India’s home textile businesses have been successfully cashing in on growth opportunities in international markets in recent times. Himatsingka Seide, amongst the most well-known vertically integrated home textile majors and export-oriented houses in the country, has seen decent traction in earnings and is now expanding capacity to grow further.

So despite the stock outperformance, does it deserve attention?

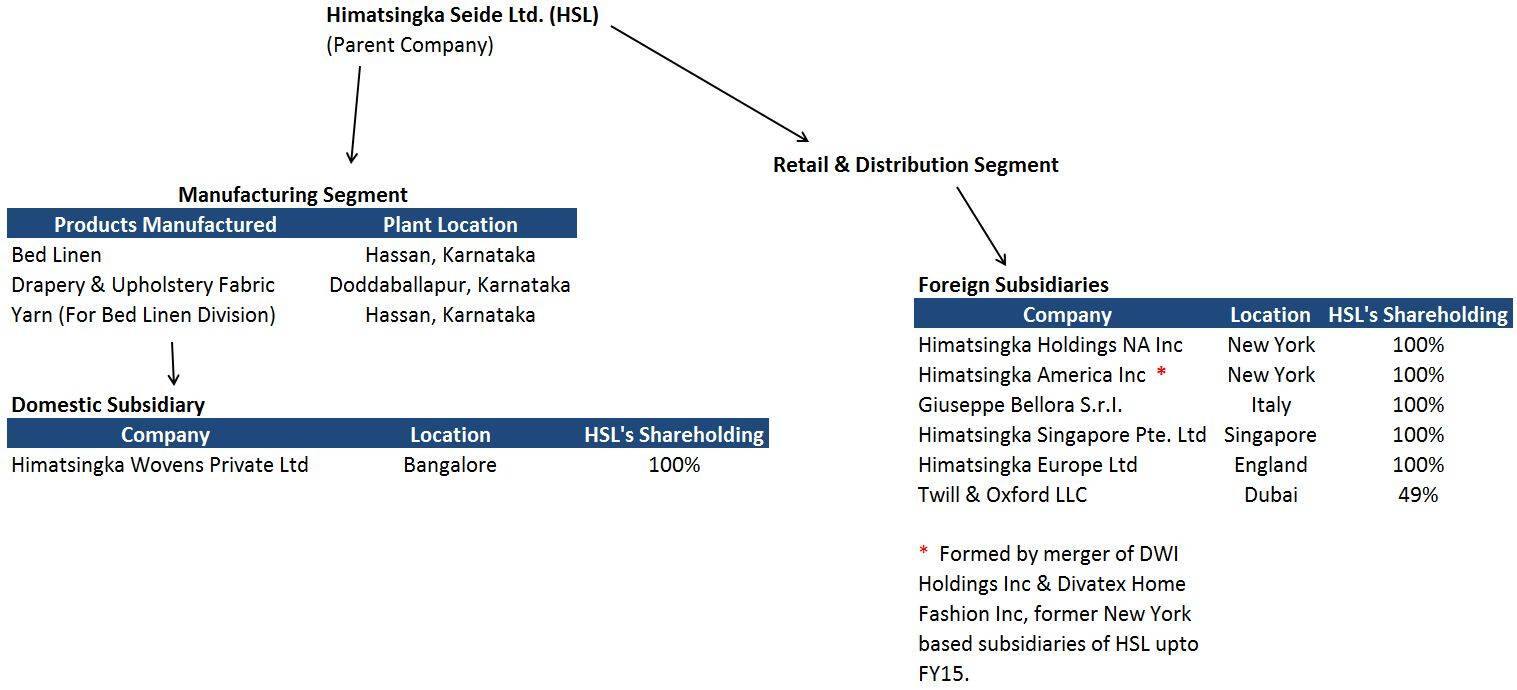

BackgroundIncorporated in 1985, Himatsingka Seide (HSL) operates through two divisions - manufacturing, retail and distribution. On the manufacturing front, HSL is one of India’s leading manufacturers of bed linen products (bed sheets in particular), upholstery and drapery fabrics. The company’s retail & distribution arms cater to diverse requirements of varied clientele across North America, Europe, and Asia through branding activities and private label programmes.

While the stock has had its fair share of success in terms of financials and price returns, we continue to like quite a few moats that it offers.

