Highlights

Every major economic shift has been powered by a defining layer of infrastructure — roads for industrialisation, telecom towers for connectivity, and now data centres for the digital and AI (artificial intelligence) economy. While data centres have long hosted servers and networks, the explosive compute needs of AI have pushed them to the forefront.

Rising cloud adoption, data consumption, and AI workloads have made data centres the backbone that converts land, power, and capital into compute and intelligence, underpinning everything from banking transactions and OTT streaming to enterprise software and AI model training and inference.

Also Read: Which stocks are good to ride India’s data centre boom?

Despite the perception that India lags in AI, a powerful surrogate ecosystem is taking shape. Policy-led data localisation, strong demand visibility, and years of under-investment have created structural capacity constraints, positioning data centres as one of India’s most compelling long-cycle infrastructure opportunities.

Over time, data centres have evolved from small, enterprise-owned server rooms into large, industrial-grade facilities. Today’s ecosystem includes enterprise data centres (dedicated to a single organisation), colocation facilities (shared infrastructure leased to multiple users), cloud data centres operated by hyper-scalers such as AWS and Azure, and managed services run by third-party providers. In addition, new formats like edge data centres, located closer to end users for low latency, and hyper-scale campuses, built specifically for cloud and AI workloads, are gaining prominence.

Structurally, India has converged on the colocation model, where enterprises and hyper-scalers lease space, power, and cooling instead of owning facilities. This model offers speed, capital efficiency, scalability, and regulatory compliance, making it the preferred route for large-scale data centre expansion.

Assessing the data centre opportunity

Demand-supply gap is favourable

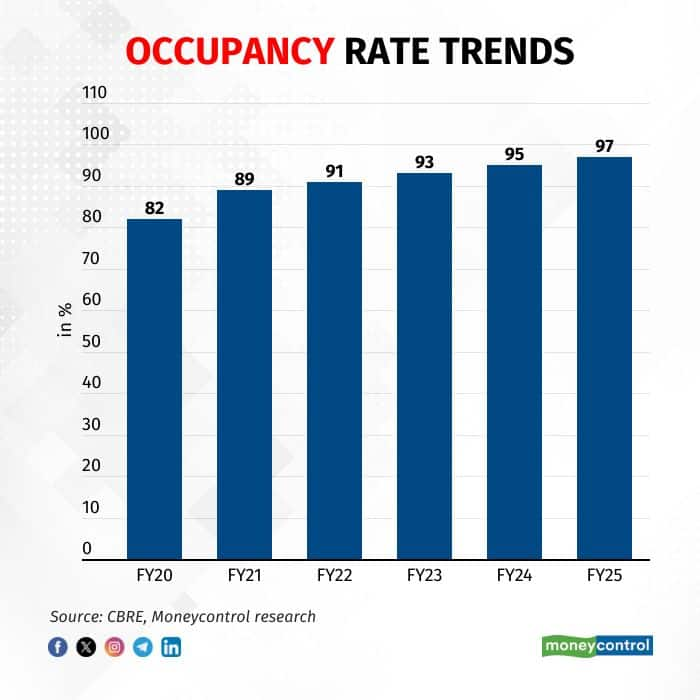

India generates nearly 20 percent of the world’s data but has just 5.5 percent of global data centre capacity, highlighting a significant structural gap in digital infrastructure. As of March 2025, installed colocation capacity stood at 1.67 GW, growing 23.3 percent YoY. Yet, utilisation remained very high at 95-97 percent, indicating persistent undersupply. Long construction timelines of 24-36 months, strong hyper-scaler pre-commitments, and rising AI-driven power intensity limit near-term oversupply risks, keeping vacancies low, ramp-ups predictable, and pricing discipline intact.

