Highlights

- Deal for 100 percent stake sale in loss-making Czech arm goes through

- NCLT nod for merger of consumer-facing business a major catalyst

- The company has gained market share in the domestic space

- Well placed to take on competition with higher investments

- Strong rally since early 2019 factors in major positives

Tata Global Beverages (TGBL) (CMP: Rs 352, market capitalisation: Rs 22,272 crore) has many high points to talk about: It continues to execute restructuring initiatives, along with a commendable operating performance in the recent past. Over the weekend, a couple of news reports underscored that.

Its UK-based subsidiary has sealed an agreement with Dr Muller Pharma s.r.o. for a 100 percent stake sale in its Czech arm - Tata Global Beverages Czech Republic. Additionally, the National Company Law Tribunal (NCLT) has approved the scheme of arrangement between Tata Global Beverages and Tata Chemicals, which paves the way for demerger of the consumer product business from Tata Chemicals and integration of the same with TGBL.

Stake sale in Czech subsidiary

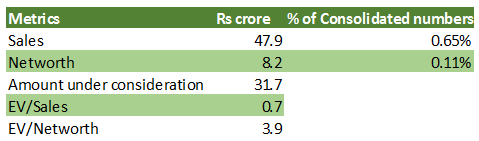

Table: Tata Global Beverages Czech Republic (FY19)

Source: Tata Global Beverages

The stake sale in the Czech subsidiary for Rs 31.7 crore (euro 4 million) includes compensation for trademark rights. At EV (enterprise value)/Sales level, this comes to a mere 0.7x, which is at a discount to TGBL's trading multiple of 3.1x.

However, we don’t see this metric as a right one for comparison as the subsidiary has been reporting loss. In FY19, the bottom line loss for the subsidiary was to the tune Rs 4.7 crore on a sales of Rs 47.9 crore. In fact, EV/Net worth multiple of 3.9 appears to be reasonable compared with some of the notable names in the domestic beverage industry.

Table: EV/Net worth

Source: Moneycontrol Research

The NCLT green light

With the NCLT nod, we believe that the merger with the consumer-facing business of Tata Chemicals and its positioning in the FMCG space remain key catalyst for the long term.

Addition of newer complementary categories such as macro snacks, beverages such as juices or other staple products cannot be ruled out, where Britannia, Dabur and ITC are major competitors, respectively. However, we see a substantial gestation period before it plays out to have a significant impact on the bottom line.

Outlook

All said, the recent news flow only lends credence to the company’s continuous focus on restructuring and plan to exit un-remunerative businesses. Continuous monitoring of international portfolio makes sense as some of the markets are facing challenges, including category shrinkage due to heightened competition. And in this context, the stake sale of Czech business is a welcome move.

The recent operational performance stood out, too. Tata Global’s 8 percent volume growth in the India business in Q2 FY20 was commendable, given the prevailing consumption headwinds. The management noted that beverages has done better than other FMCG categories even though it also faced a slowdown in rural areas.

Further, the company has been able to gain market share in the domestic market. The acquisition of Dhunseri Tea bolsters its leading position in the domestic tea market. The JVs, Tata Starbucks and NourishCo, are also progressing well, with the latter achieving break-even at the net profit level.

Tata Global seems well placed to take on competition with increasing investments in brands, advertisement and promotional initiatives. However, this is likely to keep operating margin in check.

Meanwhile, the stock has moved up 95 percent from its lows in February 2019. It is trading at 47x FY21 estimated proforma numbers of the combined entity. This kind of multiple is being currently enjoyed by some of the well-diversified FMCG players.

We think that a large part of the near to medium term positives is already factored in and hence, we remain on the sidelines. Investors who had bought the stock to participate in a turnaround story and benefited from corporate restructuring can consider the recent rally as an opportunity to book profit.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!