As geopolitical tensions intensify across Middle East regions, volatility has returned to equity markets. Indian benchmarks mirrored the nervous mood on Dalal Street, with the Sensex and Nifty 50 witnessing correction. The Nifty 50 slipped 445.45 points to 24,723.20, while the Sensex declined 1,459.46 points to 79,827.73 at 14:30 IST on 2 March 2026.

In times like these, when headlines drive sentiment and global uncertainty fuels market swings, many investors begin to reassess risk exposure. The key question then becomes: should part of the portfolio be shifted toward safer, government-backed instruments that offer predictable and sovereign-guaranteed returns instead of riding equity volatility?

It is important to note that geopolitical tensions have historically led to a 5 to 10 percent fall in Indian markets, but recovery has followed within 3 to 6 months. “Historically, equity markets tend to react during geopolitical escalations. However, data suggest that the average equity market correction across conflicts has been with a median correction closer to 10.2 percent indicating that while volatility spikes, long-term impact is often limited. Investors should consider complementing equity with other stable asset class to maintain stability during uncertainties,” said Arjun Guha Thakurta, Executive Director, Anand Rathi Wealth Limited.

The best approach is to always diversify your portfolio and have a mix of both.

Let’s have a look at some alternative options to equities:

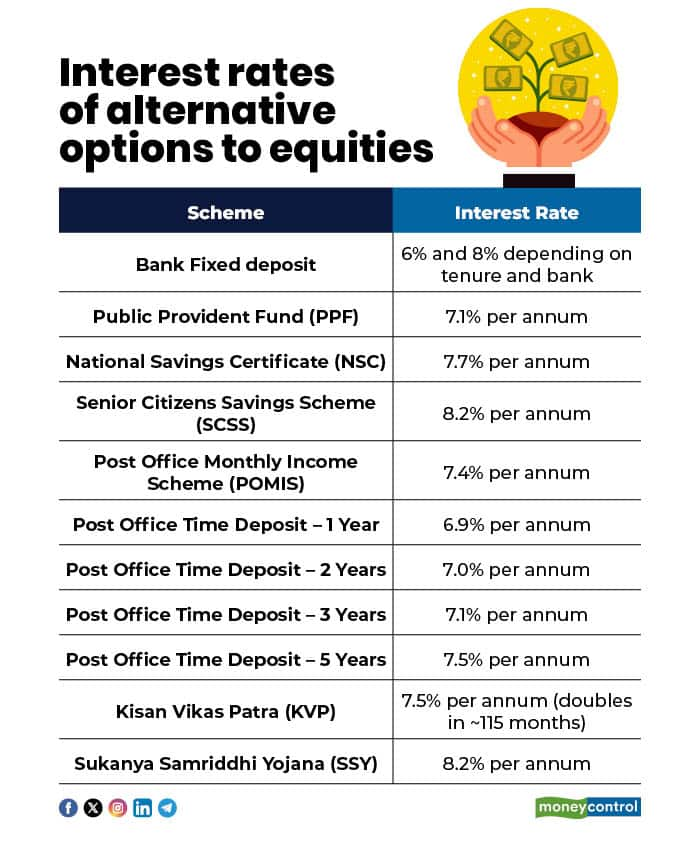

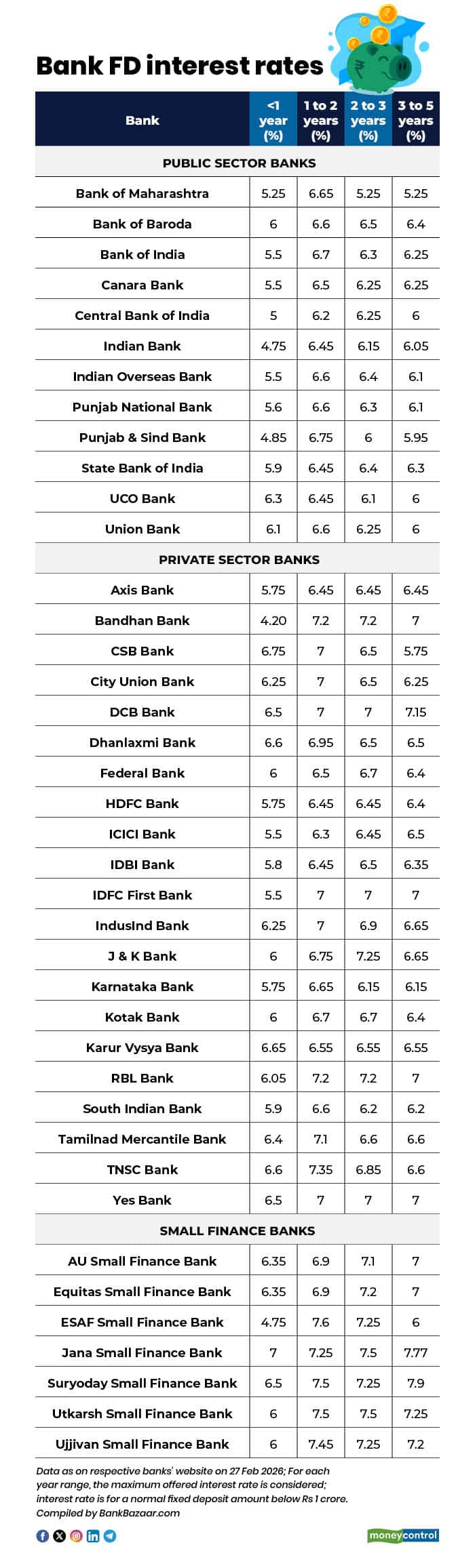

Bank Fixed Deposits (FDs)

