As the financial year draws to a close, smart investors aren't just looking at their profits. They are also looking at ways to save their tax outgo. The best way to do this is through tax harvesting, a strategy that uses both gains and losses to keep the portfolio lean and efficient.

What is tax harvesting?

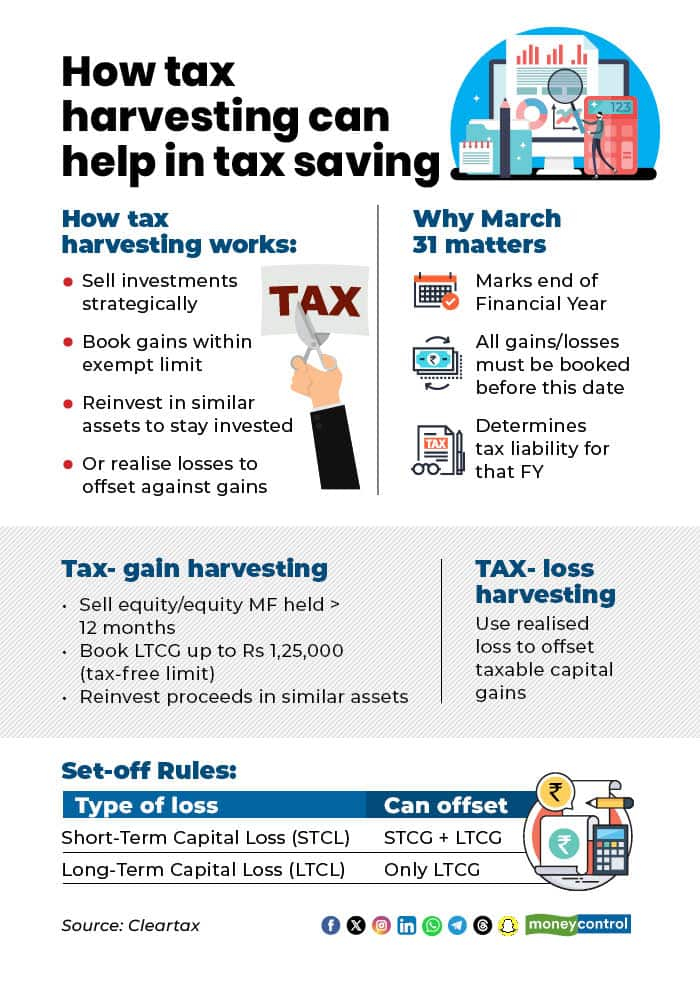

Tax harvesting is a portfolio strategy aimed at lowering the tax payable on capital gains, particularly from equities and equity mutual funds. It works by selling investments strategically, either to book gains within the exempt limit or to realise losses that can be adjusted against taxable gains.

At its core, tax harvesting is about proactive tax management. Instead of allowing gains or losses to build up unnoticed, investors plan transactions to reduce their burden while staying invested.

March 31 is critical for tax harvesting because it marks the end of the financial year, requiring all capital gains and losses to be booked by this date to calculate tax liability for that specific year.

Broadly, tax harvesting is of two types — tax-gain harvesting and tax-loss harvesting. Each is applied in different market situations and serves a distinct objective in improving post-tax returns.

Tax-gain harvesting

Tax-gain harvesting is a strategy where an investor sells equity shares or equity mutual fund units held for more than 12 months to book long-term capital gains (LTCGs) within the tax-exempt limit. The money is then reinvested, helping reset the purchase price and potentially reduce future tax liability.

Taxpayers should periodically review their tax position to optimise their capital gains outgo. “If no long-term capital gains are realised during the year, the annual exemption limit of Rs 1,25,000 may go unutilised. Therefore, a taxpayer may consider rebalancing the portfolio by realising long-term capital gains up to Rs 1,25,000 without attracting any tax liability,” said Gopal Bohra, Partner -Tax, NA Shah Associates.

Tax-loss harvesting

Tax-loss harvesting involves selling equity shares or equity mutual fund units at a loss. The realised capital loss can be used to offset taxable capital gains, thereby lowering the overall tax outgo.

Taxpayers who have already realised LTCG in excess of Rs 1,25,000 or have realised short-term capital gains (STCGs) may consider restructuring their investments where there are unrealised capital losses.

“Realising such losses can help reduce the tax liability on other capital gains. Short-term capital losses can be set off against both short-term and long-term capital gains. However, long-term capital losses can be set off only against long-term capital gains. Accordingly, taxpayers should evaluate and implement this strategy carefully and efficiently,” Bohra said.

In both cases, the goal is better tax efficiency, not timing the market or chasing higher returns. Tax experts suggest that taxpayers should avoid reinvesting in the same securities. This approach helps in rebuilding and strengthening the portfolio by exiting underperforming stocks and ensuring a genuine portfolio rebalancing. It also reduces the risk of unnecessary scrutiny from the tax authorities on the grounds that the transaction is a “colourable device” lacking commercial substance.

What are the steps one can use to gain tax harvesting?

Points to keep in mind while tax harvesting

The first step in tax harvesting is understanding the nature of your capital gains, whether they are long-term or short-term. The tax treatment differs significantly depending on the holding period and the applicable section.

“If the gains qualify as long-term capital gains under Section 112A (listed equity shares and equity-oriented mutual funds) and the total gains are within Rs 1.25 lakh, they fall within the exemption limit. In such a case, there may be no immediate need for tax optimisation,” said Chandni Anandan, Tax Expert, ClearTax.

It is equally important to understand the set-off rules for capital losses. A long-term capital loss can be adjusted only against long-term capital gains and cannot be set off against short-term gains.

On the other hand, a short-term capital loss is more flexible, as it can be set off against both short-term and long-term capital gains. Understanding this distinction helps investors plan their tax strategy more efficiently and minimise overall tax liability.

“If you do not have any capital losses, tax optimisation is still possible. Investors can sell Section 112A assets in a manner that the total long-term capital gains remain within the Rs 1.25 lakh exemption limit, and replan your portfolio in such a manner that the overall investment goals are met,” Anandan said.

While planning tax harvesting, one must also consider losses carried forward from earlier years. These losses can be set off against current-year capital gains as per the prescribed rules.

“Another important point relates to debt mutual funds purchased on or after 01 April 2023. As per Section 50AA of the Income Tax Act, 1961, such investments are always treated as short-term capital assets. Regardless of the holding period, gains or losses from these funds are taxed as short-term capital gains or losses,” Anandan said.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.