Consider this: You build a neat retirement savings kitty during your working years. You are confident that this corpus will last through your silver years. And therein lies the challenge: how do you ensure that your funds comfortably earn you a regular income and still last your entire life time?

You will have to deploy it efficiently so that the corpus lasts throughout your retirement years.

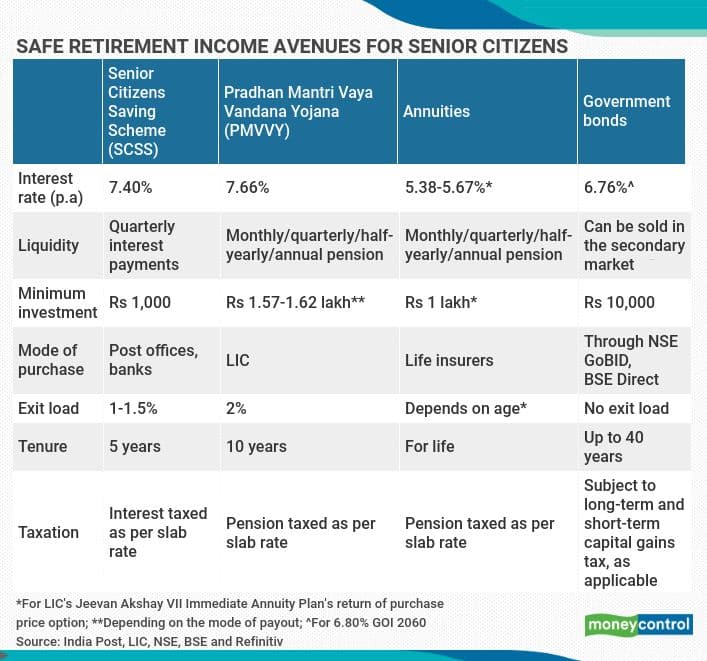

Here are some instruments that you ought to have in your portfolio to achieve this goal.

Senior Citizen Saving Scheme (SCSS)

One of the safest for senior citizens, it currently offers 7.4 percent per annum, with the interest being paid out quarterly. Since it is backed by the central government, the returns are assured, but it comes with a lock-in period of five years. You can invest up to Rs 15 lakh and rely on quarterly interest pay-outs for liquidity needs. Moreover, SCSS also offers tax deductions under section 80C. The SCSS interest rate is amongst the best on offer amongst debt instruments, despite the 120 basis points rate reduction in March. “We advise our clients to invest in SCSS before considering other options. The high and assured rate of returns make it a compelling avenue for regular income,” says Ashish Shah, Co-founder, Wealth First Portfolio Managers.

Pradhan Mantri Vaya Vandana Yojana (PMVVY)

Another product designed specifically for senior citizens, Pradhan Mantri Vaya Vandana Yojana (PMVVY) is offered by the Life Insurance Corporation of India (LIC). Like SCSS, you can invest up to Rs 15 lakh and it also promises a return of 7.4 percent. A government-backed scheme, it comes with no credit risk and a longer tenure of ten years, making it suitable for retirees. The scheme was to end on March 31, 2020, but the central government decided to extend until March 31, 2023 due to its popularity amongst retirees. However, the interest rate was slashed from 8 percent to 7.4 percent. Yet, it remains an attractive proposition for senior citizens, offering returns far higher than those of fixed deposits. For example, the State Bank of India’s (SBI) offers an interest of 6.5 percent to senior citizens for fixed deposits with tenures of 5-10 years.

Annuities from life insurance companies

Of late, annuity plans from Life Insurance Corporation of India (LIC) – Jeevan Akshay (VII) and New Jeevan Shanti – are being promoted heavily. This is how annuities work: if you were to purchase an immediate annuity plan, that is, invest a lump-sum in such plans offered by all life insurers, you will get a regular payout. “Broadly, if you invest a lump-sum now, you get regular payouts – be it monthly, quarterly or annually. The returns work out to 5.75-5.9 percent annually over 20-30 years,” explains Vikram Dalal, Managing Director, Synergee Capital.

Unlike PMVVY and SCSS, annuities offer guaranteed returns over a much longer term of 30-40 years, covering your entire retirement phase.

Now, annuities may sound like an answer to your quest for a long-term instrument capable of yielding assured returns. However, there are better-yielding, long-term avenues such as government securities that you must consider instead of annuities. The entire annuity income is taxable at the slab rate applicable to you.

Unless the annuities market develops further – especially given that 40 percent of your National Pension Scheme’s maturity at age 60 must be invested in an annuity – these are not your best options yet.

Government securities

Instead of annuities, financial planners recommend government securities. “Being a sovereign security, it is highly secure, and returns will be in the range of 6.6 to 6.75 percent. You can stay invested for 40 years (bonds with maturities till 2060 are also available). These work out better than annuities. You also have an option to exit, if the need arises. These bonds have semi-annual interest payments,” adds Dalal. The principal invested is safe as these are sovereign bonds. And, if held till maturity, you will not face any interest rate fluctuation risk either. “You must choose government bonds if fixed returns over the long term is your objective,” he adds.

While the process of investing in government securities was not easy earlier, now you can invest through NSE’s goBID platform. It is an online platform meant for retail investors who want to purchase treasury bills and Government of India Dated Bonds.

“You can invest in government securities through your stock brokers. The process is quite simple, but the awareness amongst retail investors is low. Moreover, the intermediaries do not earn much remuneration and hence do not promote this avenue,” says Shah. New investors who are clients of NSE trading members will have to register on the goBID platform. Next, you have to select the securities available for subscription, make an online payment from a bank account linked to your demat account. The allotted bonds will be credited to your demat account. “Government bonds, including state development loans, score over annuities in terms of returns. Also, you can pledge these securities to raise short-term funds, which is not possible in the case of annuities,” adds Shah.

Similarly, you can also invest through the BSE Direct platform. If sold within a year, gains made on sale of government bonds will be treated as short-term capital gains (SCTG) and taxed as per your slab rate. Beyond this period, gains will qualify as long-term capital gains (LTCG), and will be taxed at 10 percent.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!