With over 2,000 film releases in 2017, movies continue to be largest source of entertainment in India. Thanks to a huge population, along with high propensity of Indians to consume films, cinema theatres see the highest footfalls globally. No wonder, screen additions continue with growth in multiplexes in a market traditionally dominated by single screens.

PVR is the largest multiplex operator in the industry with around 700 screens across India. We visit the major events that have unfolded in the last couple of months relating to the company and analyze its impact on financials and future profitability.

Potential threat to F&B revenue seems to have recededThe Maharashtra government completely retraced its earlier stance in response to a public interest litigation (PIL). It is not in favour of allowing outside food in multiplexes citing security reasons. The PIL challenged the current practice wherein multiplexes prohibit customers bringing in and consuming food and beverages (F&B) from outside. Read | Outside food in theatres: Wait till the picture becomes clear

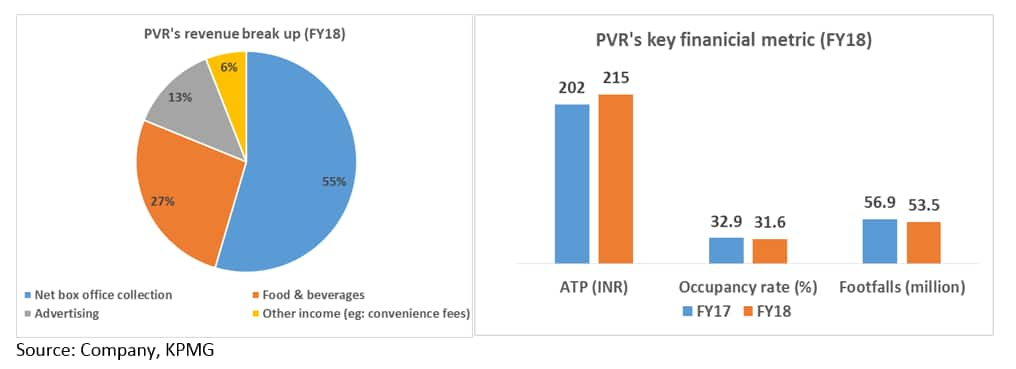

Though the matter is still sub judice, the government’s stand comes as a big relief to multiplex operators. The Supreme Court also imposed a stay on a Jammu & Kashmir High Court order allowing cinemagoers to carry their own food and water into theatres. This is very positive as F&B contributes around 27 percent to PVR’s revenue and is the second-fastest growing revenue stream after advertising, at 10 per cent year-on-year.

Given the favourable stance of the Maharashtra government and other judicial bodies, the potential threat to F&B revenue has subsided significantly, helping PVR’s share price recover over 25 percent from its 52-week low in July.

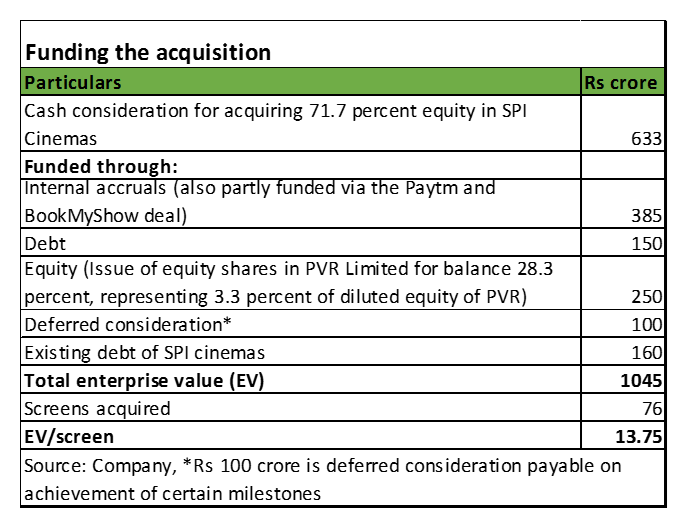

Acquisition of SPI CinemasPVR's recent decision to acquire SPI Cinemas (SPI) significantly strengthens its market position in south India with the addition of 89 screens (76 operational screens plus 13 upcoming). Consequently, contribution of south India to PVR's screen portfolio will increase to 35 percent from 26 percent.

The acquisition makes a lot sense as per capita movie consumption is the highest in south India. The three regional languages - Tamil, Telugu and Kannada - account for 37 percent of total box office collection in India. Though there is cap on ticket prices in Tamil Nadu, SPI’s occupancy at 58 percent as compared to 31 percent of PVR is a compensating factor.

