Ruchi Agrawal

Moneycontrol Research

Highlights

- Poor performance in Q3, substantial margin contraction

- AP licence suspension impacts stock

- Bajra and maize volumes decline, Rabi remains weak- Company working on diversifying product portfolio

-------------------------------------------------

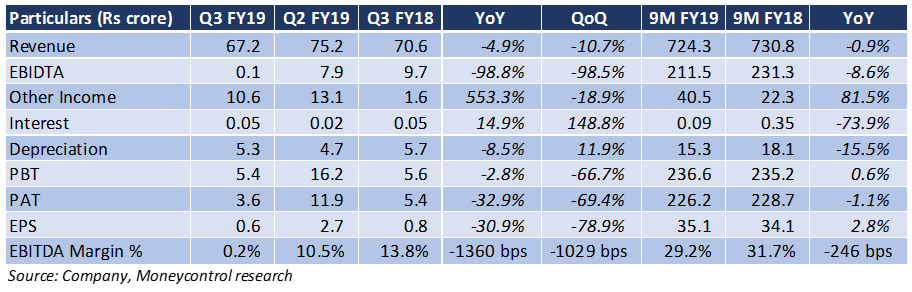

Shares of Kaveri Seed Company (KSC) have corrected substantially over the last few trading sessions following a weak Q3 and the news of licence suspension in Andhra Pradesh (AP). The Q3 performance remained dismal with a substantial year-on-year (YoY) contraction in revenue, profits and margins. Though Q3 is generally a lean quarter, the YoY degrowth indicates the tough operating environment, limited de-risking and internal inefficiencies.

Suspension of licence

-In a recent move, the AP government has suspended the sale licence of 13 major seed companies along with KSC in connection with an ongoing case about the herbicide resistance cotton seed gene. The announcement came as a blow to the AP based KSC and the shares tanked in trade.

-The company highlighted that the impact from the suspension would be less than 5 percent of the total revenue (around Rs 50 crore). Moreover, the management highlighted that they expect the licence to be renewed in the next 2-3 weeks, much before the upcoming Kharif season sales begin (starts in June-July)

Quarterly performance update

-Revenue declined 5 percent YoY majorly due to deficient and delayed rainfall which led to reduced acreages across crops. Fear of pink bollworm impacted cottonseed sales. Delayed sowing in the south and central India also had its impact.

-Earnings before interest, tax, depreciation, and amortisation (EBITDA) was hit due to higher employee expenses, other expenses and lower inventory gains during the quarter.

-Margins were also impacted due to lower sales of corn in Q3.

-Maize and bajra volumes remained under pressure. Maize sales were impacted due to fear of the Fall Army Worm. Bajra sales were severely impacted due to late and deficient rains.

-The performance of exports remained decent. The company is now working towards expanding the export segment in Nepal, Pakistan and Indonesia apart from Bangladesh.

Other observations

-The management is strategically focusing on reducing the cotton dependency in the product portfolio and aggressively launching new products in other categories like maize, rice, sunflower etc. The company expects to reduce the cotton segment from the current 60 percent to 40 percent in the next three years.

- With improving cotton and maize market prices, the management expects the acreages for these to go up in the upcoming Kharif season which would bode well for the sales volumes.

-The management maintained its guidance of 15 percent growth in cotton portfolio sales and 20 percent in the non-cotton sales for FY20

Outlook

The stock has seen a sharp correction in the last few months and is 36 percent below its 52-week high. After the correction, it is trading at a 12.5x 2020e (estimated) price to earnings (PE).

Various internal and external factors have impacted the performance of KSC in the last couple of quarters due to which the stock performance has been very volatile. The company’s product portfolio remains highly concentrated on cotton seeds where the overall environment has been unsteady. While the company is strategically working on reducing the cotton exposure, we believe it would take time to change the product portfolio and the risks would continue in the near term.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.