Highlights - RBI report encourages conversion of a large NBFC into a bank - With reducing regulatory arbitrage between a bank and an NBFC, merger of HDFC with HDFC Bank makes a lot of sense - HDFC can benefit from HDFC Bank’s retail and low-cost deposit franchise - Merger can enhance HDFC Bank’s cross-sell opportunities and increase capital efficiency - Pros and cons of merged entity– profitability will come down but may create room for more foreign holding - Merger will create a lot of synergies and a financial behemoth --------------------------------------------------------

Note from the Editor: We had published this piece in Moneycontrol Pro over a year ago. Now, we are opening the paywall on this to make it accessible to all readers while we continue to cover all aspects of the merger.With HDFC set to acquire 41 percent stake in HDFC Bank, the merger between the two is finally a reality, which is likely to create the third-largest entity in India in terms of market capitalisation.

In an exchange filing, HDFC announced that the company will merge itself with HDFC Bank following a union of subsidiaries HDFC Holdings and HDFC Investments. A similar announcement was made by HDFC Bank in a separate exchange filing.

This merger between HDFC Bank (CMP: Rs 1,639) and housing finance giant HDFC (CMP: Rs 2,738) had been talked about for a very long period. Ever since the merger of ICICI Bank and its parent ICICI in 2001, there is speculation that the fate of HDFC and HDFC Bank may be similar.

While the talks of a possible merger between the two keep surfacing time and again, a report by an Internal Working Group of the Reserve Bank of India re-ignited such speculations. The IWG recommending that well-run large NBFCs may be considered for conversion into banks heightened the case for the HDFC Bank–HDFC merger.

Once the merger process gets complete, it promises to create a financial behemoth with a loan book size of Rs 15 lakh crore and an asset base of Rs 21.5 lakh crore.

The managements of both entities have always maintained that a merger is possible in the long run if regulatory hurdles are sorted out and if the move is beneficial to all stakeholders.

As per current structure, HDFC owns 21.5% equity in HDFC Bank. Since it was set up in 1994, HDFC Bank under the leadership of Aditya Puri has overshadowed its parent HDFC in terms of growth and performance and has been the Street’s favourite.

Nonetheless, the current structure of two separate entities has worked remarkably well for several years. This gets validated by the fact that the combined market cap of HDFC twins is more than that of Reliance Industries - the country’s most valuable company. And if we take the combined market cap of all the 4 listed companies in the HDFC group, it is just shy of the market cap of the entire Tata group which has over 20 listed companies.

So the moot question is: Why consider a merger?

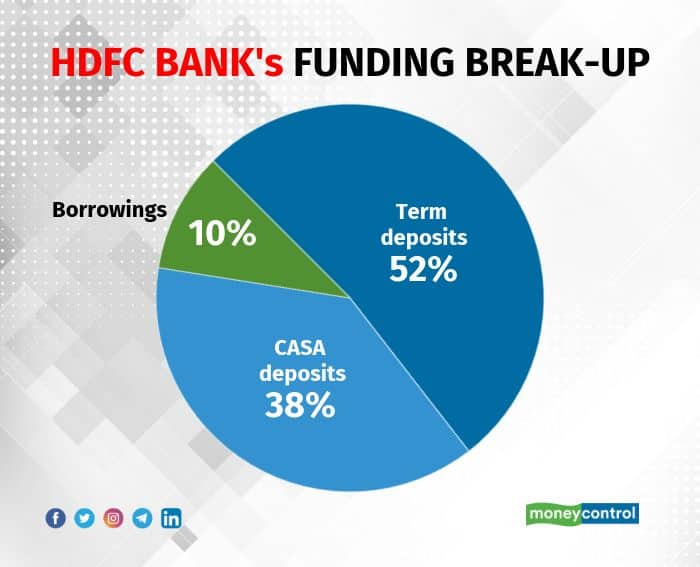

Create a funding advantage HDFC has done exceedingly well in managing its spreads across interest rate cycles. However, its cost of borrowings, despite being the best among NBFCs, stood at around 7.20% in the second quarter of FY21. In contrast, HDFC Bank’s cost of funding stood below 5%.

