CEO(1) compensation has been a contentious issue in Corporate India for a few years now. A recent, yet-to-be-published IiAS study revealed that in 66 of the S&P BSE 100 companies, CEO pay had outpaced revenue or profit growth (or both) over a three-year period. The remuneration structure itself is of concern: in most of these companies, there is a higher component of fixed pay which is assured, with a limited share of performance-based pay, creating a weak incentive mechanism.

Universal hardships affect people differently — while some bear a higher burden, others give till it hurts, and some continue to self-preserve. Corporate India geared up to shield India from the COVID-19 onslaught, by quickly making protective gear, to supporting the healthcare system, and, of course, making vaccines. Even so, labour was hard hit. The exodus of labour, the layoffs, the furloughs, and pay cuts all impacted the average worker. While some industry leaders such as Mukesh Ambani or Uday Kotak(2) led in solidarity and took pay cuts in 2021, the feudal mindset of the proverbial ‘lala’ became far more pronounced as well.

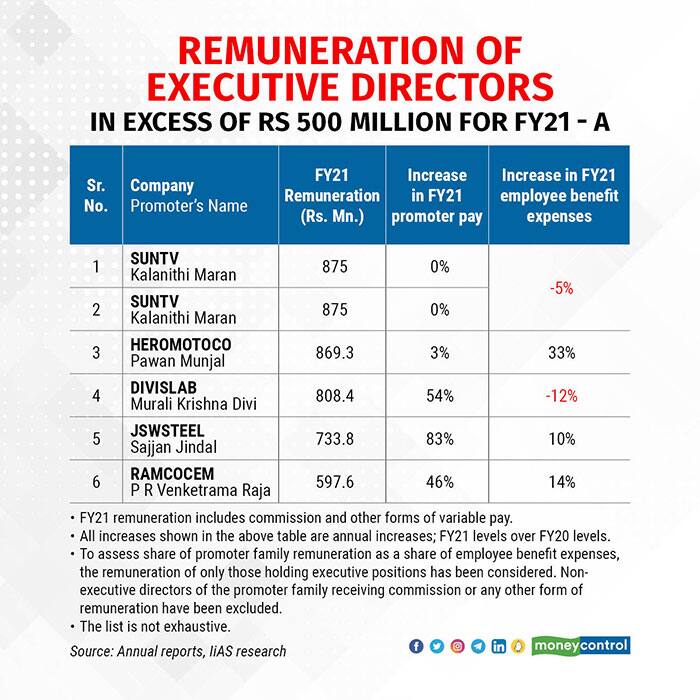

Of the S&P BSE 500, there were six executive directors whose remuneration in FY21 exceeded Rs 500 million (Table Below). These Indian companies do not have the size and complexity of their global peers to justify such remuneration levels. For context, the remuneration of the highest-paid board member of Toyota Motor Corporation (a company that has operations in about 200 countries and regions, and revenues in excess of $200 billion), aggregated JPY 1.45 billion for fiscal 2021, equivalent to about Rs 950 million.

