Downstream gas companies reported a mixed performance in Q2 FY19. Indraprastha Gas (IGL) and Mahanagar Gas (MGL) posted a healthy uptick in revenue and profit driven majorly by strong volume growth in the city gas distribution (CGD) segment. However, Gujarat Gas saw some hit on profitability, with limited price uptick during the quarter gone by.

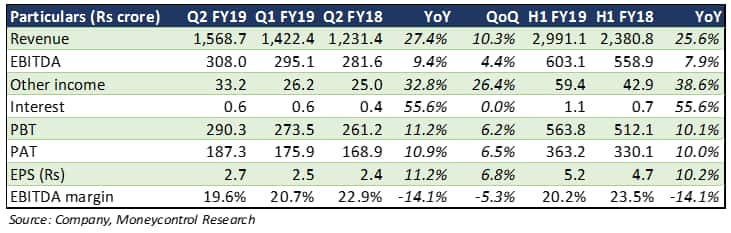

Indraprastha Gas

The company reported a 27.4 percent year-on-year (YoY) uptick in topline owing to a 12.9 percent volume uptick. Compressed natural gas (CNG) volumes grew 12.9 percent and piped natural gas (PNG) segment saw a 13.3 percent volume improvement. While higher taxes impacted net profitability, the same was offset by higher other income and lower other expenses. With plans in Delhi to provide concession on CNG conversion costs, the longer term outlook on volumes remains positive.

The long standing dispute with Haryana City Gas Distribution (HCGDL) also now stands resolved with the Supreme Court's approval for IGL to acquire HCGDL. This would enable IGL to expand rapidly in the region.

Mahanagar Gas

The 9.5 percent growth in volumes led to a 30 percent revenue growth during the quarter gone by. Both CNG and PNG volumes grew 9.2 percent and 10.2 percent, respectively. Higher gas prices for industrial and commercial segment, a depreciating rupee and higher tariff for GAIL's pipeline usage resulted in higher raw material and operating cost and moderated benefits of higher realisations. However, the management has taken adequate price hikes, which will help it protect margin going forward.

Around 85 percent of MGL's business is constituted by CNG and domestic PNG, which have a priority allocation of domestic gas from the government. This works in favour of the company and helps in protecting margin. Going forward, the company plans to aggressively expand CNG and PNG segments.

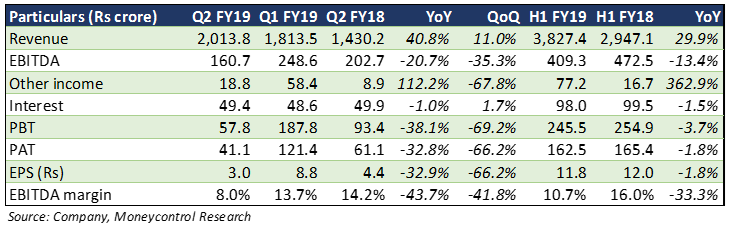

Gujarat Gas

Despite a healthy uptick in volume (16.5 percent) and revenue (41 percent), the quarter’s performance remained muted. A sharp surge in natural gas prices and weaker rupee inflated input costs for the company. With more than 70 percent of the business catering to the industrial segment, the company could not access benefits of priority domestic gas allocation. This led to a noticeable impact on profitability with earnings before interest, tax, depreciation and amortisation (EBITDA) and net profit down 20.7 percent and 33 percent, respectively.

Priority domestic gas allocation: The government has ordered priority allocation of domestic gas for CNG and PNG segments. This has substantial play is aiding margin protection for IGL and MGL, who have majority exposure to these two segments. Owing to majority industrial sector sales, Gujarat Gas enjoys limited benefits of this ruling.

Cheaper alternate fuel: Natural gas is a cheaper alternate fuel and is rapidly gaining popularity. This was one reason that led to a substantial volume uptick for these companies during the quarter gone by. The same is expected to continue in coming months both in the industrial and the domestic segments.

Environmental concerns and policy support: With environmental concerns growing by the day, there has been immense policy support to promote use of a relatively cleaner fuel like natural gas. The government has also ordered priority allocation of domestic natural gas for CNG and PNG segments to promote the use of natural gas, maintain low prices for consumers and help companies maintain margins.

Moreover, the government is now looking to aggressively expand the city gas distribution (CGD) network and increasing number of cities are being added in each round of bidding. With the 10th round of bidding on the cards, volumes are set to improve in the longer run.

Debt-free balance sheets: Both IGL and MGL have debt-free balance sheets, which leaves immense scope for future capital expenditure and expansion. Both companies are cash rich. With debt on its balance sheet, Gujarat Gas has a debt equity profile of 1.2 times. We believe these are important factors to be watched, especially amid volatile market conditions.

Outlook

Moneycontrol Research

Given the macro opportunities, we remain positive on the sector's growth story. Gas company stocks have seen a substantial correction in the last 12 months, although they have gone up in the last one month. At the current multiples and product mix, we prefer MGL and IGL over Gujarat Gas. Amid the current market volatility and with noticeable swings in stock prices, we recommend investors accumulate these stocks on dips.

Follow @RuchiagrawalFor more research articles, visit our Moneycontrol Research pageDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.