How do you remain financially independent even as you live well into your 70s and 80s? That is, you live nearly two decades after your retirement. The Rs 25 trillion Indian mutual funds industry seems to have a solution. In recent years, many fund houses have launched schemes that target retirement savings.

Life expectancy of Indians has gone up to 68.56 years in 2017 from just 41.17 years in 1960, according to World Bank data. If the trend continues, present-day Indians are likely to live longer than the previous generations.

Last week, the Axis Retirement Savings Fund was launched. The scheme offers three plans to investors – aggressive (up to 65 per cent in equities), dynamic (up to 100 per cent in equities) and conservative (up to 40 per cent in equities) plans. The new fund offer closes on December 13. Of course, there are many other fund houses that have been offering retirement schemes for years now.

Should you consider investing in retirement funds? And are they any better than equity funds, which too are meant for long-term savings?

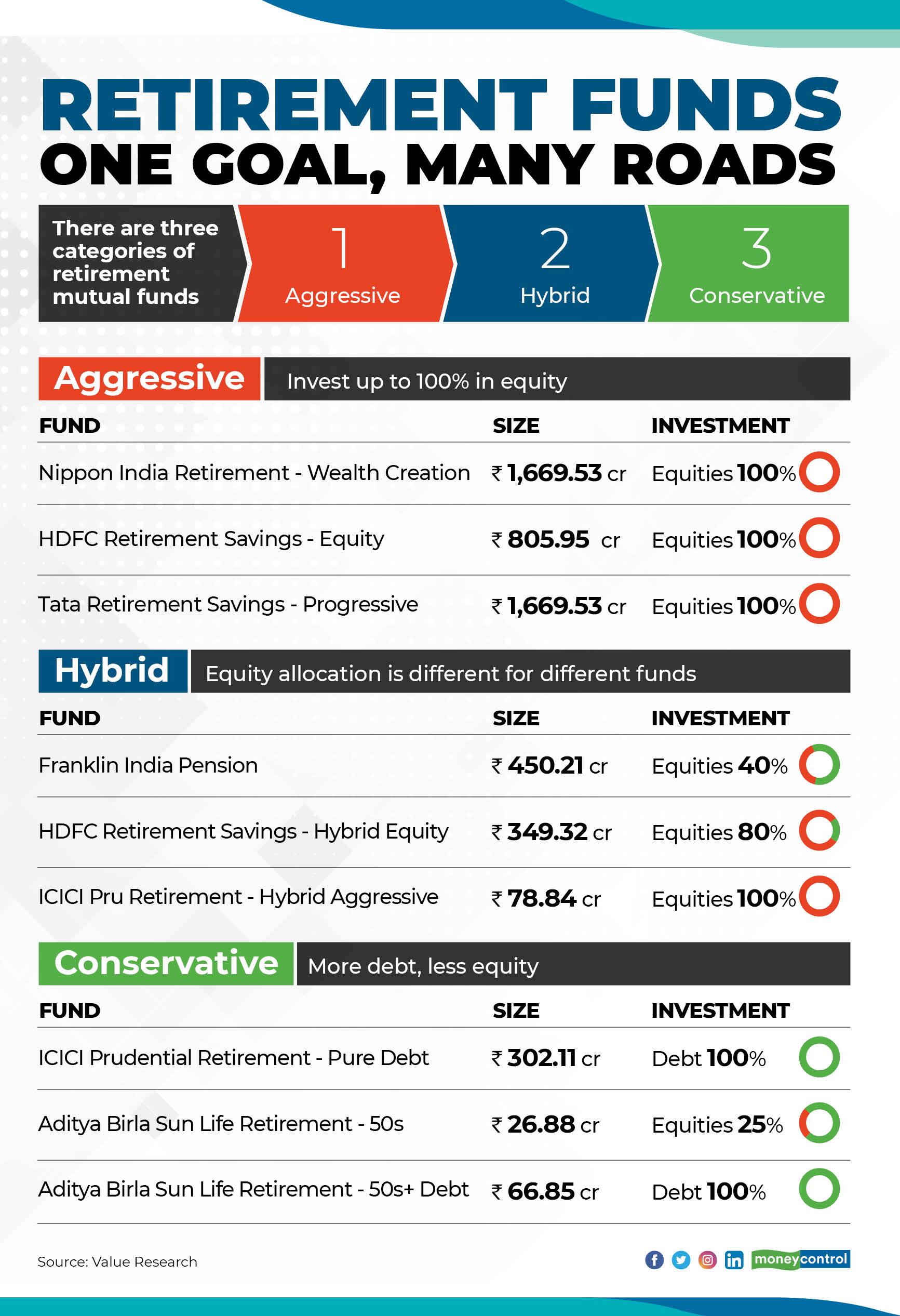

Retirement mutual fundsFinancial planners often advise investing in equity funds as the chosen vehicles to plan for your retirement. Now, mutual funds have in the past launched schemes specifically designed to help you save for your retirement. Called pension or retirement funds (not to be confused with the pension plans offered by life insurance companies), these schemes invest in a mix of equity and debt instruments. For many years, there were just Franklin India Pension Fund (started in 1997) and UTI Retirement Benefit Plan (rolled out in 1994). In recent years, many more have jumped into the bandwagon.

