Krishna Karwa Moneycontrol Research

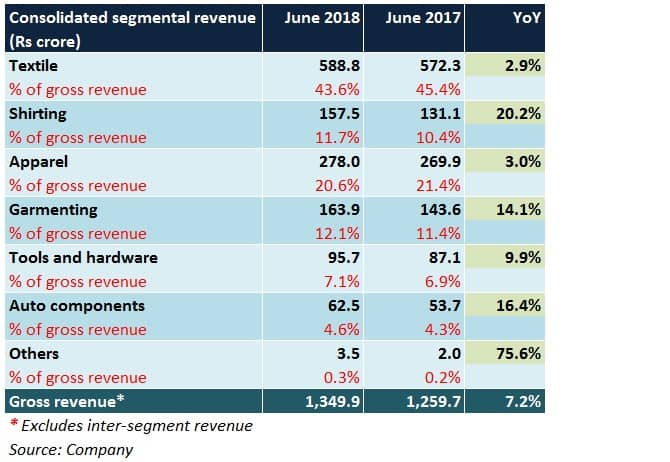

Raymond is one of India’s leading branded fabric and apparel manufacturers. The company’s six segments include branded formal wear fabric (Raymond Fine Fabrics, Raymond Made To Measure), branded high-value shirting fabric, branded casual cum semi-formal apparel (Raymond, ColorPlus, Parx, Park Avenue), garmenting (formal wear garments manufactured only for export markets), tools cum hardware components, auto components and fast moving consumer goods (wellness products and shampoos).

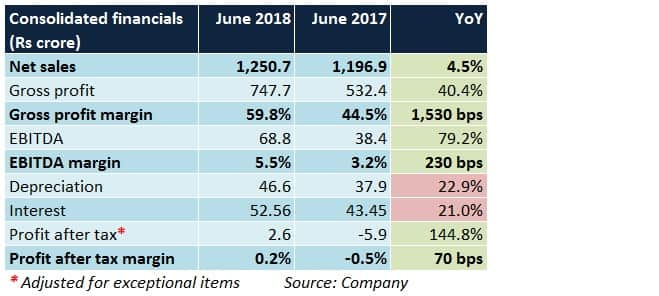

At the consolidated level, sales growth was subdued during Q1 FY19 due to a high base effect. Implementation of the Goods & Service Tax from Q2 led to preponement of purchases in Q1 FY18 in the branded fabric and apparel segments, which jointly comprised 64 percent of the quarterly sales.

However, margins improved because of lower advertisement spends, cost control initiatives and a noticeable turnaround in the branded apparel segment (constituting 20-25 percent of quarterly revenue) on the profitability front.

What lies ahead?

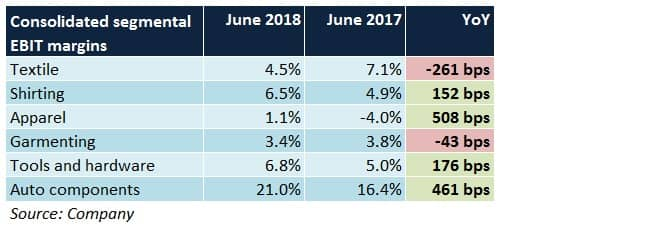

Textile (branded fabric) On account of a steep rise in raw material (cotton and wool) prices, margin in this segment may remain under pressure, particularly in Q2 FY19. As demand revives in H2 FY19 (wedding and festive season), increase in sale volumes and higher realisations could possibly offset this disadvantage.

Tie-ups with tailors across the country, availability of products with innovative features and product extension strategies (such as ceremonial wear) should provide an additional fillip to demand since it aids personalisation and facilitates a better connect with buyers, both present and prospective.

Branded apparel Spends on marketing/brand building and product launches are anticipated to pick up pace during the course of the year, thus ensuring adequate revenue visibility. As the brands mature and become capable of sustaining the momentum, advertisement expenses will normalise. This, in turn, should cause margins to inch higher.

New segments such as premium ethnic wear (Ethinix), khadi (Khadi by Raymond) and value-for-money wear (Next Look) are evolving simultaneously.

Shirting fabric Economies of scale by virtue of improved machine utilisation rates at Raymond's linen fabric factory at Amravati (the unit became functional in Q3 FY18, capacity: 4.8 million metre per annum) should lead to operating leverage, consequently resulting in margin accretion.

On similar lines as the branded fabric segment, increased activity in this segment should be visible in the second half of the fiscal year.

Network expansion To keep rental costs low and asset turns high, emphasis will be laid on increasing the number of mini ‘The Raymond Shop’ outlets from the present count of 101 (spread across more than 80 Tier IV and V towns pan India). About 70-80 percent of the proposed 200 mini ‘TRS’ stores to be added by FY20-end will be through the franchise route.

Garmenting In mid-FY18, Raymond commenced manufacturing of formal wear garments (jackets, trousers, shirts) for men at its Ethiopian facility, which has a capacity of 2.6 million pieces per annum. The rationale behind the move was to enter the European and US markets at zero rate of duty besides taking advantage of low costs and subsidies in the African nation.

Auto components Domestically and globally, the automobile industry has been growing at a brisk pace. Raymond, through its business relationships with leading names, has managed to strengthen its order book and maintain margins as well. Going forward, traction in this segment seems robust.

Tools and hardware The turnaround story in this segment appears to be playing out well for Raymond. This is evident from the steady run in margins since the past few quarters.

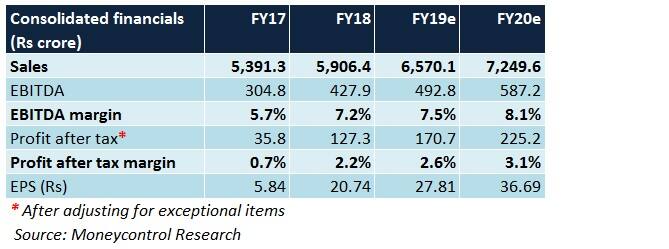

Should you invest? Completion of a major chunk of the capex cycle in FY18 (linen shirting fabric plant at Amravati and export-oriented garmenting facility at Ethiopia), increase in utilisation levels at these units, store expansion in smaller cities and a seasonally strong second half of the year should bolster Raymond’s earnings in due course.

Product premiumisation and differentiation holds the key to survival and success in an otherwise commoditised textile industry, where there are no barriers to entry. Raymond, undoubtedly, has been at the forefront in this regard by establishing itself strongly as a brand over the years. The company’s products enjoy a good recall too.

Nonetheless, risks associated with the inability to pass on high input prices to consumers (given the stiff competition), a high degree of dependence on menswear products, unforeseen changes in fashion-related trends and delays in monetisation of the Thane land bank could impact profitability and cash flows.

A steep drop in Raymond’s stock price provides a great opportunity to take advantage of industry positives that could benefit the company in the long-run. These include growing discretionary spends pan India, increased preference towards branded clothing and GST-induced economy formalisation.

At a modest post-correction valuation of 21.8 times FY20 projected earnings, the stock is worthy of consideration.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.