")

Krishna Karwa, Nitin Agrawal & Ruchi Agrawal

Moneycontrol Research

A recent Goldman Sachs report has hinted at the possibility of Reliance Retail going public in the foreseeable future. This calls for a closer look at the Mukesh Ambani-led retail giant, especially at a time when D-Street is getting increasingly bullish about this fast growing sector.

About Reliance Retail

Reliance Retail (RR), a part of Reliance Industries, is India’s biggest retailer by revenue and network. The company has 7,573 retail stores (with a retail area of 17.7 million square feet) and 495 company owned company operated (COCO) petro retail outlets across more than 4,400 cities throughout the country.

What could work in Reliance Retail’s favour?

Supply chain tie-ups: Given the breadth of its presence, RR has been successful in sourcing products cheaply and has ensured last-mile connectivity through distribution partners across geographies.

Brands: Keeping product differentiation and appeal in mind, RR has a basket of private label brands in its kitty:

Since its own brands have better margins, the company can afford to increase marketing and promotional spends for the same to drive revenue growth.

Diverse product range: RR’s key product verticals include fuel retailing (Reliance petrol pumps), food items, apparel, lifestyle accessories, electronic goods, jewellery and footwear. Varied price points within each category, coupled with periodic schemes/discounts, have helped mitigate segmental risks and boosted revenue growth over the years.

Aggressive expansion: To accelerate sales growth, RR is focusing on a healthy blend of outlet additions and same-store sales growth. Grocery and fashion outlets attract high footfalls, but consumer electronics have a higher ticket size per transaction. To capitalise on the boom in e-commerce, the company is investing more in its online portals too.

Peer comparison – an overview

The path ahead

RR has all that it takes to hold its own when pitted against the best in the Indian retail industry. Topline traction visibility across all segments, increased emphasis on omnichannels and own brands and the ability to leverage RIL’s strengths (in terms of logistics, sourcing efficiencies, Jio’s vast customer base etc) should boost its growth prospects noticeably.

In the grocery segment, RR is optimistic about the fruits category. In case of apparel, a robust domestic demand scenario is further bolstered by the company’s association with 36 foreign brands. The company’s downstream fuel outlets are strategically located on highways and derive good volumes. Lastly, tailwinds in the white goods industry will benefit the consumer durables segment.

However, RR, like any other retail company, isn’t immune to some bottlenecks. Retail businesses, more often than not, are not high margin. Compounding the problem for RR is the fact that juicy margins in some segments could be offset by lower margins in others. Stiff competition will persist, thus necessitating capex and operating expenditure at regular intervals.

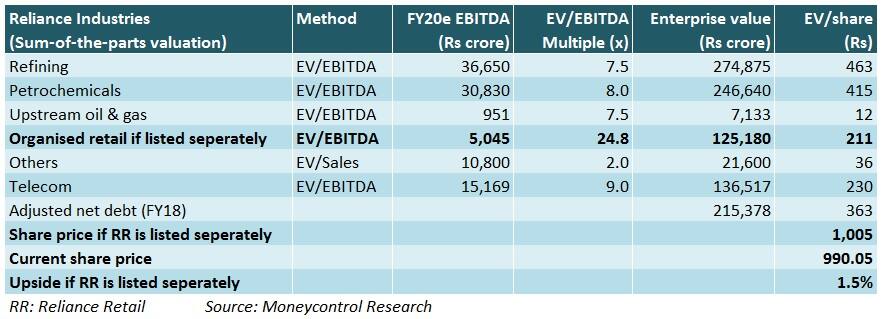

Does a shareholder receive any value on RR's listing?We valued the various businesses of RIL based on FY20 projected earnings before interest, tax, depreciation and amortisation (EBITDA) by sum-of-the-parts (SoTP) methodology to calculate the potential upside if the retail business was to be carved out.

Should RR be listed as a separate entity by going through a public issue, we expect it to trade at an FY20e enterprise value/EBITDA of 24.8 times. We arrived at this multiple after considering a discount of 30 percent to the average industry EV/EBITDA multiple of 35.4 times. The discount is because RR’s operating margin is only 3.7 percent as against the industry average of 7.9 percent.

The markets are factoring in value from RIL's retail division in RR’s price. RR’s EBITDA constitutes only 5 percent of RIL's consolidated EBITDA. Hence, RR’s margins won’t move the needle for RIL's overall margins significantly.

If RR was to be hived off from RIL and listed, the upside would be limited.

Disclaimer: Reliance Industries Ltd. is the sole beneficiary of Independent Media Trust which controls Network18 Media & Investments Ltd.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.