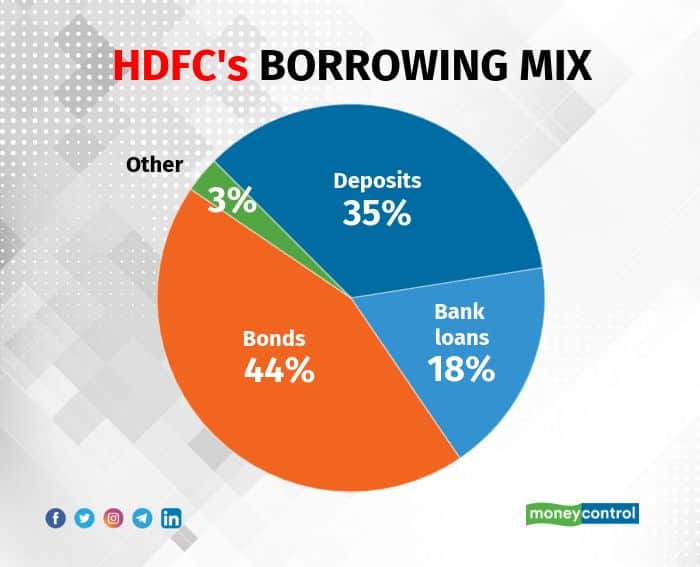

Though HDFC’s funding cost has declined in the current fiscal, the reduction has not been proportionate to the fall in interest rates. That’s because HDFC’s deposit book stands at Rs 148,330 crore, constituting 35 percent of total borrowings as at end-September. Though deposits are stickier, interest paid on deposits is generally higher compared to funds accessed from bond markets.

Source: Company, data as of end September'20

Source: Company, data as of end September'20 Source: Company, data as of end September'20

Source: Company, data as of end September'20Overall, HDFC being largely a wholesale financier is relatively more exposed to volatility in interest rates and liquidity than HDFC Bank. A merged entity will have a more sustainable and favorable funding profile.

Source: Company, data as of end September'20

Source: Company, data as of end September'20While funding benefits will be real and known for years, the regulatory cost of merging into the bank has been the biggest impediment. However, the RBI is increasingly moving towards reducing the regulatory arbitrage between a bank and an NBFC which makes the environment more conducive for merger.

Reducing regulatory arbitrage supports merger The norms on regulatory asset-allocation for banks are quite stringent as they need to allocate 40 per cent of assets towards priority sector loans in addition of setting aide cash reserve ratio (CRR) and statutory liquidity ratio (SLR). This makes banks’ asset mix much more inefficient versus non-bank lenders.

The RBI, in 2014, scrapped reserve requirements for infrastructure lending and funding affordable housing through long- term bonds, eliminating the widely-known and biggest stumbling block for the merger. The other regulations like NPA recognition, provisioning, risk weights are almost identical for banks and housing finance companies (HFCs).

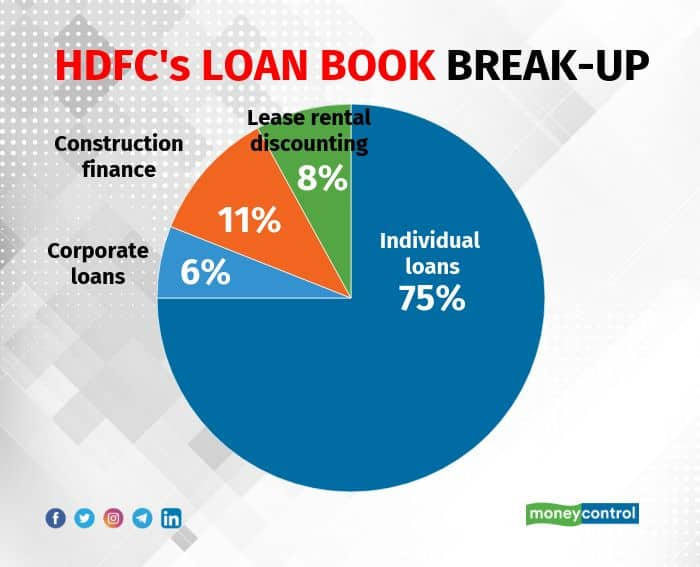

Loans to individuals constitute around 75 per cent of HDFC’s loan book as at end-September and it is increasingly targeting the economically weaker section (EWS) and lower income group (LIG) segments in affordable housing since a couple of years. For instance, in the first half of this fiscal (H1 FY21) around 18 per cent of home loans in value terms have been to customers from the EWS and LIG.

