Soon, you will be able to pay your health insurance premiums in instalments instead of an annual lump-sum, as is the case currently, given that medical policies are yearly contracts.

The Insurance Regulatory and Development Authority of India (IRDAI), in the backdrop of financial crunch that many are facing due to the novel Corona Virus Disease (COVID-19), allowed insurers to also offer monthly, quarterly and half-yearly premium payment modes to customers. This will help policyholders who would have otherwise let their policies lapse due to lack of funds to keep them in force at a time when they are critical.

Relief for policyholders

While the IRDAI had allowed insurers to offer these modes in a circular on minor modifications on certification basis issued in September 2019, they had to maintain a gap of 12 months between two such applications. Now, this provision has been relaxed for policies coming up for renewal up to March 31, 2020. Put simply, this means they can offer this option – either as a permanent feature or as temporary relief for 12 months – as soon as their IT systems are ready.

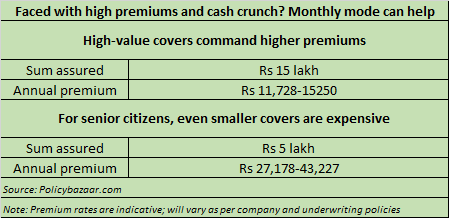

In COVID-19 afflicted times, when many are faced with job losses or pay cuts, the instalment payment plan seems like a lifeline. “This is particularly true if you have a high-value policy or are paying premiums for your parents’ health cover. Many buy policies to save on taxes and are likely to have a high premium outgo,” says Mahavir Chopra, independent health insurance expert. For example, a 40-year-old with a Rs 15-lakh health cover may have to shell out close to Rs 12,000 as annual premium. Likewise, if you are a senior citizen, annual premium even for a sum insured of Rs 5 lakh can be as high as Rs 30,000. During financial crises, such amounts are bound to seem daunting.

Tread with care

If you have a Rs 15 lakh cover that entails a premium of Rs 12,000 and is due in May, you can now choose to pay only the monthly instalment if your insurer offers the facility. “The IRDAI has given an option to insurers to offer this feature. We are trying to streamline our IT systems to facilitate it,” says Nikhil Apte, Chief Product Officer, Royal Sundaram General Insurance. Before signing up for the option, however, check the premium applicable. “There could be a minor difference, as reasonable loading of, say, 5-10 per cent, on the basic premium is permitted. For example, if your annual premium is Rs 12,000, the instalment under the monthly mode could be Rs 1,050 (so annual outgo will be Rs 12,600),” he explains. The call on loading the premium for higher frequency modes will be taken by individual insurers. Once you choose your premium payment mode, you will have to stick to it until renewal.

The emphasis here is on affordability. Choose non-annual modes only if the alternative is letting the policy lapse, which could be potentially disastrous in times of COVID-19. More employers are likely to extend such schemes now that home ministry has mandated such covers for employees of organisations that are allowed to function during the nationwide lockdown. But you must not let go of your individual policy even if you are already covered under your employer’s group insurance.

Claim conundrum

If you choose greater frequency in premium payments, the onus will be on you to ensure constant monitoring. “For instance, you could forget making the payment or the ECS debit might fail due to inadequate limit on your credit card or simply minor technical issues. In such cases, your policy will enter the grace period during which cover may not be available. Therefore, if you can afford to, stick to yearly payments,” says Apte. Currently, IRDAI has asked insurers to allow policyholders whose premiums are due till May 3 to pay premiums until May 15, so that claims triggered during the grace period, too, can be paid. However, this relaxation is confined to this specific period only.

Any premium payment mode other than the annual one can also give rise to complications at the time of claim settlement. Now, in the case of an annual payment, the insurer will simply examine the claim on its merits and approve or reject it. However, it will not be this simple in the case of other modes. “Every insurer will have to take a call on whether to adjust the balance premium instalments against the claim amount or not,” says Sanjay Datta, Chief, Underwriting, Claims and Reinsurance, ICICI Lombard.

Let’s say your policy start date is May 1 and you decide to switch to the monthly mode at the time of renewal. “Here, if you were to make a claim in August, the monthly premium due for the balance eight months (up to April) will be deducted from the approved claim amount before it is released,” explains Apte. To avoid such complications and possible heartburn reduced claim amounts can cause, go with annual premium payment option if you can afford it.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!