Be careful what you wish for, it is said, for it might just come true! This is exactly what has happened to Indian taxpayers. For long, they have demanded a simplified tax regime with liberal slabs and lower rates. In Union Budget 2020, Finance Minister Nirmala Sitharaman has acceded to the demand, but with a caveat: to take the ‘simplified’ tax structure, you will have to let go of a host of exemptions and deductions offered so far.

The current income-tax regime and the new one will exist simultaneously, with the option of choosing between the two. You, the taxpayer, will now have to decide which one works for you. Ironically, the ‘simpler’ tax regime comes with embedded complications, triggering confusion rather than a sense of relief. Here is a five-point guide to making the right choice.

Plan ahead to take an informed callThere is no single answer to the ‘switch or stick’ question. And, it doesn’t just depend on your income or salary structure. You also need to look at your investment habits, your age, life-stage, goals, responsibilities and likely expenses. You will have to plot your actual income and deduction figures to decide whether to switch or not.

Also Read: Income Tax Calculator: Know your post-Budget 2020 tax liability as per new income tax slabs

For example, if you are a young individual and dislike paperwork, and claim little or no tax-saver benefits, the new regime might sound inviting. Forgoing these tax benefits to ensure more money in your hands will not be a difficult choice to make.

However, for those who do take multiple tax breaks, the older regime will help save more on taxes.

Also Read: Budget 2020: Should you switch to the new income tax slabs?

Therefore, financial planning is now more critical than ever. Start planning right away to be prepared to take a call before your employers ask you to submit your proposed investment declarations, from the April of every year. Your employer deducts your tax from your salary through the year on the basis of the indicative declarations you make. Even those who have documentation-phobia will have to put themselves through this process at least once. “Salaried tax-payers have the option of switching between the regimes, something that those who draw business income do not have. So, if you are a salaried individual, you can always change your course next year,” says Ameya Kunte, Founder, Globeview Advisors, a tax consulting firm.

Financial advisors are unanimous in their opinion: the older regime is better for most if you have been availing of multiple tax benefits, mainly those that give you an impetus to invest, such as section 80C and 80CCD tax benefits. “In most cases, the old regime will turn out to be beneficial. Only those who did not make an effort to invest in section 80C’s avenues and avail of other deductions or could not utilise this Rs 1.5-lakh limit due to higher expenses could find their tax outgo going down in the new regime,” says Pankaj Mathpal, a Mumbai-based financial planner.

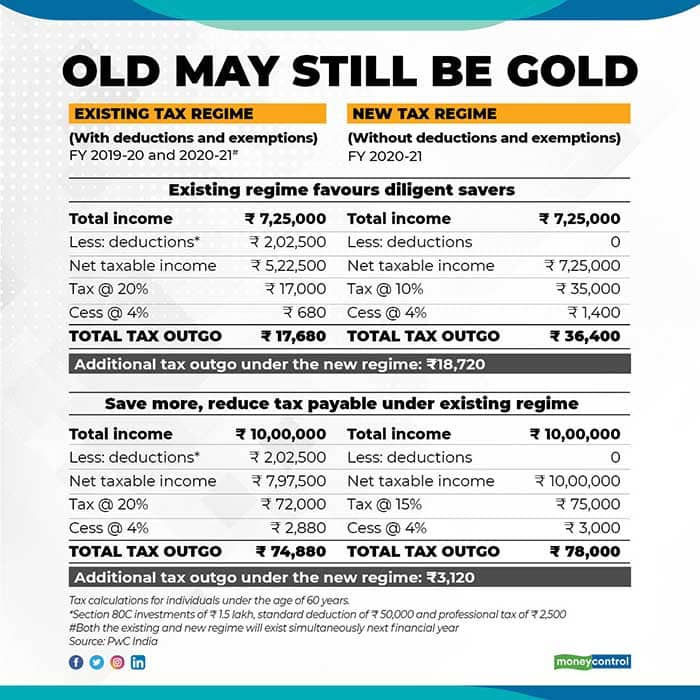

For example, if your total income is Rs 7.25 lakh or Rs 10 lakh and you take 80C benefits and standard deduction, your tax outgo will be lower by Rs 18,720 and Rs 3,120 respectively in the old regime vis-à-vis the new one (see 'Old may still be gold').

Those earning say Rs 15 lakh could save Rs 14,820 in the new regime.

However, most individuals also utilise other benefits apart from the section 80C. For instance, house rent allowance (section 10), home loan interest paid of up to Rs 2 lakh (section 24B), health insurance premium paid of up to Rs 25,000 for those under 60 (section 80D), NPS contribution of up to Rs 50,000 [section 80CCD(1B)] help a great deal in bringing down the taxable income. So, if you earn Rs 15 lakh and also pay a home loan interest of Rs 2 lakh, besides claiming standard deduction and section 80C tax deduction benefits, you will be poorer by Rs 47,850 in the new regime. Put simply, the higher the number of deductions and exemptions, the better it is for you to stick to the old regime.

