Rakesh Damani-led Avenue Supermarts (D-Mart) is set to present its earnings report for the third fiscal quarter of FY25 on January 11, 2025. The higher sales growth, as a result of increased store expansions are likely to lead revenue growth in the high teens.

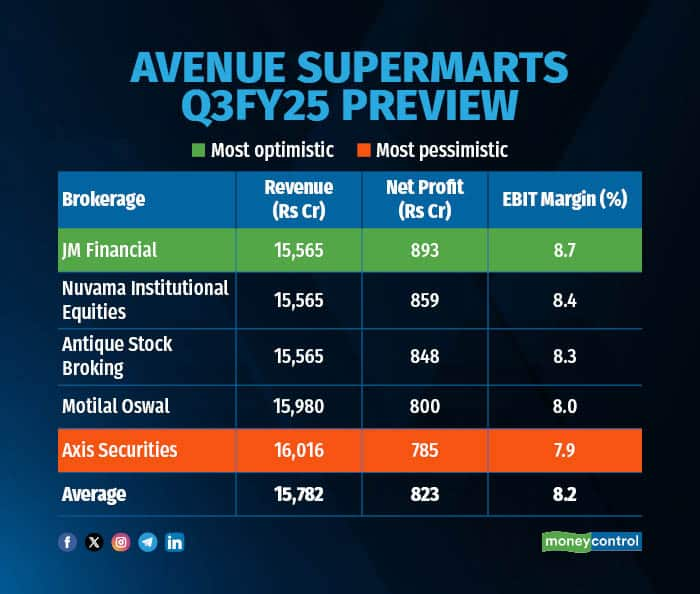

According to a Moneycontrol poll of five brokerages, DMart is likely to report a high revenue growth, up 19 percent on-year, at Rs 15,782 crore. However, in its business update for the quarter, DMart has already announced that revenues have risen 17.5 percent on-year.

Net profit is likely to come in at Rs 832 crore, up 19.2 percent from Rs 690 crore in the corresponding quarter last year.

Earnings estimates of analysts polled by Moneycontrol are in a narrow range, so any positive or negative surprises may elicit a sharp reaction in the stock. The most optimistic estimate sees DMart’s net profit jumping 29 percent on-year.

What factors are driving the earnings?

The factors driving the earnings will be store additions for the quarter, along with margins.

Demand Trends: "As per our understanding, demand witnessed a slight recovery during the festive period. However, the recovery was below expectations. Additionally, demand post the festive season failed to sustain and the overall environment remained muted during the quarter," said Antique Stock Broking on the demand scenario for retail players.

Segment performance: Brokerages expect a marginal improvement in the sale of general merchandise and apparel (GM&A) segment as consumer sentiment improves. The GM&A segment is highly margin accretive due to private product offerings.

Store additions: During the quarter gone by, Avenue Supermarts added ten stores, taking its total count to 387 stores across the country. In the same quarter of the previous financial year, DMart added five stores. Therefore, Q3FY25 saw higher openings compared to the base quarter. As a result of the store openings, Avenue Supermarts has seen a strong recovery in revenue/sqft despite increasing competition from quick commerce players, noted JM Financial.

Margins: According to Axis Securities, EBITDA margins are likely to contract on the back of higher operational expenditure, triggered by store expansions and weak gross margins. In contrast, JM Financial expects EBITDA margin to expand a marginal 20 bps. However, according to the Moneycontrol poll, the EBITDA margin is likely to be flat at 8.2 percent.

What to look out for in the quarterly show?

Analysts will closely monitor demand in metro areas and tier-3 towns. They will also pay attention to raw material prices and their effect on EBITDA margins, as well as the growing competitive pressure from unorganized players.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.