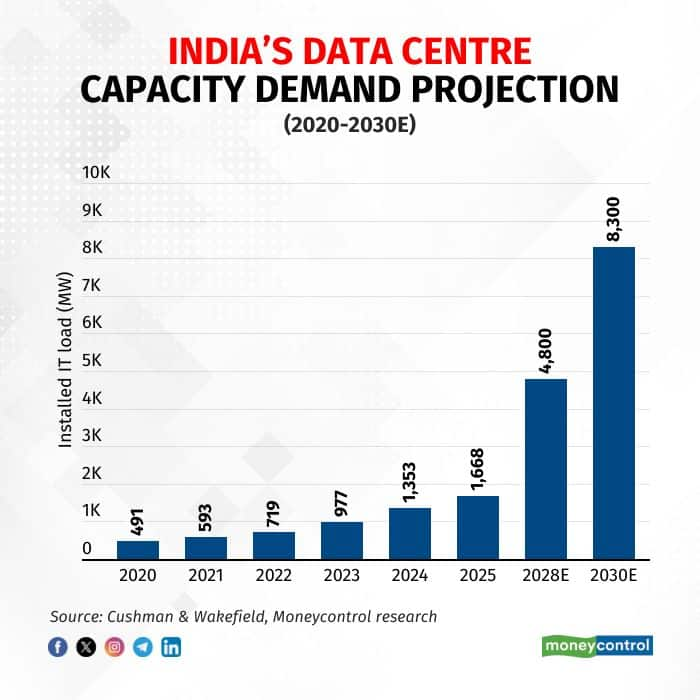

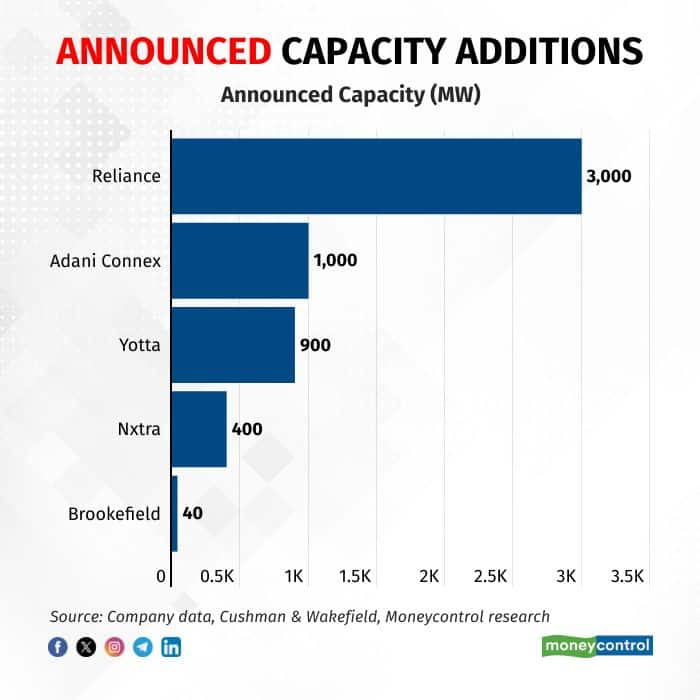

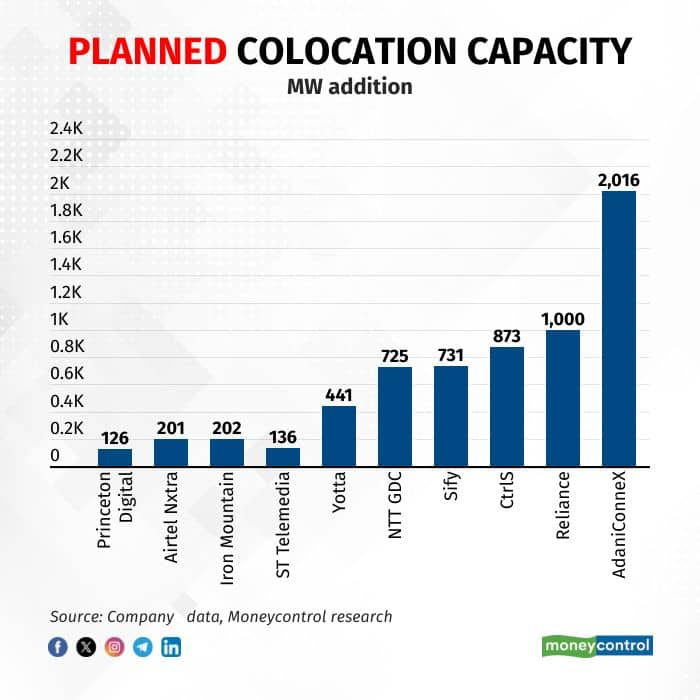

Based on announced projects and firm expansion pipelines, 4.5-5 GW of colocation capacity is visible by FY28, implying a robust 35-37 per cent CAGR from FY24 levels. With sustained hyper-scaler demand and rising AI-led rack densities, total installed capacity could reach ~8 GW by the end of the decade. Notably, nearly 50 percent of planned additions are driven by AdaniConneX and Reliance-backed platforms, pointing to a consolidated, disciplined supply build-out rather than fragmented overcapacity. This committed capacity