Abhijeet Dey, Senior Fund Manager, BNP Paribas Mutual Fund expects the RBI to keep a long pause for the better part of the CY19. If crude oil continues to remain stable, it could be a big benefit for the Indian macros at multiple levels, he added in an interview to Moneycontrol's Sunil Shankar Matkar.

Q) Do you foresee any big correction in 2019 after a positive close in 2018? What risks should investors stay wary of in 2019?

A: Looking ahead into CY19, we believe it will be a tale of two halves with macro environment dominating the first half in the form of trade war developments, the US Fed rate movement, and then the upcoming general elections in May. After this, the focus will move towards micro factors, primarily the earnings recovery (Bloomberg consensus earnings around 15 percent in FY 19 and 26 percent in FY 20) led.

To this earnings recovery theme, we add four over-arching themes that are likely to decide how the various companies stack up on their execution. These are (a) The preparedness to benefit from framework reforms that are in place for sustainable growth in for medium to long term, (b) Economic recovery being led by consumption, (c) Gradual revival of manufacturing/investment capex, (d) Embracing and accelerating digital disruption.

In that sense, we believe that amidst the volatility this year, the stock selection across sectors and market capitalisation will be a key for outperformance.

Thus while we can have volatile moves in the market in first half of CY 19 due to macro events, we believe equity markets will be supported due to strong earnings recovery. And hence, ceteris paribus, we do not expect large corrections in equity markets.

Investors should avoid making investment decisions influenced by the greed and fear due to market volatility and should consider continuing their long term ‘goal-based’ asset allocation into the markets.

Q) Will India decouple from the developed markets' slowdown in 2019 or could it be dragged down due to the slowdown in global growth ?

A: Unlike the situation in the decade of 2000s, India accounts for one of the highest contributors to incremental demand across a wide basket of bulk commodities, particularly energy commodities such crude, coal etc. In addition to that, the country’s reasonably large profit pools from the listed equity market perspective are in sectors such as IT, Energy, Pharma, Auto and Materials sectors. In that sense, given the developments on trade wars, US Fed rate movement, etc. we don't see the equity markets being entirely decoupled from any major slowdown in the developed markets.

In the same vein, however, some of the framework reforms carried out over the last few years does position India in a relatively unique space. The improving capacity utilisation across a host of end-user industries, a widening tax base – thanks to GST implementation, better adoption of digital initiatives, Jan Dhan accounts as well as the likely benefits of the Insolvency and Bankruptcy code implementation makes India one of the few markets where the fundamentals are relatively strong at this point amongst emerging markets. This, if coupled with sustained benign commodity inflation, can lead to a healthy macro environment which over a

period can drive better micro level improvement.

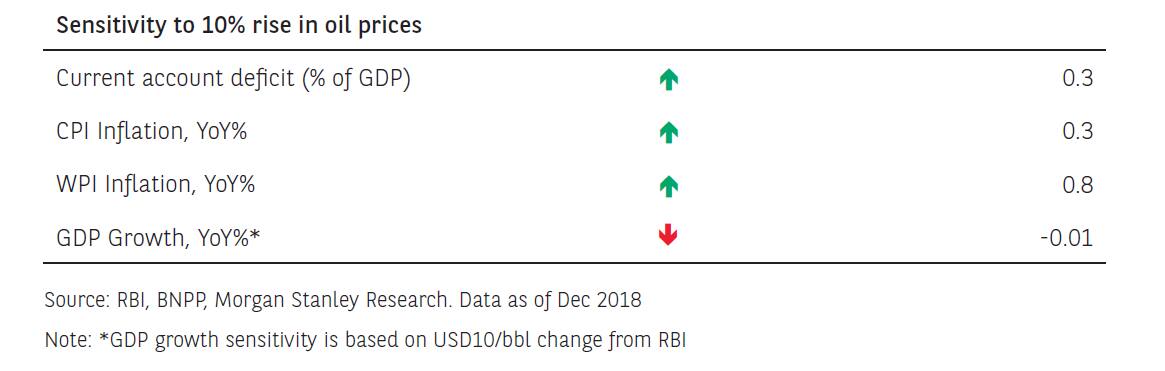

Q) Crude oil prices have stabilised after the recent crash amid global growth concerns and oversupply. Will this prove to be a game

changer for India's growth in the coming quarters if it continues to remain stable?

