Madhuchanda DeyMoneycontrol Research

Axis Bank’s first quarter was directionally positive but lacked the spark of the previous quarter. Margins shrunk as the bank shifted strategy towards creating a high quality asset book. The corporate loan book did not worsen incrementally, but there was stress in the agricultural portfolio.

If Axis is able to consolidate in FY18 with its calibrated steps, FY19 should be a much better year with lower provision and higher growth. The bank might consider a round of capital raising at that stage.

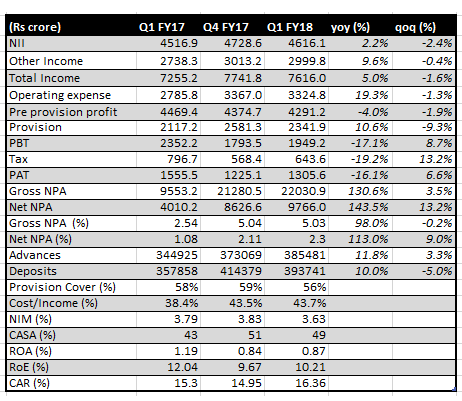

Results at a Glance

The reported numbers weren’t exciting. Earnings before provision declined by 4 percent. Advances grew 11.8 percent, but the 16 basis points year-on-year contraction in margin checked the growth in net interest income (the difference between interest income and expenses).

The growth in core fees at 16 percent was the only bright spot in the operational performance that was largely driven by retail products. One-time bonus payments to certain categories of contracted employees, pushed up operating expenses.

Provision grew by a modest 10 percent, causing a 16 percent decline in profitability.

Quality versus Profitability

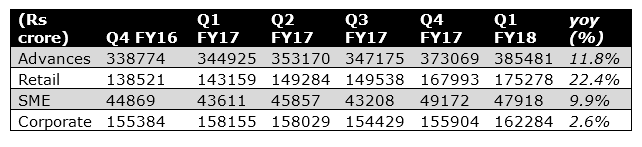

When it comes to choosing between quality and profitability, Axis Bank is clearly opting for the former. The incremental growth strategy is more measured and de-risked. The loan book growth has been driven by retail that is now close to 45.5 percent of total advances.

SME (small & medium enterprise) lending has been muted as the bank remains cautious till the GST adjustments are over. The only pocket of growth within the corporate book has been working capital.

The result of this strategy is evident in the compression of net interest margin (NIM). Despite a reduction in the cost of funds, NIM has fallen by 4 basis points from the blended level of FY17. This goes on to show that the bank is experiencing compression in yields as it is moving up the rating curve while picking up new assets. Incidentally, Axis has guided to 20 basis points margin compression in FY18 and close to 93 percent of its incremental lending is to corporates rated A and above.

Yet to Press the Accelerator

On the credit side, the bank has not pressed the accelerator in the same way as some of its private sector peers have. Axis’s share in incremental credit of the banking system stood at 9.3 percent last year and its share in incremental deposits was a more modest 3.4 percent.

The bank appears to be adopting a deliberate strategy of de-growing the term deposits book in order to stay competitive in the new MCLR (marginal cost of funds-based lending rate) regime. Incidentally, the share of the same is now higher in the portfolio.

In the quarter gone by, while low-cost deposits (CASA) have grown by 24.5 percent, term deposits have actually de-grown resulting in a more moderate 10 percent growth in deposits.

Asset quality – no incremental negative

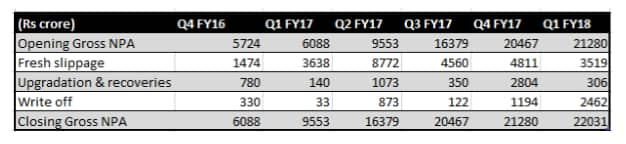

For Axis Bank, asset quality still remains a key monitorable. The net slippage for the quarter at Rs 3213 crore comprised corporate at Rs 2227 crore, retail at Rs 758 crore and SME at Rs 228 crore. The management highlighted stress in the farm loan book and hinted at “moral hazard” on account of the spate of loan waivers.

While the watch list has declined, the slippage outside the watch list that was witnessed in the quarter, brings the focus back to the stressed sectors. The bank has identified four stressed sectors namely infrastructure, power, iron & steel and telecom and has taken 1 percent standard asset provision on them (usual standard asset provision of 40 basis points), thereby allocating Rs 184 crore in the quarter.

Axis’s total fund based exposure to these sectors at Rs 48,640 crore is much larger than its watch list of Rs 7941 crore. While the watch list turning non-performing is largely factored, any lumpy slippage outside the watch list will be a dampener. While not guiding to any explicit number on slippage, the bank has maintained its credit cost guidance between 175 and 225 basis points (credit cost in this quarter was 195 basis points) in FY18.

We feel that as long as the slippage is limited to the exposure mentioned in the exhibit, the guidance on provision should hold.

The consolidation strategy of Axis Bank in FY18 should pave the way for a more balanced growth in FY19 with a much lower baggage of bad assets. The reduction in credit costs would provide a big delta to earnings in FY19 albeit the margin compression. We aren’t too concerned about the much rumoured change of guard at Axis as we feel the franchise should survive well once it comes out of the bad asset mess. The stock trades at 2.5X its adjusted book of FY18 and may be considered for accumulation on decline.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.