expansion is driven largely by hyper-scaler demand rather than speculative enterprise builds, ensuring strong utilisation visibility and limited downside risk. Even after planned additions, India’s data centre density remains far below that of the US and China, highlighting significant long-term headroom.

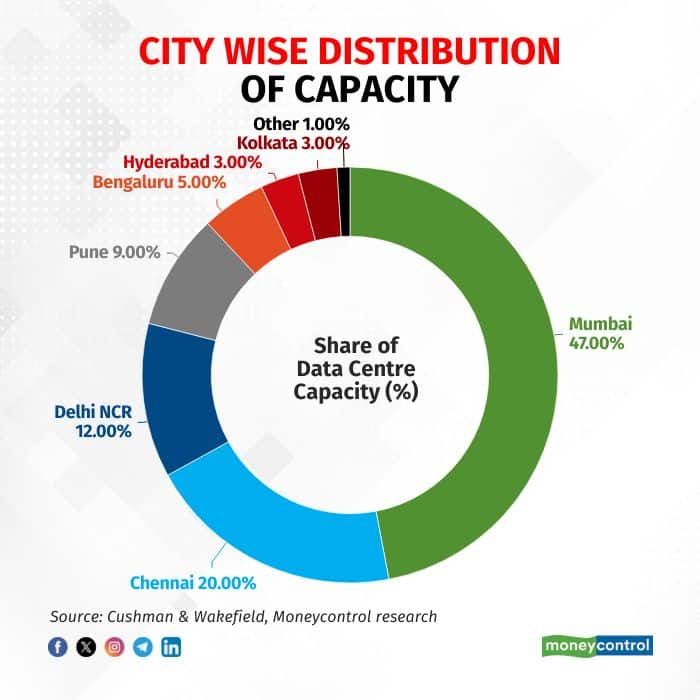

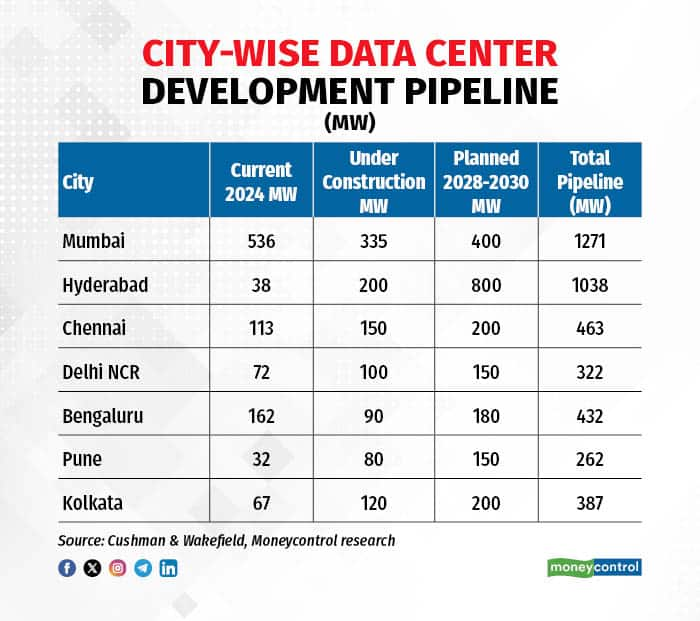

Capacity is geographically concentrated, with Mumbai accounting for 45-50 percent and Chennai 18-20 percent of installed capacity. Delhi-NCR, Pune, Bengaluru, and Hyderabad form the next growth cluster, with gradual expansion into select Tier-2 cities over time.

