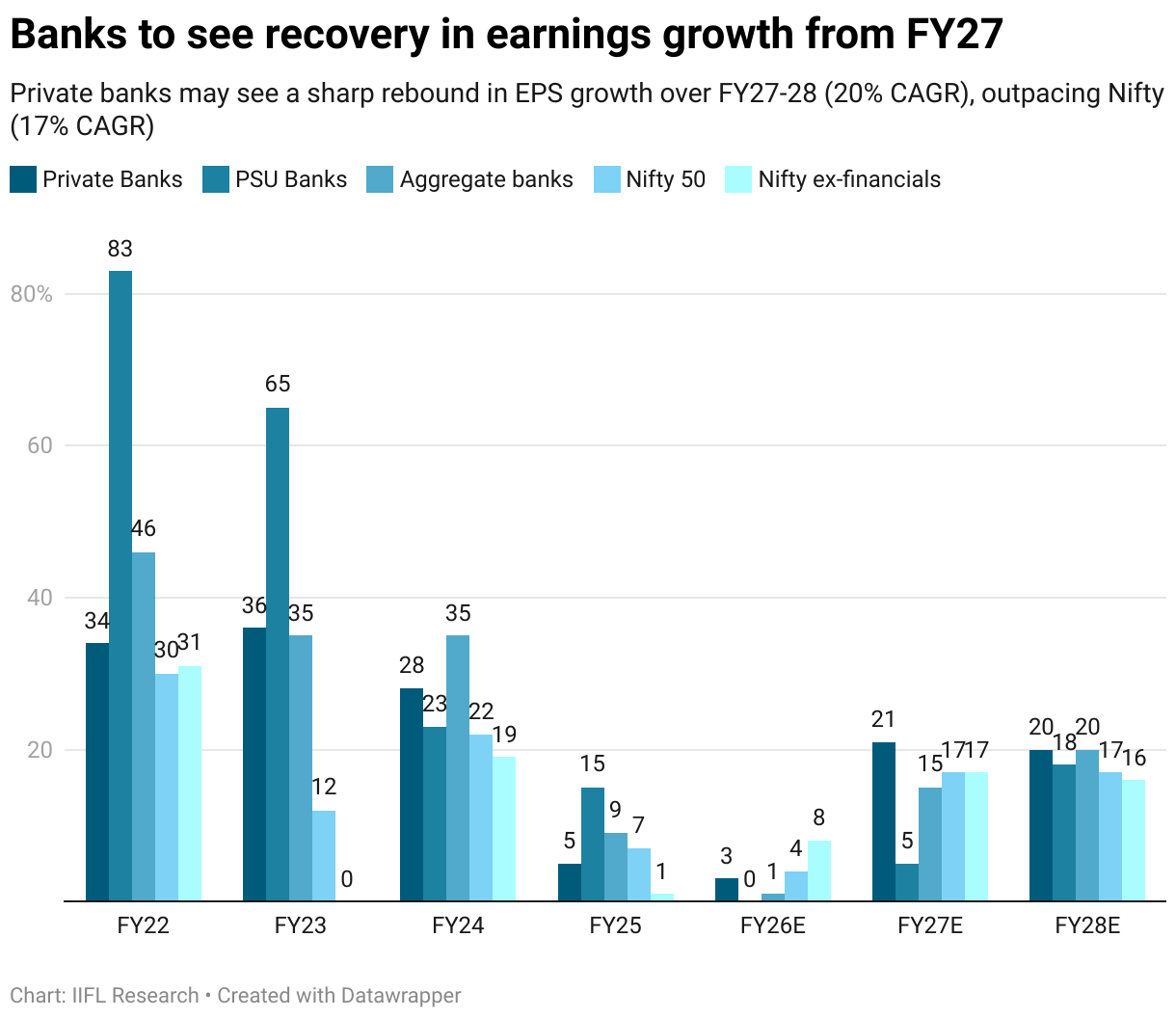

While the banking pack is likely to report lacklustre earnings for the rest of the financial year 2026, private and public banks are likely to stage a smart rebound over FY27-28. As loan growth bottoms out, a cyclical recovery in net interest margins (NIMs), and improvement in unsecured retail stress are likely to lead to a 18 percent CAGR over the next two years for the overall banking system, according to IIFL Capital.

However, loan growth might not see a sharp acceleration as home loan growth has historically moved in line with interest rate trends. Corporate borrowers are also continuing to shift towards the bond markets, which is currently costing banks about 20 percentage points of market share. Further, the overall system credit is already growing at a healthy 13 percent year on year, compared with 10 percent for banks, which implies a 1.3 times credit multiplier.

On the NIMs front, margins have surprised positively in the September quarter, spurred by the Reserve Bank of India's n liquidity infusion. This sped up rate transmission and pushed fresh lending and deposit rates down by around 90 to 95 basis points.

The brokerage noted that this move ended improving funding costs, which in turn lifted NIMs. Going ahead, analysts expect the recent CRR cut to add another 7 to 9 basis points, with time deposit re-pricing likely to cushion the effect of any further 25 basis point policy rate cut.

"However, we expect PSUs’ NIM recovery hereon to trail Private banks, due to the delayed MCLR cuts - down 25 bps for PSUs compared to 55 bps for private banks since February 2025," noted the IIFL Capital report.

Fee income remains soft for Kotak Bank, Bank of Baroda and IndusInd Bank, while cost controls helped most lenders manage top-line pressure, with only HDFC Bank and Kotak showing "positive jaws."

Additionally, a key factor to assist recovery is easing stress in the unsecured retail lending segment. Public sector banks anticipate a one-time expected credit loss (ECL) impact of about 1 percent of loans. While NBFCs' MSME portfolios are likely to see rising stress, personal loan stress across categories seems to have peaked, according to IIFL Capital, with the microfinance segment seeing healthier trends as well.

Overall, most banks reported lower net slippage ratios both sequentially and year on year, except IndusInd Bank and Federal Bank. With ageing-linked provisions for unsecured retail loans, credit costs are expected to rise by 17 basis points in FY26 before easing by 8 basis points in FY27 as retail stress moderates and corporate asset quality remains stable.

As a result of all the factors, banks' earnings are likely to rebound to see a CAGR in the high-teens. Over FY27 and FY28, IIFL Capital sees 21 percent, 14 percent and 18 percent CAGR for private, public, and overall banks.

FIIs and DIIs have trimmed their overweight exposure in private banks. The brokerage noted that FPIs have sold $15 billion of financials in the last four years, but "the tide is turning" with net inflows into the segment to the tune of $1.5 billion in October 2025.

The risk-reward for the banking pack is also very attractive at the current juncture. The overall banking pack commands a valuation of 12x one-year forward earnings, as compared to Nifty's 21x one-year forward earnings, which is one standard deviation above the long-term average.

IIFL Capital is bullish on Axis Bank, ICICI Bank, HDFC Bank, and SBI among the large banks, and prefers RBL Bank among the mid-sized banking pack.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.