These are tough times for fixed income investors. Decreasing interest rates of bank FDs (fixed deposits) and a lack of safe bond options that provide reasonably good returns have meant that investors are left searching for alternatives. For example, State Bank of India has cut its one-year fixed deposit rate to 6.5 per cent from 6.7 per cent. Last week, ICICI Bank reduced the rate of interest on deposits with a one-year tenure by 10 basis points to 6.6 per cent. Non-convertible debentures issued by non-bank finance companies (NBFCs) and company fixed deposits come with their fair share of risks, especially the former, as has been evident from events in the past year or so. That makes the choice difficult. But there is a glimmer of hope if you can sacrifice a bit of liquidity and are ready to lock your money for some time.

The good-old National Saving Certificate (NSC) and Reserve Bank of India Saving Bonds (RBISB) look particularly attractive, offering a blend of returns and safety.

Interest rates have been declining steadily this year, in line with the policy announcements made by the Reserve Bank of India (RBI). Since February 2019, the RBI has cut the repo rate, the rate at which RBI lends to commercial banks, by 110 basis points. One hundred basis points make one percentage point.

The rates are expected to remain soft in the near term. “Inflation is below 4 per cent and the growth has slowed down to 5 per cent. If growth does not revive or slows down further, then the policy rates will go down from here substantially,” said Sujoy Kumar Das, head of fixed income, Invesco Mutual Fund. Low interest rates are good for borrowers, but not for depositors. So, they look for better alternatives.

Seventy five-year-old Dombivli resident Ramesh Chaugule recently invested in the National Saving Certificate. The retired music teacher lives a busy life as an active member of Jyeshth Nagarik Sangh – an organisation that works for senior citizens. “I prefer to invest some money in NSC, given the attractive rate of interest on offer compared to bank fixed deposits.”

He has invested in bank fixed deposits, postal savings and some high-quality corporate FDs. “Recently I heard about some companies not repaying their fixed deposit holders and we have seen the restrictions imposed on PMC Bank. I have to keep my money safe,” he adds. Though his monthly pension is adequate to fund his day-to-day expenses, he banks on his investments in NSC for big white-good purchases and gifting.

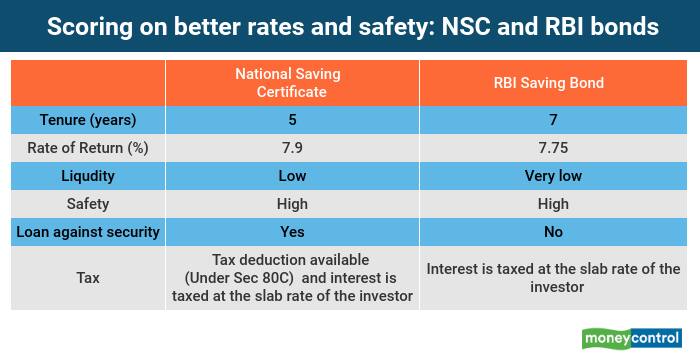

NSC offers a rate of interest of 7.9 per cent. Rs 100 invested becomes Rs 146.25 at the time of maturity at the end of five years. RBISB offers 7.75 per cent, payable half-yearly for the tenure of seven years. For every Rs 1000 invested in the RBISB, the maturity value for the cumulative option stands at Rs 1703. The rates offered by these two instruments is higher than those offered by five-year bank deposits. For example, SBI pays 6.25 per cent for fixed deposits maturing in the 5-10 years bracket.

The rates of small-saving schemes are reviewed quarterly. In the case of the NSC, the rates are locked/fixed at the time of investment. The contracted rate on the RBISB too does not change till it matures.

Return of capital, a concernThe safety of fixed income instruments has become a cause for concern to many bond investors. Many bond funds have witnessed defaults and, as a result, a fall in their net asset values. The default on debt obligations in large issuers such as Infrastructure Leasing & Financial Services and Dewan Housing Finance made many wary of investing in the fixed income space. We have seen many corporates defaulting on their loans. The recent instance of Altico Capital defaulting on its debt obligation has made investors believe that the worse is probably not behind us.

Return of capital has become a serious issue and there is a flight to safety.

“The investors need not worry about investments in NSC and RBISB, as they are backed by the sovereign. The rate offered on these investments is attractive,” said Joydeep Sen, founder of wiseinvestor.in.Low on liquidity

Both NSC and RBISB come with a fixed maturity and therefore your money gets locked in once it is invested. While NSC is a five-year instrument, RBISB is a seven-year investment. Bank fixed deposits offer interim liquidity. In case of need, investors can liquidate their fixed deposits, subject to penal interest. Bank depositors also have the option of taking loans against fixed deposits to tide over any short-term liquidity crunch.

In the case of NSC, there is no interim liquidity; but some banks do offer loans against the instrument. The RBISBs are not traded in the secondary market and no bank offers loans against them. However, in the case of senior citizens, there are rules that permit premature withdrawal. The Lock-in period for investors in the 60-70 years age bracket is six years from the date of issue, while for those in the 70-80 years category, withdrawal is allowed five years from the date of issue. Investors aged 80 and above can withdraw after four years from the date of issue. In the case of joint holders, these rules will apply if even one of the holders fulfils the conditions mentioned above.

Though NSC and RBISB score high on safety and returns, investors should not ignore the liquidity angle. “Many investors compare investments on the basis of the return, but ignore the liquidity aspect of it. While investing in NSC and RBISB, they should pay heed to the limited liquidity offered by these investments,” says Vishal Dhawan, founder and chief financial planner, Plan Ahead Wealth Advisors.

Investors should also keep in mind that the NSC are available only through post offices. RBISBs are available through nationalised and select private sector banks.

TaxationThe interest paid on the NSC and RBISB is added to the income of the investor and taxed at marginal rate of tax. Investments in the NSC of up to Rs 1.5 lakh are allowed for tax deduction under section 80C of the Income Tax Act. There is no tax deduction available on investments in the RBISB.

Should you invest?It is prudent to link your investments to your financial goals. If you are saving for a goal five years away, then the NSC may make sense if you are a low-risk investor. For an individual with a low risk appetite and income needs, the RBISB may make sense.

But you must strike a balance among risk, return and liquidity. Tax is one more consideration you must not lose track of. “Investors in the lower income tax brackets can consider investing in NSC and RBISB,” says Vishal. For those in in the higher tax brackets, purchasing tax-free bonds make sense. They can also consider investing in bond funds that invest in high-quality papers.

Whatever tax bracket you may be in, a well-diversified approach to multiple asset classes and investment avenues is necessary.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.