Anubhav SahuMoneycontrol Research

Thirumalai Chemicals (Market cap: 2227 cr), the second‐largest manufacturer in the domestic Phthalic anhydride (PAN), reported decent set of numbers backed by improved product pricing and turnaround in the Malaysian subsidiary.

Read our previous note: Thirumalai Chemicals: Exposure to varied markets, capacity expansion & diversification key triggers

Phthalic anhydride pricing trend benefits domestic business

Company’s standalone business which mainly consists of Phthalic anhydride business reported healthy numbers in Q3 2018. Net sales was up 18 percent on YoY basis. Sequentially, it was broadly flat. However, raw material cost declined by 14%/20% on YoY/QoQ basis. Consequently, gross margins continue to rise (44.7 percent vs. 33.5 percent in Q3 2017).

EBITDA margins were one of the best in recent times. Domestic supply tightness on account of closure of Phthalic anhydride plant of Asian Paints (29,796 MT) may have been one factor. Further, Chinese Phthalic anhydride price trend suggests there was ~18 percent increase in price during the quarter compared to about 5 percent increase for Xylene.

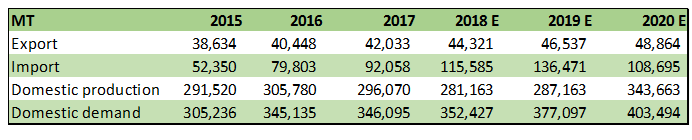

Table: Phthalic Anhydride demand supply

Source: Ministry of Commerce, Ministry of Chemicals, Moneycontrol research

Source: Ministry of Commerce, Ministry of Chemicals, Moneycontrol research

Turnaround in Malaysian subsidiary

At the consolidated level, company reported even better performance. Net sales were up 39 percent YoY and EBITDA almost doubled in last one year. Sequentially, both topline and bottomline gained, unlike standalone numbers. This was mainly due to the turnaround visible for the Malaysian subsidiary, Optimistic Organic. While last year, this entity was loss-making, it has turned around in recent times.

In the year-ago quarter, the contribution of this subsidiary to consolidated sales was 18 percent, this has improved to ~25 percent now. Same is for the profit, where contribution is about 16 percent now.

Financials and valuations

Near-term sales volume growth is expected to come from increased capacity for food acids, fine chemicals and the improved operations from Malaysian subsidiary.

In the medium term, company’s major volume growth is expected to come after completion of Phthalic Anhydride expansion.

Margin tailwinds are expected to continue with improving demand scenario for Phthalic Anhydride and Maleic Anhydride. Further, company’s exposure to food acids, fine chemicals are expected to aid overall margins, as well.

Based on recent results, we have upgraded our earnings expectations. Currently, stock is trading at a multiple of 11.1x 2019e earnings, which is reasonable and at a discount compared to peers in chemical universe.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!