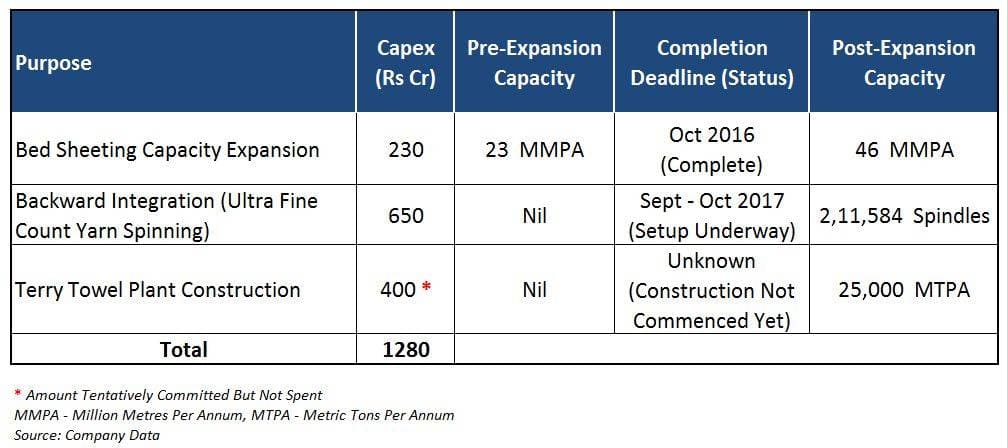

Capex Plan & Sheeting Capacity Expansion

The expanded sheeting capacity (23 mmpa), should see utilisation improving from 35-40 percent during Q3 & Q4FY17 to 50 percent in FY18, and close to 60 percent by end of FY19.

The additional output will meet the steadily rising demand from clients in the North American & European regions, where HSL already has its front-end offices established.

Moreover, the company is working towards increasing the percentage contribution of fashion bedding products, which command superior value over the non-fashion types and are margin-accretive, too.

HSL’s yarn manufacturing unit is likely to be fully operational by the end of Q3FY18, thus reducing the dependence on outside suppliers for yarn inputs by approximately 50 percent.

The entire yarn output will be captively consumed for manufacturing sheeting products, thereby saving raw material costs.

Since the company’s focus is on manufacturing ultra high count yarn (whose realisations are superior compared to the basic variants), the new spinning unit would facilitate better pricing per unit of the final product (i.e., bed sheets) as well, consequently causing EBITDA margins to expand.

Asset-Light Nature of Retail BusinessThe retail & distribution segment of HSL supplies home textile products to reputed retailers (mainly in North America) and high-end exclusive brand/multi-brand/departmental stores (in Europe and Asia) through over 7000 points of sale globally.

The company’s Karnataka-based manufacturing facilities supply bed linen products and drapery/upholstery fabric material periodically to the respective offshore subsidiaries, thus saving logistics and storage costs, while simultaneously ensuring working capital efficiency.

Reduction in Outsourcing from Third Party SuppliersCurrently, out of HSL’s sales effected through its retail channels abroad, about 40-45 percent of the output is sourced from external parties, whereas the rest is procured from the manufacturing units in India.

With the new sheeting capacity now functional, HSL’s international subsidiaries would be able to sell a higher percentage of the company’s domestically manufactured sheeting output without the need to incur substantial promotion costs since the distribution channels are already in place. Eventually, the retail segment’s operating margins are projected to inch up to 6 percent or more from the current level of 4-4.5 percent.

Brand LeverageHSL’s licensing agreements with some of the world’s leading retailers enable it to leverage its supply network optimally and enhance the shelf life of its products in a highly competitive environment. Buoyed by the optimism, the company targets achieving sales of Rs 1200 crore from the brands business by end of FY18, ie. around 50 percent of the overall annual turnover.

US’ annual home textile market, worth roughly USD 28-30 billion, constitutes nearly 40 percent of the world’s market size of USD 70-75 billion, and continues to grow by the day.

India’s share of home textile exports to the US has grown from 17 percent in 2008 to over 35 percent in recent years, most of it at the expense of the Chinese competitors.

In the US, the organised retail entities (HSL’s primary customers) have been playing a prominent role in reaching out to the masses across all states, and this trend is unlikely to change anytime soon.

However, HSL’s overdependence on the US clients exposes it to a concentration risk. A strong rupee vis-à-vis the US dollar could also hurt performance.

