Swapnil Pawar

The suspension of six debt fund schemes of Franklin Templeton AMC earlier this year left a lot of investors in shock. Particularly surprising inclusions in the list of suspended schemes were Franklin’s Ultra-Short Term Bond and Low Duration funds. Even before the suspension of schemes happened, many investors were starting to get wary of Franklin’s Credit Risk and Income Opportunities funds. The ones that stayed invested, presumably, understood that these funds carried credit risk. On the other hand, very few investors in the Ultra-short-term Bond Fund and Low Duration Fund expected these to carry significant risks.

The hunger for yields and the rush for short-term commercial papers

Indian debt markets are in the early stages of their evolution. There are very few issuers other than the government/PSUs and even these are typically financial firms – banks and NBFCs (non-banking financial services). The liquidity in non-sovereign bond markets had started to increase in recent years. However, this increase was deceptive. Mutual funds were not just the beneficiaries of this increased liquidity, they were the cause. In general, this would have been a positive development. However, given the relative lack of risk awareness amongst debt mutual fund investors, this led to an unexpected problem – the self-reinforcing loop between bond fund inflows and issuance of short-term commercial papers by NBFCs.

In moderation, this would have been fine. However, taken to its extreme, it caused a significant distortion in the balance sheets of NBFCs – that lent for much longer tenors than the duration of their borrowings. This state of affairs could only go on as long as the mutual funds kept getting inflows. Such an arrangement was always going to be living on borrowed time.

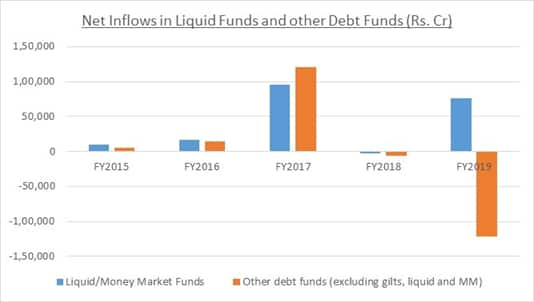

The below graph shows the jump in net inflows in debt funds in FY2017 vs FY2016. This was followed by a quieter FY2018. FY2019 was marked by net outflows from other debt funds as investors started seeing the extra risks in these funds.

The major driver for this rush to investing in commercial papers was the rush for yields from debt fund managers – who in turn were driven to them by competition, based purely on returns. One may think that investors would have paid heed to the risks in these mutual fund schemes. Unfortunately, they did not!

Mistaking liquidity for good credit quality

There is a large market for parking of funds for the short term. Unlike equity or credit risk funds, this market spans a much wider range of investors – including not only individuals and family offices, but also corporate treasuries and other institutional investors. The unstated primary requirement of this group of investors is a high level of liquidity. Most of these investors also want to minimize credit risks.

Competition amongst AMCs to gather assets in their debt funds led to the rapid rise of ultra-short term and low duration funds. Technically, these funds do not claim to be free from credit risk. However, the way they are sold in most situations does not stand by this technicality. Most of the investors were told by their advisors that ultra short-term and low duration funds had ample liquidity and low duration (by definition). This part was true. What was generally left out of a typical pitch was how risky these funds were vis-à-vis their counterparts among liquid or overnight funds.

If one mistakenly assumes that the credit risk is the same across liquid and ultra-short term funds, it seems obvious to prefer the latter. That is what most investors did. They assumed that if something is liquid enough, it is also presumably low on credit risk. The papers that most of the UST funds and low duration funds invested in were quite liquid. For a typical investor in these funds, this meant she could exit if some trouble arose. This strategy, however, does not work at the aggregate level, as the investors in Franklin’s debt funds found out!

Significant difference in credit risk between liquid and UST funds

Part of the reason many investors ignored the difference in the credit risk of UST funds and liquid was that a bottom-up risk analysis of the portfolio of a debt fund scheme is a complex task. The good reputation of the AMC and preliminary research done by advisors were typically considered enough by investors.

Let us look at how the credit risk levels compare across UST funds and liquid funds for the largest of these funds. The following graph shows the credit quality measured on a scale of 0 to 5 (5 being the best credit quality in debt fund universe and 0 being the worst) for various UST funds and liquid funds of the same AMC.

The average credit quality score for these UST funds is around 1.7 out of 5. The same score for liquid funds is around 2.9 out of 5. This is to be expected since UST funds target higher returns. The average YTM of these UST funds at present is 4.2 per cent while that of liquid funds is 3.3 per cent. However, most investors do not entirely appreciate this difference and end up comparing funds across these categories purely on the basis of returns, assuming they are broadly in the same risk bucket.

Match the fund selection to your objective

A higher credit risk in UST funds doesn’t mean they are not suitable for investment. It only means investors should be aware of the extra credit risk they are taking for the additional returns when compared with liquid funds or bank fixed deposits. In general, a UST fund is recommended if someone wants to keep moderate level of liquidity in her holdings, but is fine with some credit risk. If the tolerance for credit risk is very low (e.g., for a corporate treasury with a board mandate to take no risk at all for short term parking of funds), it is best to avoid UST funds and stay with overnight or liquid funds.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.