The key demand drivers of data centre boom

Rising AI adoption

Accelerating enterprise cloud adoption and AI investments are driving robust data centre demand, with partnerships like Google-Adani, Reliance’s AI push, and Microsoft’s expanding Azure capex underscoring confidence in India’s long-term compute needs.

Policy push fuelling hyper-scaler investments

Hyper-scalers already account for around 60 percent of leased colocation capacity, a share set to rise as AI workloads scale up.

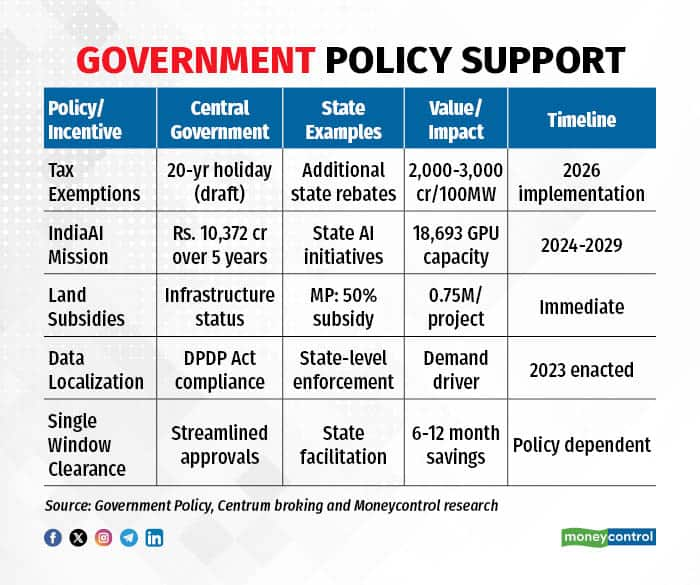

India has become a priority market for global hyper-scalers due to its scale, regulatory push, and long-term demand visibility. Data localisation mandates from the RBI, SEBI, and the Digital Personal Data Protection Act (DPDP) require sensitive data to be stored domestically and effectively, compelling hyper-scalers to build or lease local infrastructure. This is reinforced by strong government support through infrastructure status, policy incentives, and state-level data centre policies. IndiaAI Mission has allocated over Rs 10,000 crore for GPU (graphics processing unit) infrastructure, creating a strong catalyst for AI-ready data centres which will host these high-power GPUs.

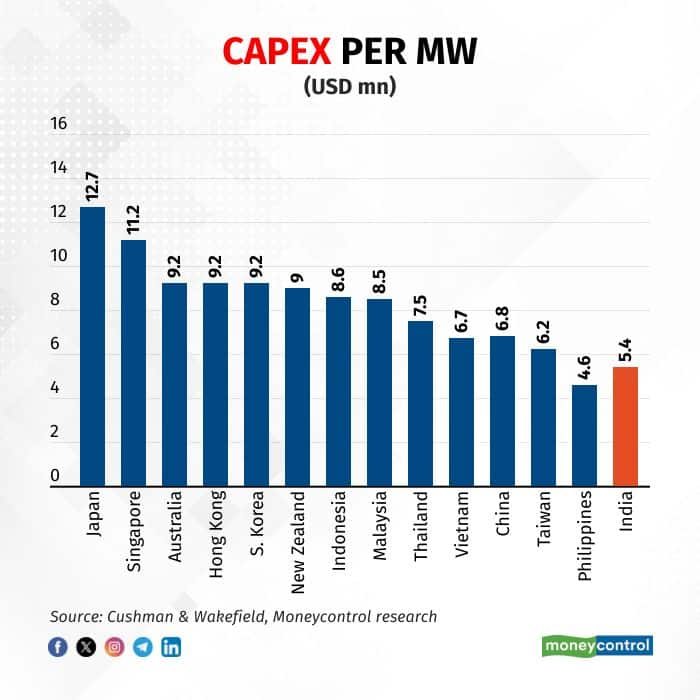

India’s cost-efficient model strengthens data centre economics

India offers one of the lowest capex per MW among major global data centre hubs such as Singapore, Tokyo, Sydney, and Hong Kong, supported by lower construction costs, affordable labour, and access to large land parcels.