With relaxation from RBI on affordable loans, efficiency of a merger between HDFC’s assets with that of HDFC Bank has improved considerably.

The merger makes sense for HDFC on many counts, but what’s the incentive for HDFC Bank?

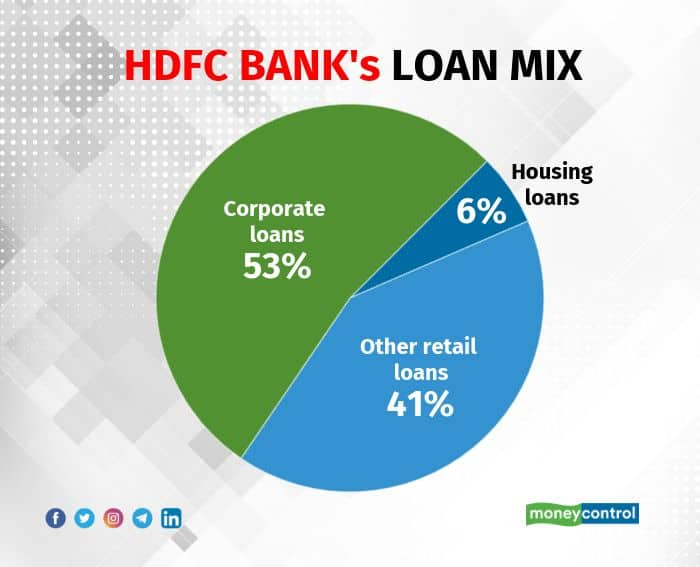

Merger will entail diversified loan mix and higher capital efficiency for the bank Home loans constitute only 6 per cent of HDFC bank’s loan book as at end-September. The proportion is much higher in case of peer banks. As per the current arrangement, HDFC Bank sources home loans from HDFC for a fee.

Source: Company, data as of end September'20

Source: Company, data as of end September'20 Source: Company, data as of end September'20

Source: Company, data as of end September'20With HDFC Bank incrementally focusing on corporate loans and being cautious on unsecured lending (personal loans and credit cards), the loan book is likely to tilt in favour of corporates.

A potential merger will not only lead to a well-diversified loan mix but will also help meet priority sector requirements. The merged entity’s capital efficiency will be higher as housing loans carry less risk weights as compared to other retail loans. Moreover, HDFC Bank’s growing capital requirements can be met by small stake sales in the group’s other key businesses.

Source: Company, data as of end September'20

Source: Company, data as of end September'20Additionally, HDFC has 7.7 million customers and around 2.1 million depositors. A merger will help unify the customer base and also increase cross-sell opportunities for the bank.

Merger can create room for more foreign holding Foreign holding in HDFC Bank is capped at 74 per cent and it has already crossed 71 per cent in November ’20. Due to limited room for foreign portfolio investors (FPIs) to buy HDFC Bank stock domestically, the bank’s ADR trades at significant premium (over 15%) to its domestic share price.

Foreign shareholding of HDFC stands at around 70 percent of its paid-up share capital and accordingly HDFC’s stake of around 21 per cent in the HDFC bank is deemed as indirect foreign shareholding. A merger can open up the window for FPIs as the foreign holding in a merged entity may fall below the current limit of 74 per cent increasing the room for more buying in the merged entity.

A win-win for both Despite the synergies on cost and capital front, the merger won’t be a smooth ride. Since only part of HDFC’s loans is towards affordable housing (assuming 40-50 per cent of individual loans), the merged entity will have to allocate funds for CRR and SLR on remaining portfolio. This will adversely impact margins and profits. The merger could also lead to a potential loss of some bancassurance tie-up.

But with benefits outweighing the cost, the merger can be a win-win situation for both entities. The exact benefit to the shareholders of HDFC twins will depend on the swap ratio.

While HDFC twins have already created a lot of shareholder wealth individually, it wouldn’t be over the top to say that the merger of HDFC Bank and HDFC will increase shareholder value manifold.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.