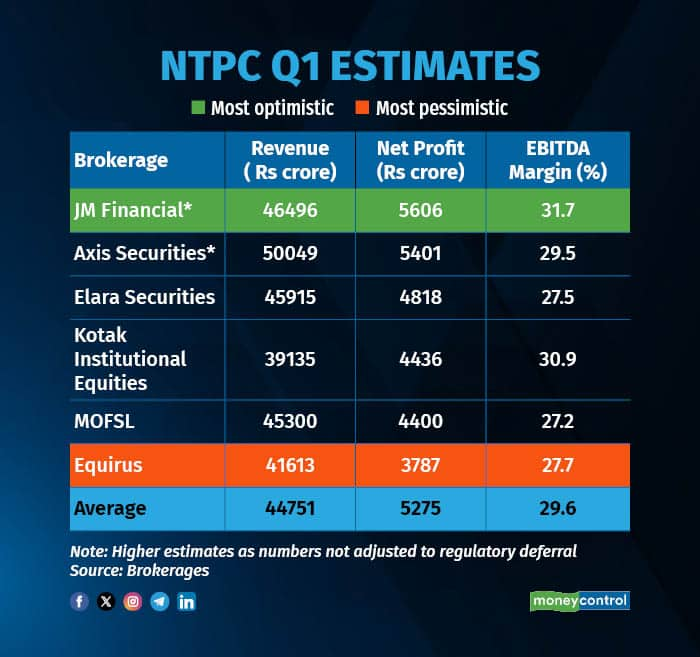

NTPC is expected to report a mixed set of numbers for the first quarter of FY26 on July 29 as analysts flag weakening demand, generation slowdown, and rising interest costs. While these factors are likely to weigh on profitability, continued capacity additions and regulated returns offer long-term strength. The power major is expected to post a nearly 1.3 percent year-on-year (YoY) growth in revenue to Rs 44,751 crore, compared to Rs 44.192 crore in Q1FY25.

A Moneycontrol poll of six brokerages estimates that net profit is projected to rise by nearly 20 percent YoY to Rs 4,741 crore, up from Rs 5,275 crore in the same quarter last year. The higher number is due to estimates by JM Financial and Axis Securities where net profit numbers are not adjusted basis regulatory deferral movement. Regulatory deferrals arise from the cost-plus regulated model under which NTPC operates. Under this framework, certain income or expenses (for example fuel costs, interest, tax) are passed through to consumers, but with a time lag.

Operating performance is also expected to improve, with EBITDA margins estimated to expand to 29.1 percent, compared to 27.0 percent in Q1FY25.

What will drive the numbers?

Weak demand and power generation

A softer summer and early onset of the monsoon led to a decline in electricity demand across the country, affecting coal-based power generation volumes. Kotak Institutional Equities expects NTPC’s generation to fall by 12 percent YoY in Q1FY26, citing subdued demand. Axis Securities also projects a decline in generation due to lower power offtake during the quarter. Equirus adds that all-India coal generation declined by 7 percent YoY, and estimates a 5 percent revenue decline for NTPC as a result of the weak power demand.

Despite lower generation, some brokerages also estimate that NTPC is likely to report modest revenue growth on a YoY basis, aided by better tariffs and incremental capacity. Motilal Oswal projects a 2 percent rise in standalone revenue to Rs 45,300 crore. Axis Securities expects revenue to remain stable sequentially, supported by tariff improvements. However, Equirus remains cautious, estimating a 5 percent decline in revenue due to demand-related pressures. While revenue trends remain subdued, NTPC’s operating profitability is expected to hold steady. Axis Securities forecasts YoY growth in EBITDA, primarily driven by marginal revenue growth. EBITDA margins are expected to remain stable, but not strong enough to offset the rising interest burden on the bottom line.

High interest costs

Rising borrowing costs are expected to be a key drag on NTPC’s profitability this quarter. Axis Securities forecasts a decline in profit after tax (PAT), both year-on-year and sequentially, driven by higher interest expenses and lower other income compared to the previous quarter. Kotak also expects a modest decline in PAT, pointing to the absence of prior-period sales that had supported the base quarter.

Capacity expansion

A key positive in the quarter is NTPC’s strong pace of capacity addition. The company added approximately 2 gigawatts in Q1FY26, reinforcing its expansion strategy. According to Elara Capital, this includes 660 megawatts each from Unit 3 of North Karanpura and Barh thermal plants. Equirus estimates total additions of around 2.2 gigawatts (GW), of which roughly 1.3 GW came from thermal sources and the remainder from renewables. This expansion is expected to support future earnings, especially as new assets begin contributing to revenue. NTPC also continues to execute a large and diversified project pipeline across thermal, hydro, and renewable segments. Elara reports that the company currently has 33.7 GW of capacity under construction, comprising 16.9 GW of thermal, 2.2 GW of hydro, and 14.6 GW of renewables. Additionally, the company received investment approval for 8 GW of new thermal projects, valued at Rs 1 lakh crore, indicating a strong long-term growth trajectory.

Regulated equity growth

Even as short-term demand and cost pressures weigh on profitability, NTPC’s regulated business model ensures earnings stability. Regulated equity stood at Rs 90,900 crore on a standalone basis and Rs 1.087 lakh crore on a consolidated basis, according to Elara. The assured return on these regulated assets helps cushion the impact of market volatility and supports consistent profitability.

What analysts will be watching out for:

Analysts will closely watch for updates on the ramp-up of renewable capacity, progress on thermal project commissioning, coal supply and PLF (plant load factor) trends, and the company’s outlook on demand recovery.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.