As the benchmark indices recovered in the past few months from March lows, broader market also participated in the rally on improving economic data points.

The declining COVID-19 infections, progress on vaccine front, improving quarterly earnings along with FII inflow aided market sentiment.

Nifty50 has surged 57 percent from March 23 low, while the Nifty Midcap index went up 55 percent and Smallcap jumped 75 percent.

But in last one month, the broader market has had a tad bit of underperformance compared to frontliners as the Nifty50 gained over 10 percent against 6-7 percent gains reported by Midcap and Smallcap indices each.

Experts feel as the economic recovery continues in coming months, the broader markets will outperform over equity benchmarks.

"Our case for two-year rolling returns indicate that the market has turned in favour of small and mid-cap stocks which are more reasonably valued and offer greater upside potential," Neeraj Chadawar, Head of Quantitative Equity Research at Axis Securities told Moneycontrol.

He believes that market volatility is likely to provide good opportunities for Midcaps and Small caps.

"The recent spate of IPOs and their success clearly indicates that there is an appetite for mid and small-cap stocks. Quality as an investment style is more likely to outperform over the medium term. We are overweight quality in our allocation strategy at this juncture," he said.

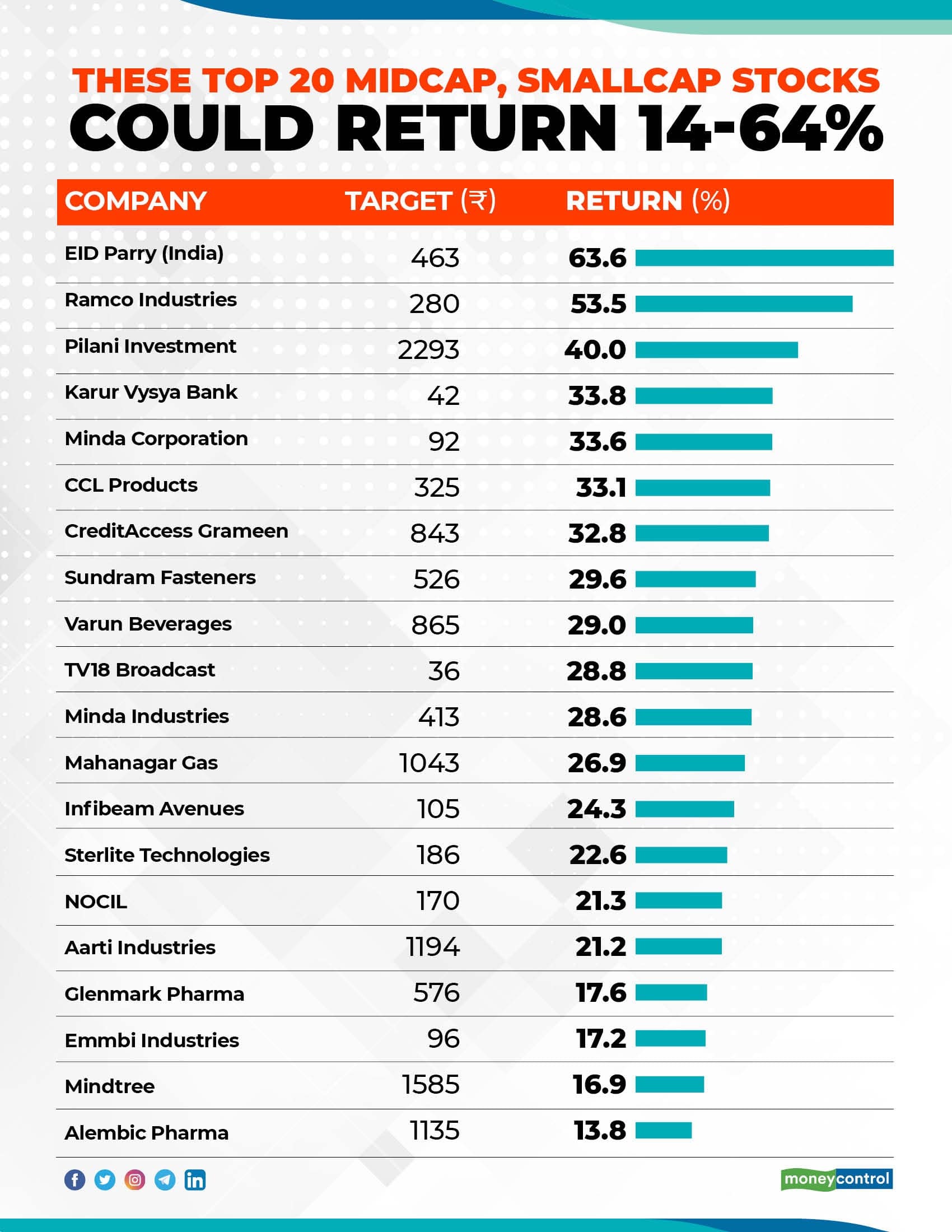

Here is a list of 20 midcap and smallcap stocks that could give 14-64 percent returns:

Brokerage: Axis Securities

While, a weak H1FY21 is likely to drag the overall FY21performance, we expect company to report improvement in the overall business from H2FY21 (aided by unlock driven improving demand in replacement tyre segment) with a sharp rebound in volumes observed in FY22 on the back of new capacity commercialization, economic growth bouncing back to normalcy and a low base. Further, a positive outcome on ADD levy and a structural opportunity to play as a dependable non-Chinese player augurs well for NOCILs long term prospects," said Axis Securities which expect NOCIL to register Revenues/Earnings CAGR of 20 percent/24 percent respectively over FY20-23.

We expect VBL to register Revenues/Earnings CAGR of 11 percent/29 percent respectively over CY19-22E. This growth will be driven by 1) consolidation in newly acquired territories, 2) distribution led market share gains, 3) cost efficiencies and margin tailwinds (cost rationalization and benign RM) should support EBITDA Margin in CY20E despite weak operating leverage. At CMP, stock trades at 10x EV/EBITDA on CY22E basis versus its 3-year mean of 14x EV/EBITDA.