A: If crude oil continues to remain stable, it could be a big benefit for the Indian macros at multiple levels. The key sensitivities be it in terms of Current account/trade deficit, CPI/WPI inflation is well articulated (refer table below). On top of this, a sustained benign price will also bolster:

- A revival of capex in a multitude of industries given that crude derivatives are used in a wide spectrum of industries;

- Also provides the Government with fiscal room to undertake some bold welfare related reforms;

- And the consumer discretionary spends to trend up at the margin.

In that sense, yes crude remains a key variable.

Q) Gold and real estate are getting few takers now. Does this mean more domestic money will flow into equity and fixed income during 2019? Also, what is your take on FII investment?

A: Financialisation as a theme has been an ongoing one in the Indian markets and structurally we believe this will continue – like in most other countries. Gold and real estate are physical assets that have historically been hedged against higher inflation levels and as we tackle that, these asset classes have been out of favour.

If volatility increases to extremes in the financial markets, then one might see some move towards these asset classes, but the longer term structural move towards financial assets is likely to continue in our view, given the RBI is committed to ‘inflation targeting’ and ‘positive real rate of interest”.

Foreign investors (FIIs) flows turned positive on a monthly basis over the last two months. Our sense is that emerging markets may make a comeback this year given the softening of the rate hike cycle in the US leading to incremental weakening of the dollar, which could be positive for emerging equity markets in general.

There is valuation gap vis-a-vis the growth rates and currencies for some countries including India. In that sense, India, being amongst the fastest growing economies, is positioned well. The upcoming election though remains a key event and foreign investors may want to re-look at the Indian markets in a more meaningful manner once this event is behind us.

Q) Do you expect the RBI to cut or hold repo rate in 2019 given the falling CPI inflation and favorable macros?

A: We expect the RBI to remain at a long pause for the better part of the first half CY19. Though the new Governor has hinted a dovish bias on interest rates, we need to be cognizant of global headwinds emanating from US politics, Eurozone parliamentary election shaping the Eurozone, rate path of US Federal reserve, as well as the possible tightening stance from ECB.

The MPC could err on the side of caution and hold rates. The demand-supply dynamics looks fairly balanced for better part of Q1 CY 19 and thus, till the RBI keeps the tap open for liquidity via the OMO purchases, we are constructive on the sovereign curve. However, with the increased supply of SDLs because of political populism through farm loan waivers, we expect it to crowd out the investments in the corporate bond space keeping the spreads elevated.

We expect the 10-year G-sec to trade in the range of 7.10 percent -7.40 percent for the first half of CY2019. We expect the RBI to actively provide liquidity to the banking system via increased OMOs in Q1 CY 19, add to it improved capital flows via remittances and portfolio flows. Thus with a long pause at rates, we expect the yield curve to steepen going forward.

Q) Where do you see good opportunities (sectors) in the current market condition, especially for 2019?

A: Given our outlook for the year and the themes mentioned earlier, we are positive on sectors like private sector banks (given they are seeing continued momentum in retail business and the receding credit quality issues with the corporate loans), insurance companies (continued benefits of the financialisation of savings), consumer staples, paints, media, retail (that have tailwinds from improved consumption drivers). We also like select chemicals, gas utilities and industrial players (that are likely to derive

benefits from the developments in China around pollution and trade wars; as well as the improving utilisations in the Indian industry).

Our stance on technology is neutral and driven by a more bottom-up view on the various companies. While we see the likely global growth slowdown resulting in the order pipeline, and growth levels moderating from previous year levels, the companies have improved their competency levels in the new emerging technologies and are better placed. This, coupled with improved capital allocation and reasonable valuations, offers balanced risk-reward. We are also neutral on the diversified financials given they are going through a period of growth slowdown (vs the elevated growth levels were seen in the last few years) owing to the recent liquidity issues and the

likely change in funding sources.

Our underweight stance on the auto sector is due to likely pressures from the increased cost of regulatory changes that are having an impact of demand as well as profitability. As to the other major sectors, we remain underweight on public sector banks, given their continued market share losses and balance sheet constraints. On pharma, while there is likely to be large earnings growth, it is coming on a very subdued base and the valuations are yet not at a level where the risk-reward is favourable, except fot a few names.

Given the global growth slowdown, we remain underweight on metals names as they are likely to face the twin pressure of subdued prices and the elevated leverage levels.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.