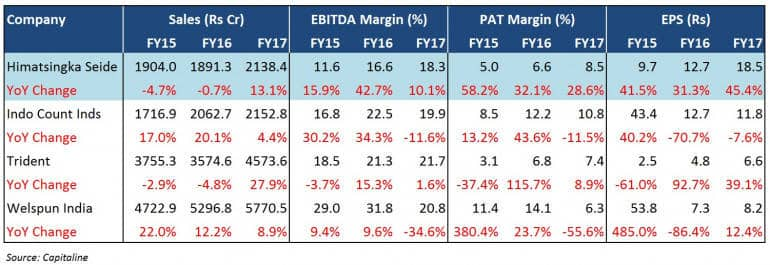

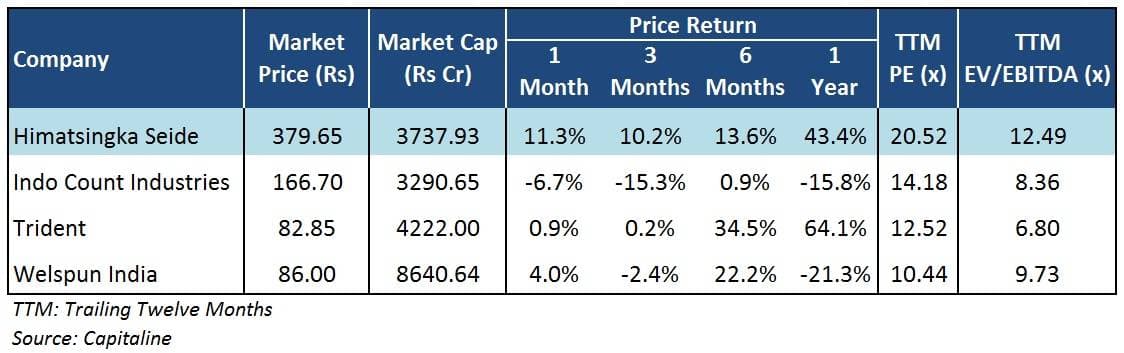

Peer Comparison & Valuation

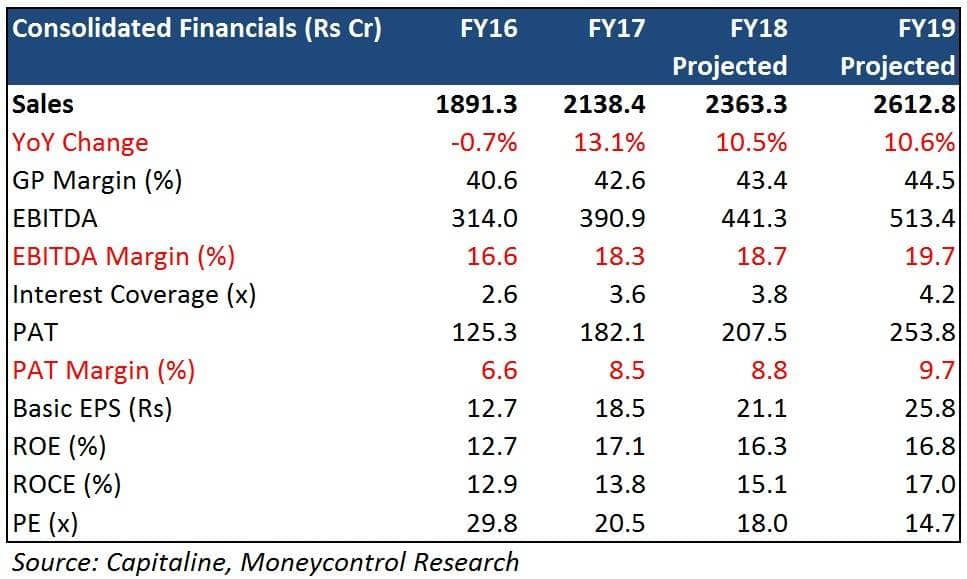

Prima facie, though HSL’s valuations seem expensive versus its peers, a closer look at the key parameters of the company underscores the fact that the stock has been rewarded by way of multiple rerating for its consistency over the years. At 14.7x FY19 estimated earnings, HSL is surely a stock you wouldn’t want to overlook.

Follow @krishnakarwa152Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.