We believe CCLP is well placed to deliver steady earnings over medium term given 1) expertise in customized blends & cost efficient business model, 2) long standing client relationships (around 50 percent revenue contribution from brand owners) 3) largest exporter of instant coffee in India 4) presence in Vietnam- world’s largest Robusta growing country 5) capacity additions in value added products (FDC & small packs) and 6) steadily improving branded retail business.

We are bullish on MNDA's ability to comprehensively beat industry performance by 1) leveraging the broader vehicular trends of industry like EV, premiumization, automation 2) strategic inorganic acquisition to enhance product offering and gain market share 3) maintaining balance sheet discipline and maintain optimal leverage, 4) investing in R&D to bring technological change 5) tap on its deep rooted relationship with OEM’s to increase kit value.

Given its success in developing import substitution products, it would be able to capture the business opportunities offered by the ‘Atma-nirbhar Bharat’ move in auto sector. New product lines to aid margin and growth.

Management has initiated strong cost control measures like reducing the subcontractors, better service mix and higher execution which will help to gain long term sustainable operating margins. Management is confident in gaining the momentum and has worked efficiently with zero productivity loss. While traction is expected in Capital good and Digital initiatives remained strong, HiTech and automation is expected to gain pace post COVID-19. However company sees some near-term challenge in terms of softness in revenue growth and pressure on Q1 operating margin.

Brokerage: KR Choksey

We are optimistic of company’s growth prospects on the back of new product introductions in the US, new products filed from recently commercialized Aleor JV, and improvement in the revenue mix with contribution from general and onco injectables. Moreover, one-time opportunities in the sartans in short-term (with a portfolio of 15 ANDAs) & company’s low base in the US (and being revised to $70 million from $50 million earlier) gives earning visibility.

We continue to remain positive on AIL in the light of greater tailwinds as against relatively few challenges (China raw material sourcing, COVID related disruption etc). The company’s capex plans for both its segments, well-established backward integration facilities, focus on rising share of high-value products shows strong earnings visibility over the next 2-3 years. We estimate AIL to grow its revenues at a CAGR of 19.4 percent over FY20-22E.

Measures like focus on raising funds for innovation subsidiary ICHNOS (to be completed in the 2HFY21), lower R&D spending going forward, control other costs bodes well for the company. With these measures, company will be focusing on reducing its debts & improve profitability & margins.

We expect Glenmark’s topline/bottomline to grow at 7.6 percent/22.8 percent over FY21/22. The shares of Glenmark are currently trading at an attractive valuation of 14.8x/12.5x PE on FY21/22E earnings.