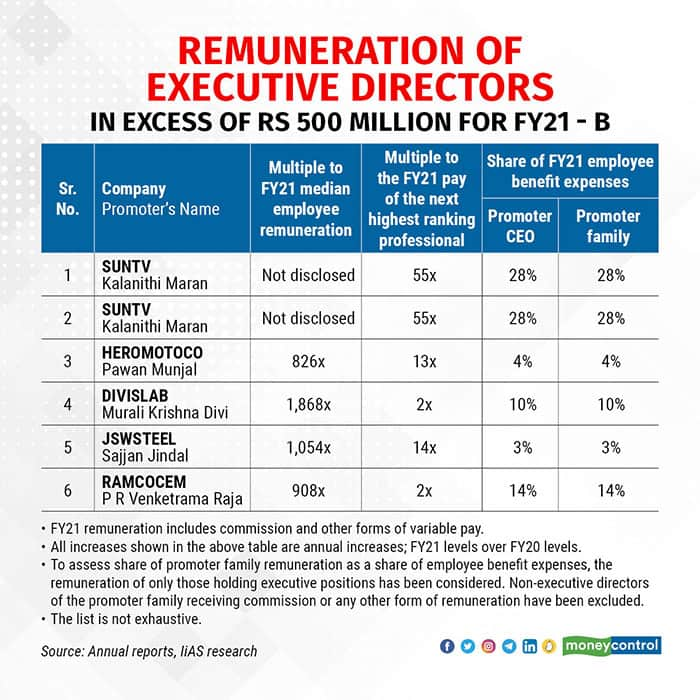

Industries like automobiles, cement, and pharmaceuticals have relatively higher levels of CEO pay. ‘Ours is a complex business in a difficult industry’, is the most common refrain when explaining high levels of remuneration. If that were true, at the very least, one would expect CEOs pay structures to be aligned to the company’s internal pay standards. Interestingly, for some promoters, this too is not true. Some promoter CEOs are paid more than 50x the next executive director who is a professional, and more than 1000x the median employee remuneration. For context, the CEO of Rio Tinto (a natural resources company that operates in more than 35 companies and generated revenues aggregating $44.6bn in 2020) was paid 81x the median employee remuneration.

Boards believe competence is genetic, independent of experience, and so there are a few 20+ year-old executive directors belonging to the promoter family that are paid almost equal to the company’s 50+year-old CFOs and other whole-time directors. Promoter compensation alone accounted for more than 20 percent total employee benefit expenses in a few companies.

Several companies’ businesses were deeply-impacted by the COVID-19 crisis — media and entertainment, hospitality, travel, and retail industries being the hardest hit. Some of these companies let go of employees, and others implemented pay cuts, yet the CEOs continued to be paid a high remuneration, and annual raises irrespective.

A company that reduced its headcount by more than 40 percent, gave its promoter CEO a pay raise because a fixed pay raise was baked into the remuneration structure when it was approved by shareholders. Making an exception during an exceptional year and not taking a raise was the right thing to do. Not only promoters, but professionals like Sandeep Bakshi of ICICI Bank(3) did so. Several companies reported lower employee benefit expenses in FY21, yet promoters got their pay increases.

The expectations for CEOs to deliver should not be different, whether they are promoters or professionals. Most professionals have a large proportion of their compensation linked to performance targets or through stock options — and so they are compelled to create shareholder wealth. For promoters, because their wealth (and in most cases their identity) is associated with the company, the general expectation is that they would be focussed on driving business. But in taking huge salaries, promoters are signalling that they are separating their roles as owners and managers. If so, shouldn’t there be equivalent performance standards for promoters too?

In most companies where promoter remuneration is being questioned by investors, the nomination and remuneration committees more often than not includes the promoter as well. While companies can extol the virtues of their conflict-of-interest policies, the practical realities are different — it is hard to ignore the promoter’s presence, whether they are physically in the room or not.

Boards too are happy having the promoter-in-charge: it is easy for them to delegate some of their responsibilities to the promoters. With such weak governance structures, setting performance orientation to promoter pay is a challenge. It is time for the regulator to consider putting executive remuneration of promoters to a majority of minority vote.

Promoter greed doesn’t go unnoticed. As investors watch executive remuneration closely, so do employees. While employees accept that promoters are a cut above, their (promoters’) behaviour during the crisis can deeply wound employee morale and loyalty. Companies describe human capital as one of their most important assets; yet its shabby treatment poses long-term risks for businesses. Boards urgently need to set greater accountability and ‘professionalise’ the promoters, an unenviable task by all measures.

Notes:

1: For the purpose of this article, CEO is being used as a generic term. It refers to the management leader, a role that may carry different designations across companies, including Executive Chairperson and Managing Director.2: Kotak Mahindra Bank is one of IiAS’ several shareholders3: ICICI Prudential Life Insurance Company Limited, part of the ICICI Group, is one of IiAS’ several shareholdersHetal Dalal is President and COO at Institutional Investor Advisory Services India Limited (IiAS). Twitter: @hetal_dalal. Views are personal, and do not represent the stand of this publication.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.