Inherent contradictions have long tangled the wires of India’s power sector, adding vulnerability to the Indian economy, and its commitment to clean energy.

To be sure, the government has drawn up an aggressive roadmap for the transition to clean energy. However, lack of infrastructure investments by bleeding distribution companies (discoms) are stymieing these plans.

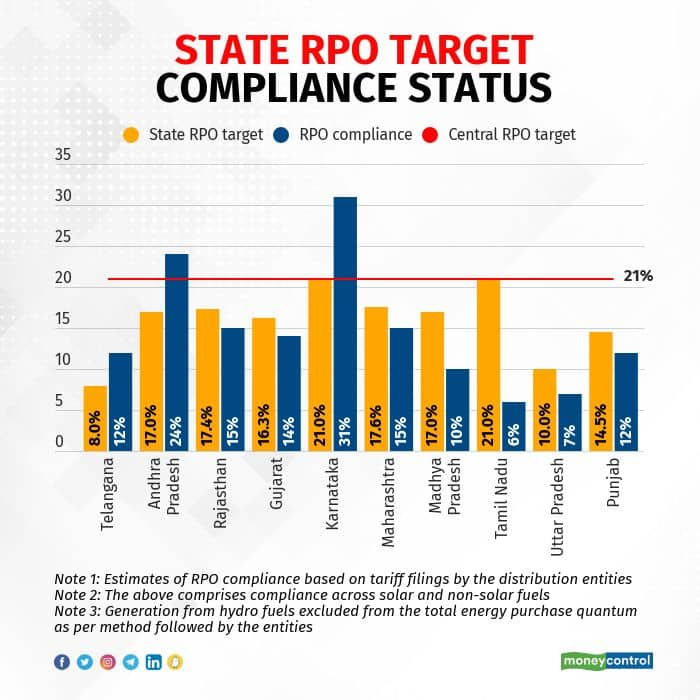

As a result, states are not only underperforming on their central renewable purchase obligation (RPO) goals, but are also largely unable to meet the often-lower targets set for themselves (see table below).

So, how can India meet its power needs, and energy transition goals?

Three things need to happen:

Let’s examine these intertwined necessities.

CRISIL Research’s transition modelling and analysis indicates that in the first decade of energy transition, 80 percent of capacity additions would be for non-fossil fuels, versus the opposite in the decade till 2020. Thus, reaching 50 percent RE generation by 2030, as targeted under COP26, is ambitious. However, tripling the RE share (excluding hydro) from 11 percent now to around 36 percent is possible — and will be a feat in itself.

For this to happen, investments in grid infrastructure, smart meters, energy storage, and new business models to handle intermittent power are inevitable.

Such expenditure will have to be driven by India’s 45-odd state discoms. But financial inefficiencies stemming from bad karma and operational logjams have left them with little ability to do so. Add policy U-turns, poor implementation of annual tariff revisions, and inadequate disclosure of financials, and what you have is high vulnerability.