The acquisition will be funded through a mix of internal accruals, debt and equity. The deal would be carried out in two phases for an enterprise value of around Rs 1,000 crore.

SPI’s acquisition is expected to slightly weaken PVR's financial risk profile due to increase in debt to around Rs 1,250 crore from Rs 832 crore as on March 31. PVR’s debt-to-EBITDA (earnings before interest, tax, depreciation and amortisation) ratio will, therefore, increase from 2 times as on March 31, but will remain below 3 times at peak debt.

The acquisition is earnings accretive. As per the management, the circuit is expected to deliver sustainable exhibition EBITDA margin of 21-23 percent after integration and synergies. Opening of 17 and 23 screens in FY18 and FY19, respectively, will drive revenue growth as these properties reach their optimal level of operation. Also, the full year impact of the increase in ticket price cap in Tamil Nadu will drive growth in average ticket price for SPI screens.

Aggressive expansion plans for the futureAs per media reports, PVR is now looking to buy north Indian chain Waves Cinema, but the management denied any such move. But such a scenario can’t be ruled out considering that in the past it has heavily relied on the inorganic route to consolidate its market position. In 2012, PVR acquired Cinemax, strengthening its presence in western India. In May 2016, it completed the acquisition of DT Cinemas in the National Capital Region.

The management is now considering an overseas expansion. After having formed a subsidiary in Sri Lanka in FY18, PVR has now signed an memorandum of understanding (MoU) with Dubai-based conglomerate Al-Futtaim group to explore opportunities to jointly develop a cinema business in the Middle East North Africa region, especially in United Arab Emirates and Saudi Arabia (recently decided to open up to the cinema industry). The potential in terms of pricing (ATP) as well as on the F&B front is much better than global averages in both these markets. Details of the plan like capital outlay are not yet available.

On the domestic front, PVR plans to add 60-70 screens per year and undertake significant capital expenditure for the same.

What do we make out of these newsflows? Expansion is extremely important for a multiplex business as healthy profitability and return ratios come with scale. The increased scale of operations enables higher bargaining power with advertisers and F&B suppliers, which supports operating efficiencies. In this context, PVR seems to be on a right track with its expansion strategy. However, adequate internal accruals are a must to fund its expansion plan, the absence of which would make it dependent on additional borrowings, thereby increasing debt levels and adversely impacting its financials.

We decipher the three main revenue drivers to understand adequacy of internal accruals.

Box office performance Though a largest revenue stream, box office collections are the most unpredictable and volatile. Although ATP has increased, footfalls and occupancy rates have reduced for PVR, which is a big concern, especially in light of the growing popularity of digital platforms. The limited headroom for ATP growth makes other revenue streams extremely important.

Advertising revenue PVR is best positioned with its pan India presence to entice advertisers. Hence, in-cinema advertising revenue can continue to grow for PVR. However, the higher footfalls is a pre-requisite to ensure sustainable higher revenue from this segment.

F&B revenue Even if the court ruling favours multiplex operators and doesn’t permit outside food, we see downward pressure on F&B prices, considering the general backlash. It is worth noting that not only does F&B contributes 27 percent to revenue, gross margin on the same stands around 75 percent. Hence, any reduction in F&B prices means spend per head (SPH), which has been on a rising trajectory, appears to be at risk.

PVR shares a large proportion of ticket revenues with distributors. Its business model is structured to compensate relatively lower ticket prices with higher F&B prices. However, current events may propel some changes to the business model that supports and incentivises screen expansion.

Valuation and outlook The film exhibition segment has seen several decades of disruption through other electronic mediums (VCRs, CDs, DVDs). Theatres not only survived, but flourished during these times. While online streaming providers like Netflix and Amazon Prime can change the way patrons watch movies over a period of time, we don’t see a complete disruption to theatre operators as both mediums can co-exist. For instance, theatres can keep away some competition by seeking exclusivity for a longer period before movies are available on streaming platforms.

Currently, the stock is trading at 49 times FY18 price-to-earnings and 16 times FY18 enterprise value-to-EBITDA. In terms of forward multiple after considering dilution, the stock is trading at 32 times FY19e P/E, which is reasonable. However, a valuation re-rating is unlikely due to uncertainty around F&B revenue and challenges posed by digital platforms. Long term investors wanting to play the multiplex sector should buy the stock on dips.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.