Indian equity benchmarks bounced back with more than a percent rally for the week ending September 5 after a sharp weakness in previous week, but the upmove was not convincing enough to set the further uptrend given the pressure at higher levels amid uncertainty over US tariffs and consistent FII outflow.

The GST rate rationalisation and subdued oil prices supported the market rally but global trade tensions and persistent foreign outflows weighed on sentiment, while the safe haven demand pushed the gold prices to fresh record high of $3,655.5 per troy ounce amid above-average volumes.

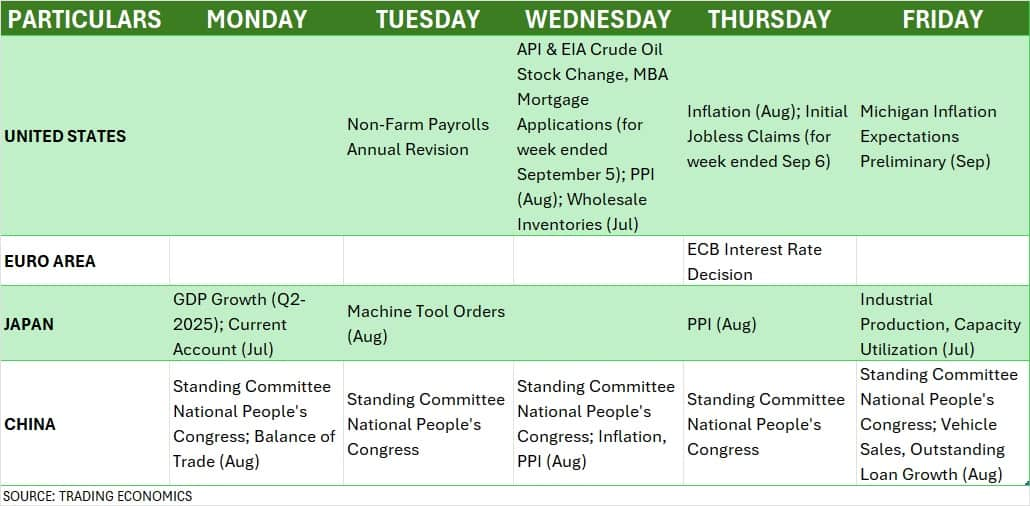

In the coming week starting from September 8, the market will remain volatile and rangebound with focus on India & US inflation, China's NPC meeting, ECB interest rate decision, weekly US jobs data, and any updates related to India-US trade deal, according to experts.

The BSE Sensex soared 901 points (1.13 percent) to 80,711 and the Nifty 50 jumped 314 points (1.29 percent) to 24,741, while the Nifty Midcap and Smallcap 100 indices outperformed the benchmark indices, gaining 2.42 percent and 2.49 percent, respectively. Most sectors led the rally but Nifty IT dropped 1.55 percent amid fear of reduced discretionary spending.

"While external headwinds from global trade uncertainties and tariff hikes remain a key risk, the combination of a simplified GST framework and positive domestic macros would underpin market momentum in the near term," Siddhartha Khemka - Head of Research, Wealth Management at Motilal Oswal Financial Services said.

According to Vinod Nair, Head of Research at Geojit Investments also, the sentiment is likely to remain mixed. "A multi-asset investment strategy is expected to gain traction in this environment," he said.

Here are 10 key factors to watch next week:

India Inflation

All eyes will be on the retail inflation for August due on September 12, which is a crucial data along with global factors for the Reserve Bank of India Monetary Policy Committee (RBI MPC) to make interest rate decision in the September 29-October 01 policy meeting. In July, the inflation dropped further to 1.55 percent from 2.1 percent in previous month. This is the first time that the inflation fell below the RBI's 2-6 percent inflation range (i.e. 4 percent +/- 2 percent), signalling the hope for rate cut. But now most economists believe the inflation rate seems to have bottomed out.

The RBI in its August policy meeting clearly indicated that it wants to see transmission of previous 100 bps repo rate cut before going for further cut, focussing more on growth, though there is a scope for one more rate cut.

Further, bank loan & deposit growth for the fortnight ended August 29, and foreign exchange reserves for week ended September 5 will also be released on the same day.

US Inflation

On the global front, the focus will be on the US inflation for August releasing on September 11. Most economists see the inflation rising a bit in August, compared to 2.7 percent in July, one of the critical factors for making interest rate decision by the Federal Open Market Committee (FOMC).

Further, the weekly jobs data, and preliminary Michigan inflation expectations for September will also be watched.

China's Top Legislature Meeting

Apart from US inflation, globally, the key factor to watch next week will be the seventeenth session of China's top legislature - the 14th National People's Congress and its Standing Committee - scheduled next week during September 8-12.