CreditAccess Grameen is a leading NBFC MFI offering credit to its micro borrower base of 40.11 lakh across 14 states and an Union Territory. Gross Loan Portfolio (GLP) of Rs 11,720 crore has grown by 53.9 percent YoY. In our opinion, company's major business is in rural (82 percent of rural borrowers); and hence it has a wider scope to get back to normalcy post lockdown due to COVID-19. CreditAccess/MMFL collection efficiency were at 88 percent/83 percent as on September 2020 versus 74 percent/54 percent as on June 2020, respectively. Around 8 percent of CreditAccess and 7 percent of MMFL borrowers have not paid so far.

We expect gradual recovery in disbursements on the back of steady demand and adequate liquidity.

We maintain positive stance, on back of diversified set of product portfolio, strong domestic presence in all segments of automobile. SFL currently trades at we expect revenue to grow by CAGR of 5 percent over FY20-22E and net profit to grow by CAGR of 12 percent.

Over the years. SFL has reduced its dependency on fasteners business, currently fasteners is 36 percent (specialized fasteners within it is 25 percent and 8-10 percent revenue mix of standard fasteners) of total compare to 65-70 percent a decade back. Other product lines contributes 64 percent which includes engine components, pump assembly, powder metal and extruded products, wind energy and radiator caps. Company is focusing on higher share from other non-auto (industrial) segment such as defence, industrial machinery, aerospace and wind turbines. Aftermarket remains strong which is 10 percent, through strong dealership and distribution.

MGL's sales volumes have reached around 65 percent of pre-COVID levels in August 2020. CNG volumes have reached around 50 percent of pre-COVID levels in August 2020. We expect the current volume growth to pick up since the commercial activities and movement of vehicles have gradually revived. Owing to regulatory push towards relatively cleaner fuels like natural gas and considering government’s expansion plan in CNG Sector and Company’s growth in Compressed Gas Distribution (CGD), we are positive on Company’s long-term outlook.

With the ongoing capital expenditure, MGL is trying to increase its reach in new Geographical areas, especially in the Raigad region. In the longer run the growth story remains strong. With volume picking up, margins are expected to see a strong recovery.

Infibeam has started offering end-to-end payment solution through backward integration of services such as Merchant Plug-In, Directory Server and Access Control Server. The solution is implemented at an international bank and will be launched globally. Leveraging acquisition of Cardpay, it is planning to tape large market of credit offerings to SMEs and Corporates. The card payment business will allow the company to earn higher profitability (net take rate ranges between 50-100 bps) as it commands higher Transaction Discount Rate.

We expect topline and earnings estimates to grow by 63 percent and 113 percent yoy in FY22 as momentum will pick up in FY22 post revival from COVID-19 and recent tie-ups with Jio Platform and other leading banks based in Middle East.

Increasing investments in 5G, IOT, FTTH roll out and domestic led initiatives like digital India and opportunities arising from global demand is giving strong visibility of strong demand traction going forward. STL well placed to leverage the same with its unique set of capability from providing end to end solution and integrated offerings to its client (products are embedded with service which reduces the risk of pricing and increases the value added offerings).

Order book stood at Rs 10,312 crore (as reported in Q1FY21), diversified across 38 percent from Telco, 41 percent from Enterprise 20 percent from citizen networks and 1 percent from cloud player. Strong open participation funnel of Rs 10,100 crore. Going forward, we expect this trend to continue led by STL’s quality interaction with marquee global customers, multiple customer engagement across network use cases. We expect this trend to continue going forward, STL has unique capabilities to be a leading digital network integrator.

EID Parry is a defensive play with operations in sugar industry (essential commodity) with interests in Nutraceuticals segments. It is one of the top five sugar producers in India. EID Parry is preferred pick in the sugar space backed by leadership position, stable growth prospects and best-in class return profile. Besides, its reported improvement in profitability, attributed to the government measures of a) Minimum Selling Price of sugar b) monthly release orders c) robust ethanol prices.

EID Parry's shares have advanced around 80 percent in last 12 months against its subsidiary – Coromandel’s shares advanced of around 115 percent. Besides, EID Parry shares traded at 5-year average of 32 percent P/NAV discount whereas currently, the shares are trading at discount of 62 percent; offering attractive valuation.

Going forward, the management optimistically targets a significant reduction in slippages at around 2.75 percent over FY21-22E. However, we remained cautious on asset quality and have modelled slippages at 3.3 percent.