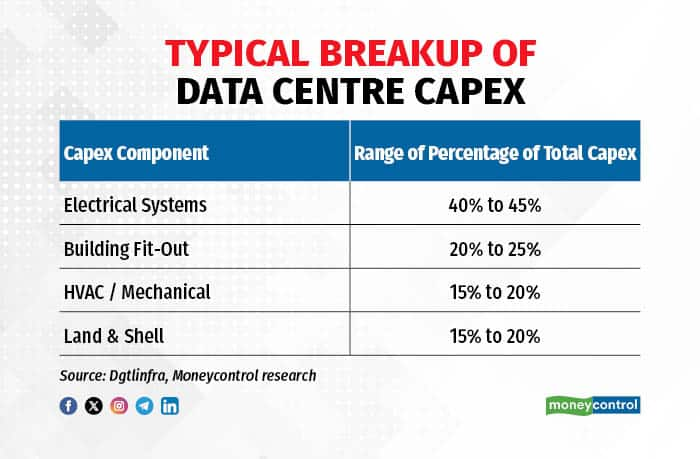

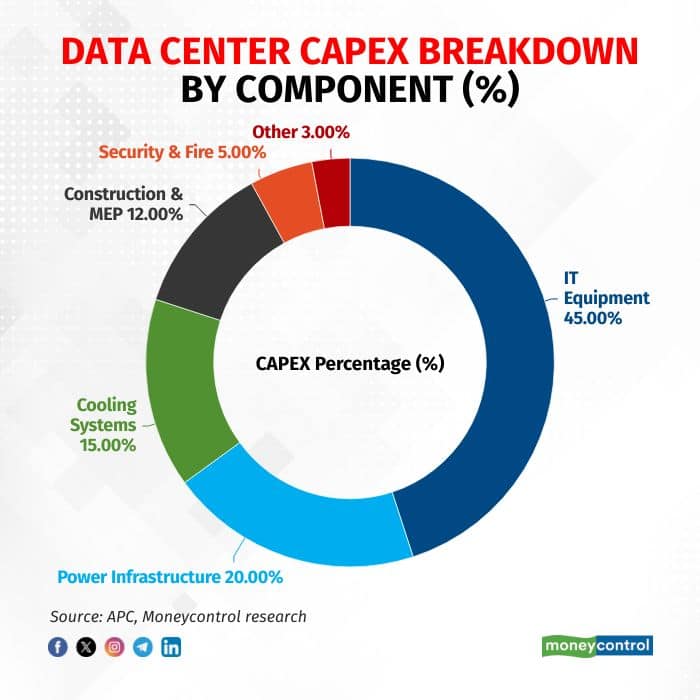

Average colocation capex stands at Rs 400-430 million per MW (~ $5 million/MW), among the lowest globally, with power and electrical systems accounting for 40-45 percent of total costs. Since utilities are largely pass-through, operators are able to protect margins. At steady state, data centre operators can generate EBITDA margins of 40-50 percent, supported by long-term contracts, with power efficiency emerging as a key performance metric.

Opportunity beyond data centre operators

The data centre investment opportunity extends well beyond operators, creating a broad-based investment theme across the ecosystem. At the core are large, well-capitalised platforms that build, own, and lease facilities under long-term contracts. Players such as Nxtra Data (Bharti Airtel), Reliance, and AdaniConneX are strategically positioned and could together account for nearly 50 percent of India’s capacity by 2030, alongside established names like NTT GDC and Sify with sizeable expansion pipelines.