“Many deductions are of a recurring nature. Why would you want to stop availing of these benefits by switching to the new regime?” asks Mathpal. For example, your provident fund contribution, eligible for tax break under section 80C, is a mandatory deduction made from your salary every month. You cannot turn the tap off. Any investment in public provident fund (PPF) also has to be made for 15 years. If you claim deduction under section 24 (b) on housing loan interest paid, you will be incurring this expense over the home loan tenure, which could extend to 30 years.

Homi Mistry, Partner, Deloitte, though said in an earlier interaction with Moneycontrol that even if you opt for the new regime, you can still continue your investments in the typical Section 80C compliant investments. Just that the tax benefits will not accrue to you, if you choose the new tax regime. However, clarity is awaited here if, say, you have invested in a public provident fund and the interest here is tax-free. Will the interest continue to be tax-free if you choose to switch to the new regime?

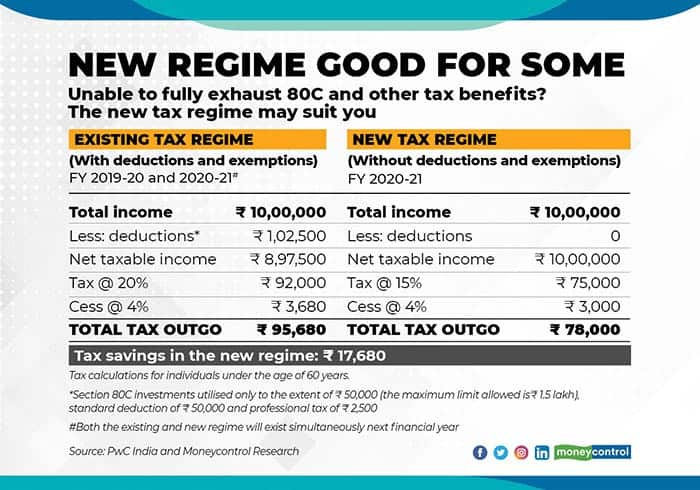

Do not ignore long-term savingsFor millennials or those in their first or second job and claiming minimal tax benefits on account of relatively lower PF deduction, the prospect of moving to the new regime might seem interesting. After all, it will be easy to let go of lower eligible deductions as also avoid the pressure of investing more to claim higher tax breaks. They could be left with more money in their hands, besides bidding goodbye to paperwork (see 'New regime good for some').

That doesn’t mean it’s okay for the young to not save. The urge to splurge this additional disposable income could mean indiscriminate spending, especially through credit cards. Not only can it lead them into a debt trap, but lack of savings can also hamper their financial future. Absence of any push to save will be a highly negative fallout from the new tax regime proposal, feels financial planner Gaurav Mashruwala. “Individuals by nature will not save unless you force them to. The tax deductions are one way of getting them to save for their future. Increasing consumption should not come at the cost of savings. I do not recommend anyone to switch to the new tax regime,” he explains.

On the positive side, however, forgoing section 80C will eliminate the possibility of any taxpayer falling prey to insurance agents’ sales pitches for low-yielding endowment policies. Disciplined investors can always look at equities for long-term goal planning.

NPS gets the edge nowThe new tax regime does get one tax benefit, though. That’s the national pension system (NPS). In her Budget speech, finance minister Nirmala Sitharaman said that nearly 70 exemptions and deductions will be removed from the new tax regime, out of over 100. There are some tax benefits that escaped the axe. Employers’ contribution to the NPS that is deductible from your salary under section 80CCD(2) is one such tax break. The deduction limit is 10 per cent of your basic salary plus dearness allowance. Whether you choose the old regime or the new one, ensure that you enquire whether your employer offers this option and take the same.

Choose your charity with careOne of the deductions you can presently claim is on donations made to charitable institutions. Based on the organisation, you can claim 50 or 100 per cent of the amount donated, under Section 80G. The pain point for taxapayers has been in claiming the deduction, as donors had to preserve the receipt after the financial year. This was because he/she had to quote the details such as the receipt number, charitable institution’s address, PAN and the amount donated in the tax-return form.

Budget 2020 has eased the process a bit. Now, the income-tax department will directly get your donation details from charitable organisations and mention the details beforehand in your income-tax form. In simple words, your income-tax form will come pre-filled with your donation activities. An essential condition here is that the charitable institution needs to be registered with the IT department and should have obtained a unique registration number. If you make a donation, ensure that your charitable trust has completed this process.

(Khyati Dharamsi also contributed to the article)

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.