We expect the valuation upside for the bank to be led by cautious efforts of the management to control NPA and focus on retail (gold) loan business. We apply a P/Adjusted BV multiple of 0.55x to the FY22 adj. BVPS of Rs 77.2 to arrive at a target price of Rs 42 per share. Accordingly, we reiterate buy rating on the shares of KVB.

One of the leading building materials manufacturers in South Asia with a combined production capacity of 10,00,000 TPA; has 12 plants across South Asia and with 8,000 strong partner network. Ramco Cement is 5th largest producer in the country with Ramco SUPERGRADE being most popular cement brand in South India.

Historically, The Ramco Industries shares traded at 5-year average of 52 percent P/NAV discount whereas currently, the shares are trading at discount of 57 percent; offering buying opportunity. We value The Ramco Industries on SOTP basis with Core business at INR 117 per share and subsidiary businesses (after allowing for intrinsic valuation discount and shares pledged by the promoters) valued at Rs 163 and arrive at a TP of Rs 280.

We expect MCL to benefit from implementation of stricter emission norms which will increase the content per vehicle of wiring harness in 2W, 2W wiring harness would increase the content per vehicle 2.5x to Rs 900 per unit from Rs 400-450 per unit, it doubles the segmental revenue for MCL in wiring harness. MCL is leading supplier of wiring harness supplier to automotive OEMs, in this segment company is market leader with 35 percent market share in domestic 2W industry, 35 percent share in CV and 25 percent share in tractor. Currently 2-Wheeler segment contributes more than 50 percent to its revenue.

We believe domestic business is rightly placed with various product developments, gaining market share and increase share of business with existing OEMs. We expect the recovery in the overall business to happen by H2FY21.

Diversified investment portfolio that benefits from the robust credit risk profiles of the operating entities in which the value of investments is substantial the strong reputation of the Birla group. It also enjoys steady financial performance from its stake in Hindalco, Grasim, ABFRL, ABCL, Ultratech, Century textiles, Hindalco and others. The group has consistently rewarded its shareholders with a strong dividend track record for the last ten years (dividend yield stood at around 1.6 percent)

Historically, Pilani Investment & Industries shares traded at 5-year average of 74 percent P/NAV discount whereas currently, the shares are trading at discount of around 78 percent; offering upside to current market price. We value Pilani Investment on SOTP basis with Standalone business (dividend and interest income) valued at Rs 215 per share and investments in listed/unlisted/MFs valued at Rs 2,078 (after allowing for intrinsic valuation discount) and arrive at a TP of Rs 2,293.

Digital only subscription which (B2C) is expected to set next wave growth for TV18. This has further benefited from consumption tailwinds that have been boosted during the lockdown. The Broadcaster OTT app VOOT saw an increase in consumption of digital exclusive content. VOOT (Viacoms18's Over the top), its average daily viewership of 45+mins that is the highest amongst broadcasters OTT apps. Voot Select, the freemium offering was launched in Mar-20 with live channels, digital first broadcast content.

We expect advertising revenue to improve on back of increase in TV and Digital media consumption. Ease of lockdown restriction and resumption of content production for National and GEC gradually. We expect recovery in ad-spend to kick in from H2FY21 on account of recovery in overall economic activity and favourable government measures.

We expect Emmbi's business mix to gradually shift towards water conservation business as the popularity of ponds has been increasing with rising awareness for water storage. Demand for pond liners is seeing good traction with an average run rate of making ponds at 13 per day in Q1FY21.

The demand in the B2C rural agri distribution for the Emmbi is stable and on expected lines. Avana which focuses on B2C segment is continuing to expand and is expected to clock in Rs 100 crore in FY21. We expect the Revenue/PAT growth for the company at 8.3 percent/20.0 percent, respectively, over FY20-22E.

Shares of the company are currently trading at PE valuation of 9.2x/6.9x on FY21E/FY22E earnings. Expecting a recovery in upcoming quarters & stable margins, we continue to apply P/E multiple of 8.0x on FY22E EPS of Rs 12.0 per share and maintain target price of Rs 96 per share.

Disclaimer: The views and investment tips expressed by investment expert on Moneycontrol.com are his own and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

"TV18 Broadcast is a part of Network18 Media & Investments Ltd which publishes Moneycontrol."

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.