To ensure that investors stick around till their retirement, these funds impose high exit loads if you redeem before attaining retirement age, in addition to the compulsory lock-in of three years. A tax deduction benefit under Section 80C helped incentivise investors to stay put.

In 2017, capital market regulator, SEBI, carved out a separate category for retirement funds. So far, fund houses such as Aditya Birla Sun Life, HDFC, ICICI Prudential, Nippon India, Principal and Tata have launched their retirement funds.

“SEBI’s categorisation rules have standardised the lock-in to five years or till retirement age, whichever is earlier,” said Abhishek Gupta, founder and managing director of Moat Wealth Advisors. However, they differ from each other due to varying asset allocation policies, he added. While the offerings of Franklin and UTI have only one plan, the new entrants have consciously offered multiple plans catering to investors with varying risk appetites.

The retirement funds of Franklin India, UTI, Tata, Nippon India and HDFC offer section 80C tax deduction benefits of up to Rs 1.5 lakh. Recent schemes rolled out by various fund houses do not enjoy the tax benefit.

Investment strategyFranklin India Pension Fund and UTI Retirement Benefit Plan invest up to 40 per cent in equities. ICICI Prudential Hybrid-conservative plan and Tata Retirement Savings Fund-conservative plan invest a significant chunk of their assets in debt securities, with and up to 30 per cent parked in equities. HFDC Retirement Savings Fund-Equity Plan and Nippon India Retirement Fund Wealth Creation Scheme invest up to 100 per cent in equities.

Even within their broad asset allocation strategies, they aren’t strictly comparable. For example, HDFC Retirement Savings Fund– Equity Plan has seen its equity exposure ranging between 79 per cent and 87 per cent over the last two years. Nippon India Retirement Fund Wealth Creation kept its equity allocation between 90 per cent and 97 per cent, over the same period, according to Value Research data. Both funds are allowed to invest up to 100 per cent in equities.

ICICI Prudential Retirement Fund-Pure Equity Plan has been investing predominantly (more than 90 per cent of the assets) in large-cap stocks. Aditya Birla Sun Life Retirement Fund-The 30s Plan, has invested around 40-45 per cent of the money in large-cap stocks and the rest in stocks of mid and small-sized companies. These schemes were launched in March and February 2019, respectively.

Tata AMC’s Retirement Saving Fund also prefers to have a large cap bias. “A multi-cap equity portfolio dominated by large-cap stocks works in favour of investors. Globally large companies are becoming larger and India is no different. Investing in large-cap stocks also makes it easy to take corrective steps or to restructure the portfolio whenever required,” said Sonam Udasi, senior fund manager, Tata AMC.

Retirement funds or equity schemes?Most individual investors prefer ‘mental accounting’ when they are saving for specific financial goals. A public provident fund for their retirement corpus, a mutual fund investment to finance their child’s education, a fixed deposit to pay for their next holiday and so on. “The mental accounting or bucketing brings in passion to achieve the goal envisaged and ensures that the individual does not liquidate that investment for any other purpose,” said Amol Joshi, founder of Mumbai-based Plan Rupee Investment Services. “But if you think you could do with a nudge, then retirement funds help since they come with a lock-in feature,” Joshi added.

“A retirement fund serves as a dedicated investment option for individuals to fund their retirement. It brings in the much-needed discipline in the way individuals approach this goal,” said Chandresh Kumar Nigam, MD & CEO, Axis Asset Management Company. These schemes with longer lock-in period compared to tax saving schemes can bring in much required patience. “The five year lock-in ensures that in most cases the investors have a positive experience with their investments and they add regularly to their investments in these schemes leading to a large corpus in the long term,” said Valmiki Khatri, Partner, Krushna Finserv LLP.

The problem with retirement funds is the lack of a track record. Except Franklin India Pension Fund and UTI Retirement Benefit Plan, most of these funds are new. Besides, they aren’t strictly comparable due to different strategies.

“Investing in open-ended funds allows you rebalancing, which is not the case in retirement funds since there is a lock-in,” points out Joshi. He prefers open-ended equity hybrid, large-cap or multi-cap funds for retirement funding.

“Investing in equity oriented retirement fund with a long term view should help investors to outperform the inflation and the fixed income returns handsomely,” said Sonam Udasi.

Gupta says that there is nothing unique the retirement funds offer that open-ended schemes do not offer. “If you are a disciplined regular investor and understand the importance of achieving your financial goals, you can instead invest in open-ended multi-cap or aggressive equity hybrid funds,” said Gupta.

While retirement funds gather a track record, stick to diversified equity funds for now to build a sufficient retirement kitty.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.