Highlights

- Strong Q3 a result of traction in the domestic market

- Commercialisation of new products infuses life

- Healthy Rabi season and improved acreages other positives

- Isagro buyout complete, margins seen steady- Company on track to raise funds via QIP for expansion

--------------------------------------------------------

Chemical manufacturer PI Industries (PIND) (CMP: Rs 1,535; Mcap: Rs 21,395 crore) went all guns blazing during October-December of 2019-20 with a healthy set of earnings. Traction in the domestic market and the custom synthesis manufacturing (CSM) segment steered the ship. Commercialisation of new products also gathered steam.

About the company

PI Industries manufactures agrochemicals, plant nutrients, plant protection chemicals, specialty fertilizers and hybrid seeds. It also provides services in contract research and process development, among others.

Financial performance

Key highlights

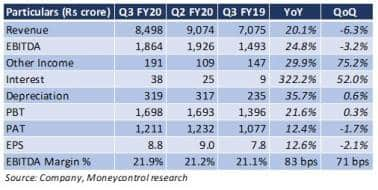

PIND registered a growth of 20 percent year-on-year (YoY) in consolidated revenue as both CSM and the domestic market shaped up.

The local operations grew 20 percent on the back of good Rabi sowing amid healthy reservoir levels, which boosted volumes. The CSM segment expanded 24 percent as it gained from commercialization and ramp-up in demand for new molecules launched by the company.

Product mix improved with a slight moderation in raw material cost, which means a sequential improvement in gross margin.

However, earnings before interest, taxes, depreciation, and amortization (EBITDA) margin remained steady on higher other expenses and employee cost.

The quarter also saw a jump in tax expenses, along with higher depreciation, which ate up a part of net profit growth.

Other comments

The acquisition of Isagro is now complete and the financials of the company are expected to get consolidated from Q4 onwards. The domestic business of Isagro will be transferred to a subsidiary, Jivagro, while the remaining business will be merged with PI. The low-margin profile of Isagro’s business might chip away at margin expansion of PI Industries. That means margins are expected to stay flat.

Meanwhile, the board has approved a fund-raising plan via QIP (qualified institutional placement) for Rs 2,000 crore in the coming two months. The funds, once raised, would go towards scaling up the existing operations, organic growth, R&D (research and development) and diversification into new verticals like pharma CSM, specialty chemicals, and nutraceuticals.

The current coronavirus spread is a point of concern for many agrochemical companies. According to the management, the company is well covered for Q4. However, if the spread is not contained post Q4, there might be some impact. Since the revenue dependency of the company on China is in single digits, the effect might not be a lot.

There has been a temporary shutdown of the Jambusar plant, which may have an impact to the tune of Rs 40-50 crore in Q4. However, the management has ruled out any impact as far as orders are concerned.

Outlook

A key takeaway is volume surged noticeably. The CSM business has seen a strong build-up, with inflows coming in from the order book. We expect this to continue.

With enquiries on the rise leading to more firm orders, we expect the growth in exports to sustain. A ramp-up in sales of recent product launches, along with new molecules lined up, suggests that volumes will improve.

The company’s domestic business has also shown signs of revival with a healthy Rabi season. And the Isagro takeover is expected to bolster the domestic play.

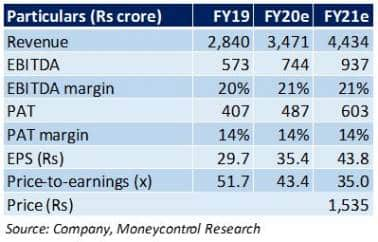

The stock has had a steady run over the past months. At current prices, it is trading close to its 52-week high, valuing the company at 35x FY21e earnings, which seems a bit on the higher end. The company’s growth story remains intact. We would recommend to keep the stock on your radar and enter when there is a correction.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!