Jitendra Kumar Gupta

Moneycontrol Research

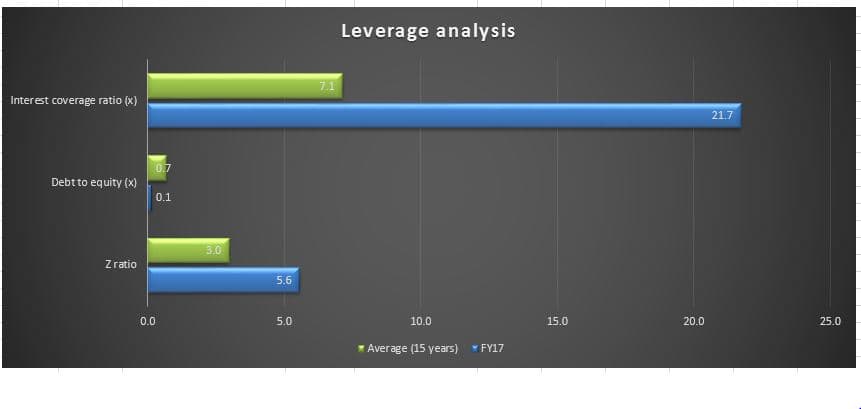

While investing in commodity companies, prudence lies in looking at the balance sheet. Maithan Alloys, which is into manganese and ferro alloys, is one such company that has succeeded in managing its balance sheet prudently during different industry cycles. Despite the business being working-capital intensive, its debt-to-equity has remained at an average of 0.7 times and interest coverage at 7 times over the last 15 years.

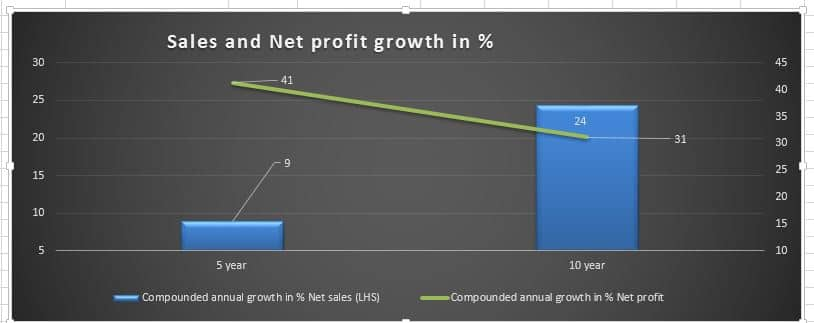

Importantly, the cash generated during good times has been used for reduction of debt and the company today is debt free (adjusted for cash). What is worth taking note of is the fact that despite the conservative approach, it has managed to grow well. Over the last ten years, its net profits have grown at 31 percent annually on the back of 24 percent annual growth sales.

Maithan Alloys has close to two decades of experience in manganese, which finds its application in steel and stainless steel. For every tonne of steel produced, close to 1-1.5 percent of manganese alloy is required.

Effectively, the growth of ferro and manganese is closely linked with growth in steel demand. In India, Maithan supplies manganese to clients like SAIL, Jindal Stainless, JSPL, JSW Steel. Ferro alloys enhance steel strength, durability, anti-corrosion and anti-stain properties and acts as de-oxidant for steel manufacturing.

The growth in steel is expected to improve with the National Steel Policy envisaging to take domestic steel production of about 300 million tonnes by the end of the year 2030 as against current production of about 120 million tonne.

Better realisations to drive earnings growth

The upcycle in the steel industry has already began. In the calendar year 2017, India has already produced about 3.6 million tonnes of stainless steel, which is about 8.3 percent higher in the corresponding period last year.

Maithan Alloys, which is the largest player, has seen a spurt in earnings over the last two years backed by strong volume growth and realisations.

The global upcycle in the steel industry has helped companies like Maithan Alloys, which is one of the lowest cost producers in the world. Moreover, within steel the consumption of stainless steel is increasing at a higher pace leading to better pricing.

Demand is expected to pick up further with the global steel production increasing. Moreover, the domestic steel utilisation of the stressed steel plants post the restructuring or sale of these assets will pick up and generate more domestic demand for manganese.

There is a high possibility of manganese prices hovering at current levels. As against Rs 54000 a tonne realisations in FY16, the company posted realisations of about Rs 63000 per tonne in FY17. If the prices remain at current levels (high probability given the demand) there is more room for the earnings growth. In January this year the manganese ferro prices had crossed a high of Rs 100000 per tonne and corrected to around Rs 60000 a tonne in May 2017. However, thereafter, they have stabilised at the current levels of about Rs 70000-72000 a tonne.

Eyeing inorganic growth

The company is currently producing about 2.13 lakh tonnes annually and running at full capacity of about 95 percent leaving very little room for the volume growth. Growth in the coming year will be largely driven by higher realisations and marginal growth in volumes. While the company is evaluating land for the greenfield expansion, which might take time, in the interim it is looking for the acquisition as the company believes that because of the stress in the sector and marginal players unable to carry on business and are up for sale. It is thus in talks with banks exploring suitable acquisition opportunities as the company is sitting on close to Rs 190 crore of cash (Rs 585 crore net worth) in the books.

Valuations

There may not be a strong growth in the medium term till the time the company is able to scale through organic and inorganic routes. What is important is that promoters have extensive experience having demonstrated capabilities to sail through several commodity down cycles with the focus on keeping costs low.

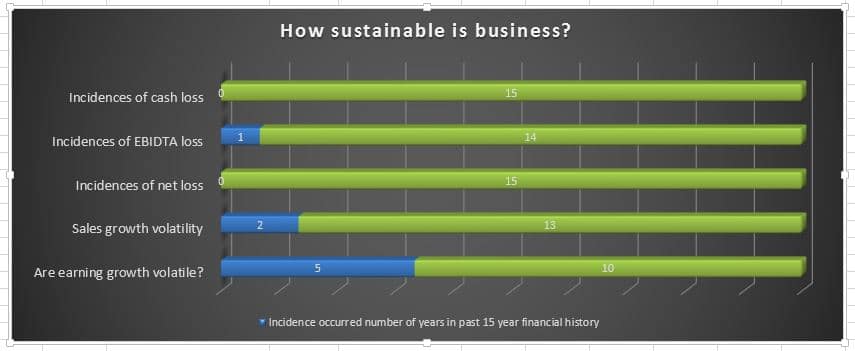

Even at the current scale and realisations, it will make an annual operating cash flow of close to Rs 180-200 crore (Rs 126 crore in FY17), which is about 9-10 percent earning yield on its current market capitalisation of Rs 1923 crore (share price of Rs 651). This is quite good for a company which is a low cost producer having a dominant position. The company has zero debt in the books and never in the last 15 years had a cash loss. It is earning a return on equity of close to 32 percent, in fact, higher should one adjust for the ideal cash on the books.Follow @jitendra1929

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!