")

Non-banking financial companies (NBFCs) that sell gold loans are facing the heat from bigger banks, who have been pushing these loans aggressively since the pandemic.

This is particularly reflected in Muthoot Finance, which gets 90% of its assets under management (AUM) from gold loans. Quarter on quarter, its AUM has shrunk to Rs 562 billion from Rs 575 billion, and PAT has dropped to Rs 802 crore from Rs 960 crore.

After the Q1FY23 results were announced, the NBFC’s stock fell by nearly 15%.

During the pandemic, faced with lower incomes, job losses and banks who were hesitant to extend loans, people leaned heavily on their gold holdings to raise money. In fact, at the close of the first year of the pandemic in March 2021, the value of gold loans had gone up by 82% year on year, according to RBI data. Two other factors contributed to this rush as well.

One, when India was battling with the first wave of Covid-19 infections (roughly April to October 2020), gold prices shot up, which meant people could get more per unit holding. Two, in August 2020, the RBI raised the loan-to-value ratio to 90% from the previous 75%, an allowance that was to hold till March 31, 2021.

This started a pricing war with banks cutting their rates to half of NBFCs’ rates by Q3FY22. To counter this blitz, Muthoot announced teaser loans between December 2021 and March 2022, with interest rates as low as even 0.57% per month.

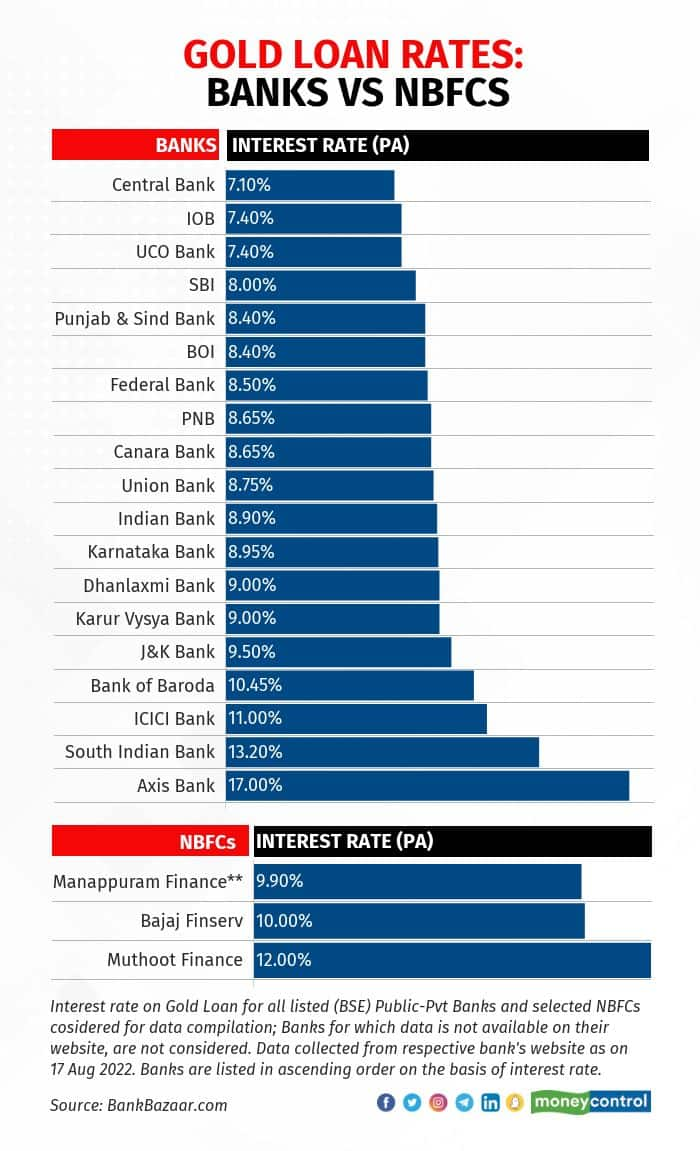

Rates charged by most banks continue to be lower than what the NBFCs charge.