Bank FDs remain a popular choice during uncertain times due to guaranteed returns.

Interest rates: Typically range between 6 percent and 8 percent depending on tenure and bank.

Senior citizens usually receive an additional 0.25–0.50 percent. While returns are taxable, FDs offer capital protection and predictable income.

Debt Mutual Funds

Debt mutual funds are investment schemes that mainly allocate money to fixed-income instruments such as government securities, corporate bonds, treasury bills, and money market instruments. These funds are available in multiple categories, from liquid and short-duration funds to gilt and dynamic bond funds, allowing investors to choose options based on their risk appetite and time horizon.

How Do Debt Funds Work?

Debt mutual funds generate returns by investing in interest-bearing securities such as government bonds, corporate debt, treasury bills, and other short-term instruments. The income earned primarily comes from interest payments and, at times, from capital gains when bond prices move favourably.

The net asset value (NAV) of a debt fund changes depending on interest rate movements and the credit quality of the securities in its portfolio. Typically, when interest rates decline, bond prices rise, which may push up the fund’s value. Conversely, when rates increase, bond prices tend to fall, affecting returns.

While debt funds are generally less volatile than equity funds, they still carry risks. Experts suggest investors should align the fund’s duration, credit quality, and overall risk profile with their financial objectives and investment timeline before investing.

Public Provident Fund (PPF)

PPF remains one of the most trusted government-backed tools for long-term, low-risk wealth building.

Current interest: 7.10 percent per annum

Tenure: 15 years, extendable in blocks of 5 years

The PPF account allows you to deposit up to Rs 1.5 lakh per person per year and claim a tax deduction under Section 80C. However, this benefit is available only under the old tax regime.

The government uses the recommendations of the Shyamala Gopinath Committee while determining the interest rate on Public Provident Fund (PPF) accounts. As per the committee’s framework, the PPF rate may be aligned with the average yield on 10-year government securities (G-Secs) in the secondary market during the previous quarter, with an additional spread of 25 basis points.

National Savings Certificate (NSC)

NSC is a post office savings certificate that combines fixed returns with tax-saving potential.

Current interest: 7.70 percent per annum

A minimum investment of Rs 1,000 is required to open an NSC account, and the lock-in period is 5 years.

Tax benefits of up to Rs 1.5 lakh are available under Section 80C of the Income Tax Act.

Senior Citizens Savings Scheme (SCSS)

SCSS is a government-backed retirement plan for individuals aged above 60 years.

Eligible individuals can invest a minimum of Rs 1,000 up to Rs 30 lakh for a period of 5 years, with an interest rate of 8.2 percent per annum.

The principal amount invested can be claimed as a deduction under Section 80C of the Income Tax Act up to Rs 1.5 lakh.

Post Office Monthly Income Scheme (POMIS)

POMIS is designed for risk-averse investors who want a monthly payout without market risk. Under this scheme, you can deposit a specified lump sum amount and receive monthly interest at a fixed rate.

You can invest up to Rs 9 lakh individually or Rs 15 lakh jointly, and the investment period is 5 years.

The interest rate is 7.40 percent per annum, payable monthly.

Post Office Time Deposit

It behaves like bank FDs but is fully sovereign-backed, which reduces credit-risk concerns compared with many NBFC FDs.

Current interest:

1 year: 6.90 percent

2 years: 7.00 percent

3 years: 7.10 percent

5 years: 7.50 percent

Tenure: 1, 2, 3, or 5 years

Investment: Minimum Rs 1,000; no upper limit.

Kisan Vikas Patra (KVP)

KVP is a long-term postal savings certificate meant for gradual, predictable wealth accumulation.

Current interest: 7.50 percent per annum, doubling in approximately 115 months.

Tenure: 115 months (approx. 9.5 years).

Investment limits: Minimum Rs 1,000; no upper limit.

Sukanya Samriddhi Yojana (SSY)

SSY is a girl-child-focused, sovereign-backed scheme aimed at long-term, tax-efficient education or marriage planning.

Current interest: 8.20 percent per annum, compounded annually.

Tenure: Until the girl turns 21 or gets married (whichever is earlier).

Investment limits: Minimum Rs 250 per year; maximum Rs 1.5 lakh per year.

Disclaimer: The views and investment tips expressed by experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.