The Reserve Bank of India (RBI) Governor’s announcement on June 8 that credit cards will now be allowed to be linked to Unified Payments Interface (UPI) has given a huge upshot to both credit card as well as UPI transactions.

To begin with, it will only be RuPay credit cards, India’s homegrown card network. Until now, customers could link their UPI accounts only through debit cards.

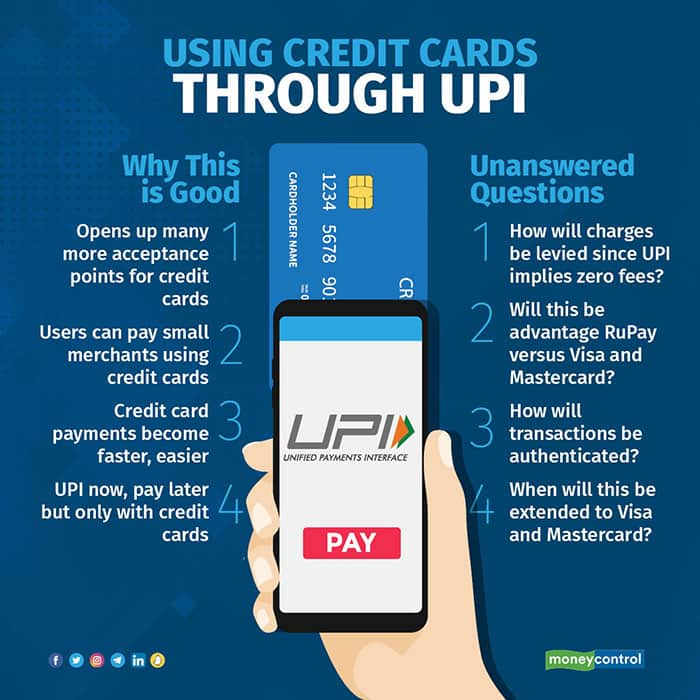

However, there are many questions to be answered.

The RBI and National Payments Corporation of India (NPCI), which operates and manages UPI and RuPay, is yet to clarify as to how the economics of this will work for card networks and other players.

How it will workUntil now, you could either use UPI or your credit card for making payments. If you are someone who prefers credit cards, you will have to take out your card, hand it to the merchant, put in a PIN in some cases and close the payment for every transaction.

Sometimes, this process would also mean waiting for the PoS machine to be free, or some machines not working, etc.

On the other hand, if you could just scan a QR code and pay using UPI, while still using a credit card for your transaction, life will be easier. That’s exactly what the new RBI move promises.

It is another step towards RBI’s plan to make all payments systems inter-operable – meaning all systems can work with one another and talk to each other.

A senior fintech industry source said on condition of anonymity: “Basically, what they are saying is that if you have a credit card, you can now use it at all terminals across the country. The adoption rate of PoS terminals is not as high as that of UPI. So this is a boon from an acceptance standpoint.”

In FY22, UPI made up 60 percent of all non-cash transactions, according to a joint report by PhonePe and the Boston Consulting Group. PoS transactions, on the other hand, made up only 5 percent. So, this opens up a larger avenue for credit card transactions.

Shinjini Kumar, co-founder of Salt, said: “Practically, this expands the scope of credit card transactions from only PoS to all UPI QR points. For now, this is a gain for RuPay credit cards. Whether this will further cannibalise into card transactions is something we have to see.”

If implementation picks pace, this could also be a threat to fintech credit players that offer Buy Now Pay Later (BNPL) options at points of sales across physical outlets and apps.

According to Monica Jasuja, Head of Money Management at Go To Financial, "This is a serious threat to BNPL who offer products to the non-credit card customers using this form of credit to get credit when and where they want. How can any serious BNPL provider compete with UPI at this scale? This actually gives credit card issuers a major boost."

Among all forms of digital payments, credit cards draw the highest charges. The merchant has to bear these costs. They are then divided among banks and payment service providers and are collectively called Merchant Discount Rate (MDR).