Graphic: Upnesh Raval

Graphic: Upnesh Raval

Mohan K, Senior Vice President and Head of Agri Micro & Rural Banking at Federal Bank, said that everyone started pushing gold loans during the pandemic because the other lines of businesses had dulled. The Federal Bank, which has always been bullish on gold loans, saw a 70% rise in sales of the product in FY21; in FY20, it was around 28% (also because of rising gold prices) and in FY19, it was around 20%. “Public sector banks have never been focussed on gold loans and they weren’t in FY21 either, but that changed in FY22, when they started pushing gold loans aggressively. They gained a lot of the incremental business,” he said.

Also, with many mergers between south and north India banks, there was a transfer of cultures that happened. “South Indian banks have been traditionally more focussed on these loans. After the mergers, that outlook towards these products was passed on to the other geographies as well,” said Mohan.

End of an era?

Will banks disrupt the gold-loan market and unseat NBFCs then?

Not anytime soon.

According to Jinay Gala, Associate Director at India Ratings and Research, banks entering into the gold loan segment will only lead to an expansion of the market. “They won’t pose a challenge to NBFCs because the segments they cater to are different,” he said. There is a huge unorganised market (60-65% of the total gold-loan market) yet to be tapped and banks don’t cater to the customers that NBFCs do.

Also, there has been a change in mindset, with an increasing number of people willing to pledge gold to get working capital.

Gold prices were stagnating in FY2022 and teaser rates were introduced in the second half of that year. According to Gala, the lower-rates were NBFC’s way of generating growth in the face of stagnating prices, by trying to break into the higher-end of the market that banks usually cater to. Higher gold prices and customer additions are what drives growth in these NBFCs’ loan book, he said. “Going after the banks’ customer base gives the NBFCs a higher loan-book growth but it doesn’t deliver higher margins considering their cost of funds,” he added.

Mohan too believes that NBFCs’ teaser rates were aimed to break into the banks’ customer base, and added that it may not have been the best decision. “Teaser rates work usually only with high-value loans because with smaller-ticket loans, the borrowers don’t care so much about the rates, they care more about convenience and speed. They usually borrow for a month or two, and a higher interest rate (on a smaller amount) does not make much difference on the outgo,” he said.

“But, larger-ticket sizes are extremely sensitive to interest rates. So if the teaser rates are withdrawn, NBFCs will find it hard to move these customers to the higher rates,” he said.

That said, Mohan thinks that this was just a temporary setback to NBFCs and that, if banks continue to be aggressive in this segment, then NBFCs may see a slower rate of expansion for a year or two. “NBFCs will continue to be in business, and see growth with expansion, adding more branches. They cannot be done away with because of the convenience they provide to customers,” he said.

Also read: Can you get a gold-loan delivered to your doorstep?

Yes, banks did lower their ticket sizes to widen their customer base, but India Ratings’ Gala believes that it could be a passing trend because the banks would need significantly higher operating power to compete with NBFCs, with more branches selling the product and more focus on the product line. NBFCs single-product focus will be hard to beat, he said.

Mohan too said that, with the pandemic receding and economy back to normal, banks will have to focus on multiple products and NBFCs may be able to regain lost ground on that.

Yield recovery

The pricing war seems to be ending and therefore yields should recover soon.

“NBFCs are now phasing out their teaser-loan rates and are moving back into their own segments,” said Gala.

An ICICI Securities report, released on August 13, too stated that schemes with lower interest rates seem to have been withdrawn industry-wide, going by gold-loan companies’ commentary. The brokerage, which has given a ‘buy’ call on Muthoot, indicated in its report that the yields are likely to bottom out with the ending of teaser loans and NBFCs moving to higher rates. They have cut yield estimates for FY23 to 18% from 18.5%, but have maintained those for FY24 at 19%. Yield in FY22 was around 20%. “While teaser schemes enabled the company to acquire new high-value customers, it focused on migrating such teaser loans to higher-rate schemes during Q1FY23, which it successfully completed,” the analysts wrote.

The NBFC is also set to add 150 new branches, which brokerage’s analysts expect will act as an “additional growth lever”. “It takes some time for new branches to mature; however, on reaching the existing average branch level productivity, it could lead to ~3% yearly gold AUM growth,” they wrote.

Certain brokerages have pointed to the challenge posed by new fintechs, but Gala does not see much disruption from these startups. “They are largely functioning as loan originators for banks and NBFCs. To become full-fledged lenders, source of liability is key and you need online and offline presence,” he said.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.