Ruchi Agrawal

Moneycontrol Research

PI Industries (PIND) posted a weak Q4 FY18 performance due to delays in custom synthesis shipments caused by logistical issues at ports. Though performance showed some traction sequentially, revenue and operating profit growth remained muted on a year-on-year (YoY) basis. Earnings before interest, tax, depreciation and amortisation (EBITDA) dipped 12 percent YoY with an almost 390 basis points YoY contraction in EBITDA margin. Adjusting for taxes, net profit saw a substantial decline YoY and overall earnings dipped almost 22 percent YoY.

We see weak results as a passing phase and expect improved performance in FY19 owing to several positive operating factors like substantial growth in the custom synthesis manufacturing (CSM) segment, healthy order book line-up, limited and reduced exposure to rising global raw material prices and new product launches for the domestic business.

Segment-wise performance

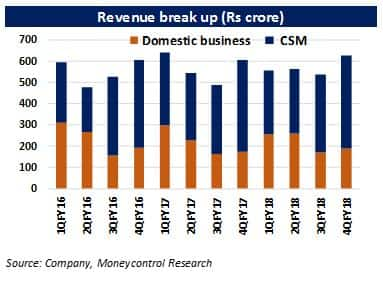

FY18 remained a weak year for the company, with first half impacted by slow growth in global demand and H2 hit by raw material and logistical issues.

During Q4, the domestic business reported a healthy 10 percent YoY growth, but the same was offset by tenderness in the CSM segment. Weak performance in CSM was mainly on the back of several logistical issues and congestion at the port due to which there was a pile-up of inventory. The management said these issues have now been addressed and there is steady flow of stock. It has guided for aggressive revenue growth of around 18 percent in this segment.

New products to drive growth

After a weak year, the company now has an aggressive line-up of products which is expected to drive growth in the coming quarters. At present, there are around 70 products in various stages of development, which is almost twice that of FY18. Four new molecules were commercialised by the company in FY18 and another four are in the pipeline for FY19.

In the domestic segment, the management plans to launch four to five new products. It reiterated its optimistic outlook on the CSM business, underpinned by a robust order book and growing product pipeline. The company is looking for inorganic opportunities to diversify in the pharma CSM business.

PIND has announced capex plans of Rs 230 crore for two new plants by the end of CY18. This along with de-bottlenecking of existing plants should provide some support to volumes.

Raw material issues from China

FY18 saw tight raw material supplies owing to closing down of manufacturing units in China due to tightening of environmental policies. The same had impacted raw material availability and spurred prices of many inputs, which adversely impacted the entire agrochemical space. The management has now indicated that the raw material prices have softened with improving availability. Moreover, the company has reduced its dependence on Chinese imports and plans to further distance itself from its unstable supply via backward integration.

Nominee Gold

Nominee Gold is the flagship herbicide product of the company and is used primarily for rice cultivation. The product has witnessed increased competition as several generic players have entered the market, which has led to reduction in prices and realisations. According to the management, overall industry volumes expanded by almost 15 percent YoY, due to which the company has been able to retain its market share and volume growth. This has also helped in mitigating the impact of price reduction and increased distributor margins.

Outlook

Owing to several operational and macro factors, FY18 remained a difficult year for PIND. With consecutive weak quarterly performance, the stock saw corrected around seven percent in the last three days and is now 20 percent below its 52-week high. Post-correction, the stock is trading at 24 times FY19e price-to-earnings.

Continued commercialisation of new products, nearing timelines for the strong order book line-up, global recovery in agro-chemicals, clearing up of inventory channels and a conducive domestic agri pricing environment, we expect growth to pace up in FY19. PIND is a quality stock in the agro chemical space. At current prices, it is worth looking at from a long-term perspective.

Follow @RuchiagrawalFor more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.