MDR is the key source of revenues for the payments ecosystem, including banks, and credit cards contribute the most.

As per norms, UPI (along with RuPay debit cards) comes under the Zero-MDR norm, which means that no charges are levied for these transactions. However, RuPay credit cards, like Visa and Mastercard, attract an MDR of 1.65 percent for classic cards and 1.85 percent for premium or platinum cards. The charges may go higher in some cases.

Card networks and banks cannot afford to let credit card transactions happen at zero charges, considering the costs involved.

Vishwas Patel, Executive Director at Infibeam Avenues and Chairman of the Payment Council of India (PCI), said, “It’s a very interesting development, but all ecosystem players need more clarity because in giving credit, there is a cost of funds involved for issuing banks, while in UPI transactions, the MDR is zero. There are lots of questions and a whole lot of clarity regarding the same.”

When asked about the pricing model, RBI Deputy Governor T Rabi Sankar said that “thinking about the pricing structure will be jumping the gun”. This is a clear indication that the RBI is not in a hurry to answer these questions.

A fintech executive, who did not wish to be named, said : “How the whole interchange play will work out is not very clear right now.” For many, the question is also of a new customer base when you get credit into the picture.

“If you're really trying to create a credit line on top of UPI, you really need to go into a different set of consumer base altogether. In that consumer base, it is not really a matter of card or UPI, it is a matter of underwriting that consumer,” he said.

Once credit is given, there are costs involved for underwriting and then recovering the credit from the customer. Furthermore, even if MDR is levied, the merchant will not know whether they are being charged an MDR or not because at the face of it, it will be just UPI. Only if the merchant asks the customer whether this is a credit card UPI payment or a debit, will they know.

“Generally, the MDR is decided by the payment scheme. I expect NPCI to set up a steering committee, which will basically deliberate on MDR. Card networks will not be okay with zero MDR because it will take away a majority of their revenues,” said Nikhil Kumar, co-founder of payments API platform.

Another ‘advantage RuPay’?Visa and Mastercard’s grievance against the Indian government for openly supporting and pushing for RuPay adoption is well known. In fact, Visa had also written to the United States government that the Indian government’s promotion of RuPay is hurting Visa’s prospects in the country, according to a report by Reuters.

Over the past few years, RuPay has also gained considerable market share in the number of cards issued. Under the Pradhan Mantri Jan Dhan Yojana (PMJDY), which was flagged off in 2014, the government issues only RuPay debit cards to new account holders.

According to the latest RBI data, RuPay had a 60 percent market share, led by debit cards. In the credit card space, however, RuPay lags behind Visa and Mastercard, which together make up around 80 percent of the market, according to sources.

“To be honest, it gives RuPay an unfair advantage over others because we have not figured out the pricing yet. If the customer now wants to pay at a roadside tea stall or a vegetable vendor using a credit card, for now, only RuPay will provide that option,” said the fintech industry source mentioned earlier.

The other question that remains unanswered is additional security for credit cards. The industry is awaiting clarity on how payments will be authorised for credit card UPI transactions – through a two-factor authentication or using just a UPI PIN.

A long-pending moveCredit on UPI has been a long-pending plan of the NPCI. Many fintechs, too, have been waiting for it. Credit on UPI was never launched as a separate product, owing to the unanswered questions on MDR.

While this announcement is a step in linking credit to UPI, it is not the same as what was planned earlier. Fintechs and banks can still not link your credit line to UPI without a thorough evaluation by NPCI.

NPCI also asked a few players like neobanking platform Jupiter to take down in-house credit-linked UPI products. Jupiter relaunched the offering after complying with NPCI’s norms and Jupiter Edge has been live ever since.

LazyPay, too, is in the implementation phase to launch a credit product, according to industry sources.

The source said, “NPCI is okay with fintechs doing this as long as the partner bank of NBFC is compliant with RBI norms. Additionally, UPI should be connected to a pre-paid payment instrument (PPI) and the fintech should not be extending a revolving credit line.”

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.