharper focus on the different business segments, HSIL is demerging the current business of the company into three separate legal entities. The consumer products, distribution and marketing undertaking of the company along with the retail chain EVOK will be demerged into Somany Home Innovation Limited (SHIL) – which will be listed on both the stock exchanges (NSE and BSE). The Distribution and Marketing function of building products is being demerged into ‘Brilloca Limited’, will operate as a wholly owned subsidiary of SHIL. The demerger approval is pending with the regulatory authorities and the process is expected to complete by the end of this calendar year.

Going forward, the management expects an overall revenue growth of 14-15 percent in the current fiscal year. It expects the growth momentum in consumer products segment to continue in FY19 and anticipates 10-12 percent revenue growth across other segments. Besides, there will be incremental revenues from the Pipe segment.

Recommendation

In the recent past, the growth in building material products has been subdued due to sluggish real estate activities. FY18 in particular turned out to be a challenging year as the sector was impacted by a number of factors including demonetisation, roll out of the Goods & Service Tax, and implementation of RERA (Real Estate Regulatory Authority). The sectoral outlook for FY19 looks positive as revival in new construction activity (post the implementation of RERA) is expected to spur the demand for building products. These companies will also benefit from Housing for All (60 million new houses by 2022) and Smart City Mission (development of 100 smart cities) projects initiated by the government.

We remain optimistic on the long-term prospects of both Cera and HSIL as they enjoy market leadership position in the sanitaryware segment. Cera would be our preferred pick between the two names as the company’s superior operational execution gets reflected through its margins, high return ratios and cash-rich balance sheet. We, therefore, advise long-term investors to accumulate this stock.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.