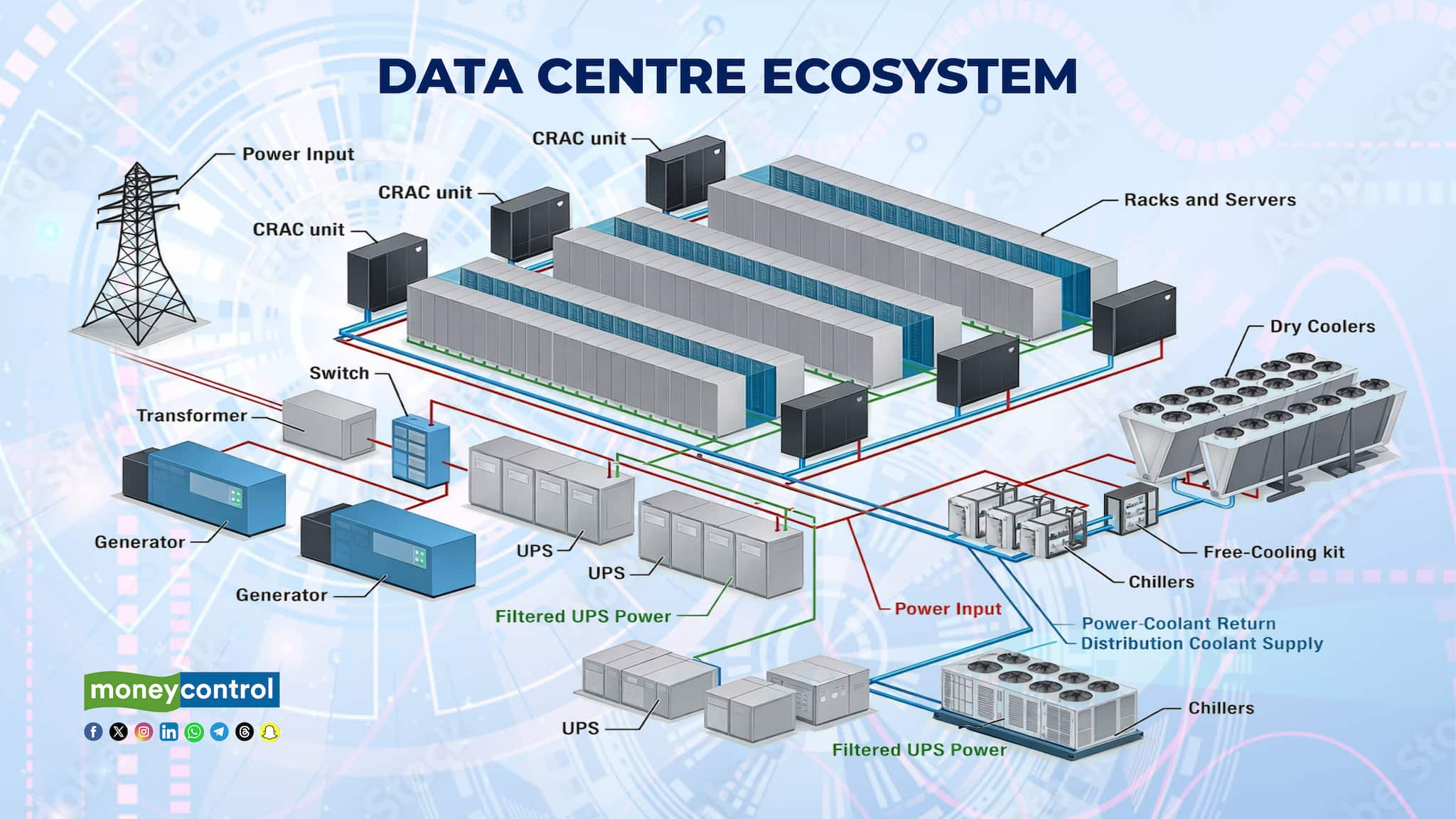

Beyond operators, a wide ecosystem stands to benefit. Electrical and mechanical systems such as transformers, UPS, switchgear, power distribution, and cooling account for over half of data centre capex.

For investors, the opportunity spans operators, power and cooling suppliers, EPC players, and IT hardware providers making data centres one of the most durable and comprehensive plays on India’s next growth cycle. Moneycontrol Research has identified 17 proxy and surrogate plays to participate in India’s data centre boom. MC Pro subscribers can access the list for the stocks here. Non-subscribers can sign up for a Moneycontrol Pro subscription at any time for investment related content and curated stock ideas.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.