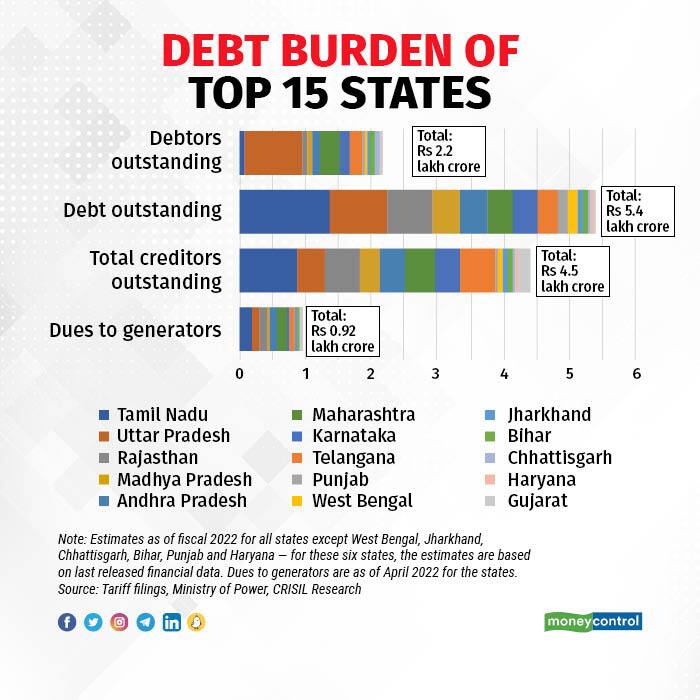

All that has meant debtor days (receivables from customers of the top 15 states, accounting for 85 percent of India’s power consumption) rising to 130-140 days as compared to an ideal benchmark of 30-60 days, and payments outstanding of Rs 2.2 lakh-crore (see table below).

The discoms’ dues to power generators stand at ~Rs 110,551 crore as on June 2022. Further, debt requirements are increasing with interest payments surging, even as operations bleed.

Non-receipt of such monies is why generators haven’t been able to shore up coal stocks despite a sharp 7.9 percent uptick in power demand in fiscal 2022.

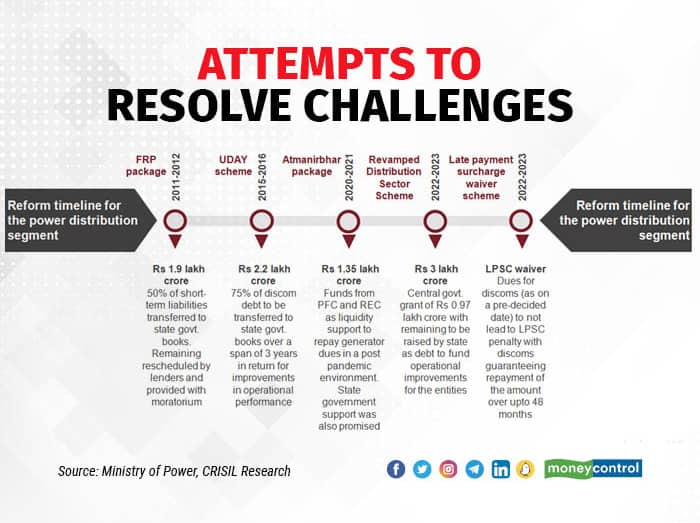

Attempts have been made to course correct. With UDAY, nearly Rs. 2.2 lakh-crore of discom debt was transferred in 2016 to corresponding state governments, paving the way for investments, and borrowings to trim system losses (see table below).

However, political interventions to keep subsidising power, alongside systemic inefficiencies have erased potential benefits. Further, low demand during the pandemic, especially from high-paying industrial customers, amplified the payment crisis.

It was the short-term liquidity infusion of Rs. 1.35 lakh-crore through the Aatmanirbhar package that prevented a ballooning of this crisis.

Fast-forward to 2022. The government has approved the Revamped Distribution Sector Scheme (RDSS) to give discoms another chance to take corrective actions, and gain funding access.

Some corrective steps have failed, some partially succeeded and the results of the rest are awaited.

However, the RDSS, along with amendments in the Central Electricity Authority (CEA), and the recent announcement of the Late Payment Surcharge (LPSC) waiver, can help the distribution sector build investor confidence.

Further, the recent open access rules will drive green power usage among commercial and industrial consumers. The LPSC waiver can enable discoms to regularise the significant dues to generators. It’s a win-win scheme — it prevents deterioration in discoms’ financials, and averts penalties, while assuring payments to generators over 48 months.

But there are several monitorables. How generators cope with the higher interest cost arising from receivables being staggered over 48 months, and how the government handles this funding bears watching.

For long, discoms have grappled with cash flows and dues. The ability to generate cash is crucial since subsidised electricity sales, systemic inefficiencies, and interest on legacy debt will not vanish overnight.

While the modalities of the LPSC scheme are awaited, funding for it would be a handy crutch for discoms. It will be the first step to transforming this segment of the power value chain.

Hopefully, it will lead to generation of ‘swachh’ power, paid for by ‘swachh’ discoms.

Hetal Gandhi is Director, and Surbhi Kaushal is Associate Director, at CRISIL Research. Views are personal, and do not represent the stand of this publication.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.