Nitin Agrawal Moneycontrol Research

JBM Auto (JBM) is a leading auto-component manufacturer catering to passenger vehicle (PV), commercial vehicle (CV) and tractor segments. With marquee clients in its kitty, huge industry opportunities, focus on high margin products, plans for launching electric buses, strong performances from subsidiaries and joint ventures (JVs), and robust financials, the company beckons investor attention.

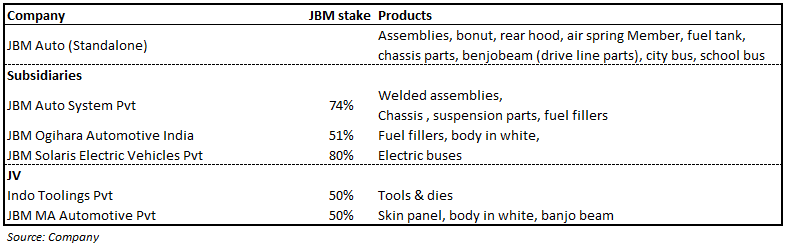

The business The company is one of the leading auto component manufacturers. Within this segment, it manufactures safety critical items such as chassis and suspension systems like axles, twist beams, lower control arms, sub-frames, exhaust systems, air tanks, fuel tanks, complete cowl assemblies, pedal boxes etc.

JBM has a tool room division that provides tools and dies for turnkey projects. The bus division of the company deals in a diverse portfolio of buses (CNG, diesel and electric). It has, strategically, located its plants in close proximity of leading automobile hubs of India at Delhi-NCR, Sanand, Pune, Indore, Nashik, Bengaluru and Chennai.

The table below gives an overview of the company’s main segments, product portfolio and products it manufacturers:

Riding on PV growth With effects from the regulatory challenges – demonetisation, transition to Bharat Stage IV and Goods & Services Tax waning, things have returned to normalcy for the automobile sector. This is evident from the volume growth being registered by original equipment manufacturers (OEM).

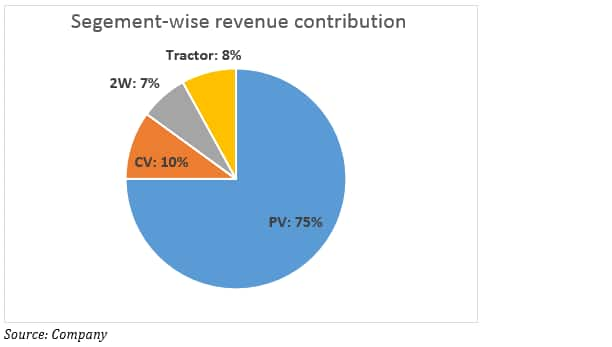

The PV segment, in particular, is set to cruise smoothly in India on the back of lower car penetration, increasing affordability and rising disposable income. At present, PVs currently constitute 13 percent of total automobile sales volumes compared to 81 percent for the two-wheeler (2W) segment. There is a massive long term growth potential for the PV segment. JBM is in the sweet spot to capture this growth as it generates around 75 percent of its revenue from this segment.

CV and tractor segments are also doing well on the back of government’s focus on infrastructure, increase in mining activity, normal monsoon lifting rural sentiment and strict implementation on the overloading ban.

Strong clientele The management boasts of a strong client base which includes auto majors such as Honda Motors, Mahindra & Mahindra (M&M), Eicher Motors and Tata Motors. The company generates around 35 percent of standalone sales from Honda Motors and 10 percent each from M&M, Eicher and Tata Motors. JBM is expected to benefit from Tata Motors and Eicher gaining strength in the PV and CV segments, respectively.

Electric vehicle ready The company has forayed into the manufacture of buses and deals in a diverse bus portfolio (CNG, diesel and electric). It has started supplying CNG buses to Noida Metro and is focusing on other regions as well. In lieu of the government’s focus on electric vehicle, it has signed a JV agreement with Solaris Bus & Coach, Europe in July 2016 for developing EVs.

Focusing on the high margin tooling business Though the tooling business contributes around 5 percent of total revenues, the management is aggressively focusing on this high margin business (around 3 times the margin of auto component business). Increase in contribution from the tooling business would lead to margin expansion for the company.

Subsidiaries and JV are on a rise Most subsidiaries and JVs of JBM are performing well. JBM Auto System Pvt (JBMAS) is a key supplier to Ford India and has benefitted from growth accruing from the latter. Moreover, the success of Renault-Nissan is also benefitting JBMAS.

JBM Ogihara Automotive India (JBMOA) is performing well on the back of Toyota, which is its biggest client. JBM Solaris Electric Vehicles Pvt (JBMSEV) is seen growing on the back of an expected rise in the adaption of EVs.

On the JVs front, JBM MA Automotive Pvt (JBM MA) is catering to Jeep of Fiat, which is receiving overwhelming response from customers.

Financial performance From a financials perspective, revenue grew 12 percent compounded annually over FY11-17. Earnings before interest, tax, depreciation and amortisation (EBITDA), however, grew faster at 15 percent over the same period. This is due to operating leverage and fall in raw material (RM) prices. EBITDA margin has averaged around 11.6 percent over the same period. Margin was impacted in FY17 due to losses in the bus business. The same recovered on the back of strong growth coming in from the PV segment.

Profit after tax (PAT) witnessed a compounded growth of 17 percent over FY11-17 on the back of falling interest expense and rising other income. The company has consistently reduced debt and debt-to-equity ratio down to 1.14 times in FY18 from 2.67 times in FY11.

Superior returns

In terms of return ratios, it has delivered average return on equity (RoE) and return on invested capital (RoIC) of 20.5 percent and 12.6 percent, respectively, over FY11-17. Returns in FY16 were impacted due to its venture into the bus business.

The company is trading at 13.7 and 12.2 times FY19 and FY20 projected earnings, respectively.

Peer analysis Peer analysis suggests that JBM is currently trading at a discount compared to the average multiple of its peers.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.