According to China Daily reports, the lawmakers will review a slew of draft laws, including atomic energy, public health emergency response, national parks, safety management of hazardous chemicals, and other pressing issues. Also, lawmakers will deliberate on a series of proposals, including one for reviewing the draft revisions to the Cybersecurity Law, and one for reviewing an extradition treaty between China and the Republic of Serbia.

Global Economic Data

Apart from US economic data and China's top legislature meeting, the European Central Bank's (ECB) policy meeting, and Japan's final GDP growth numbers for April-June quarter will also be watched next week.

Most economists expect the ECB to keep its interest rates unchanged at 2.15 percent in its policy meeting scheduled September 11, wanting to see the full impact of US tariffs on the economic growth and inflation, before making decision of further rate cuts. In the last meeting in July, the central bank ended its monetary easing after eight cuts, while the inflation in August, as per preliminary estimates, increased to 2.1 percent from 2 percent in July.

Further, as per preliminary estimates, Japan's economy expanded to 0.3 percent in Q2-2025 against the revised 0.1 percent growth registered in Q1 despite US tariffs.

The market participants will also check the mood of the FIIs (Foreign Institutional Investors) who remained net sellers even in the first week of September despite India announced GST reforms to boost consumption, concerning about high valuations and Trump tariff related uncertainty along with delay in trade deal.

FIIs net sold to the tune of Rs 5,667 crore in the week gone by, but domestic institutional investors (DIIs) maintained their bullish stance on equities, completely offsetting FIIs outflow and net buying Rs 13,444 crore worth shares in the week.

Indian Rupee

The focus will also be on the Indian rupee which hit the record low of 88.3625 against the US dollar, before finishing the week at 88.1430, weakening by 0.02 percent and extending weakness for second consecutive week due to consistent FIIs outflow and uncertainty with respect to India-US trade deal, though there were reports of RBI intervention to curb losses and support from US dollar index weakness and subdued oil prices. The currency futures formed Doji-like candlestick pattern last week, indicating indecision among bulls and bears.

Experts expect the rupee to remain volatile in the coming week amid the dominance of external headwinds.

Meanwhile, the US dollar index dropped 0.12 percent during the week to 97.737 following disappointing US jobs data, sustaining below all key moving averages, and forming indecisive candlestick patterns for last few weeks.

The primary market will remain in full swing despite volatile and rangebound action in the secondary market as investors will see the launch of 10 new IPOs (initial public offering). This includes three from the mainboard segment which are Urban Company, Shringar House of Mangalsutra, and Dev Accelerator worth Rs 2,444 crore, opening all on September 10.

Other seven new public issues - Krupalu Metals, Nilachal Carbo Metalicks, Karbonsteel Engineering, Taurian MPS, Jay Ambe Supermarkets, Airfloa Rail Technology, and LT Elevator - will be from the SME segment. Further, the SME IPOs which opened last week for public subscription including Austere Systems, Vigor Plast India, Sharvaya Metals, and Vashishtha Luxury Fashion will close next week.

On the listing front, total seven companies will debut on the bourses including only one from the mainboard segment which is Amanta Healthcare. And the remainder six firms - Rachit Prints, Goel Construction Company, Optivalue Tek Consulting, Austere Systems, Vigor Plast India, and Sharvaya Metals - will be from the SME section.

Technical View

Technically, the market mood remained cautious though there was optimism with more than a percent rally. The Nifty 50 formed bullish candle with long upper shadow on the weekly timeframe, indicating positive trend but selling pressure seen at higher levels. The index took support at 24,400, the previous week's low as well as the upward sloping support trendline, and closed above 20-week EMA, but failed to sustain above the midline of Bollinger bands (24,775) and close above the previous week's high (25,000), i.e. traded within previous week's range.

Hence, the index is expected to be in the 24,400-25,000 range in the upcoming week. Above 25,000 can open door for 25,200-25,250, but below 24,400, 24,300 is likely to act as crucial support as below which bears may take full charge, according to experts.

F&O Cues

The weekly options data suggested that the Nifty 50 is expected to be in the 24,500-25,000 range next week as decisively breaking of the range on either side can give firm direction.

The maximum Call open interest was seen at the 25,000 strike, followed by the 25,500 and 24,900 strikes, with the maximum Call writing at the 25,100, 25,400 and 24,700 strikes, while the 24,000 strike holds the maximum Put open interest, followed by the 24,500 and 24,600 strikes, with the maximum Put writing at the 24,000, 24,650 and 24,800 strikes.

Meanwhile, the fear index India VIX reached to nearly two-year low last week, which is definitely favouring bulls but being at lower zones also signal some alert for sharp moves on either side. The VIX fell sharply by 8.27 percent to 10.78, the lowest level since October 9, 2023. Overall, the index has been rangebound since the mid of July this year.

Corporate Action

Here are key corporate actions taking place next week:

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.