Krishna Karwa

Moneycontrol Research

India’s leading organised retailers reported a mixed set of numbers in Q2 FY19. Revenue growth was either subdued or below expectations due to postponement of festive season sales to Q3.

In comparison, top-line traction was seen in late Q2 and early Q3 in FY18. Therefore, retailers were forced to take price cuts to clear pre-festive inventories. Investments in store additions/refurbishment, an increase in employee costs, low conversion-to-footfall rates and build-up of working capital led to a dip in margins of most companies.

Q2 snapshot

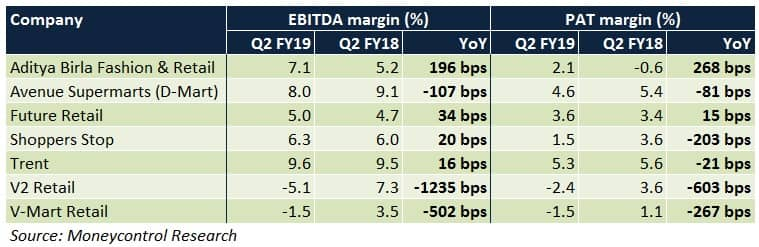

Aditya Birla Fashion and Retail (ABFRL) and Future Retail were the standout performers on the back of decent year-on-year (YoY) sales growth and a visible improvement in margins. In contrast, V2 Retail and V-Mart were the big laggards.

The path ahead

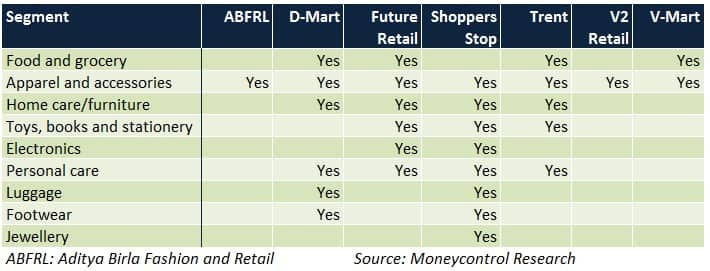

A differentiated business model (on fronts such as brands, network, strategies, product positioning etc) has enabled each company to create a niche for itself in an industry where margins can be pretty thin and achieving high asset turns could be quite a challenge.

Going forward, here’s what investors need to bear in mind from a company-specific perspective:-

Aditya Birla Fashion and Retail

Revenue drivers: Around 250-300 new stores will be added every year under Madura and Pantaloons. Branded innerwear is expanding rapidly too. Premium brands under Madura are capable of delivering strong same-store sales growth and steady cash flows. In Pantaloons, the product portfolio will be refreshed periodically to cater to a wider customer base.

Margin drivers: Most store additions will be under the franchise route to limit capex. Turnaround strategies in Pantaloons have begun bearing fruit. More unprofitable outlets in the fast fashion segment (brands: Forever 21 and People) may be shut to facilitate cost savings.

Avenue Supermarts (DMart)

Revenue drivers: About 25-30 stores will be added each year, of which some could be on lease as well. DMart Ready, the company’s online platform that manages home delivery processes and includes collection centres for orders placed, is expanding its reach from metros and Tier I cities.

Margin drivers: Adoption of a cluster format, wherein new outlets are situated in a 100-150 km radius from the existing ones, would result in lower logistical costs. The company’s product mix is also being tweaked in favour of non-food items. Exposure to long-term debt will be trimmed from proceeds of its initial public offer.

Future Retail

Revenue drivers: Convenience stores (Easyday, Heritage Fresh) will be aggressively added to achieve last mile connectivity. About 100/200 Big Bazaar/Fashion at Big Bazaar outlets will be operational over the next 4-5 years, respectively. Partnership with Amazon would be crucial in bolstering product visibility.

Margin drivers: Loss-making eZone stores (pertaining to electronics and consumer durables) are being phased out. Integration of operational similarities between Hypercity with Big Bazaar is underway.

Shoppers Stop

Revenue drivers: Around 4-5 large format stores (i.e. Shoppers Stop) and 8-10 premium beauty product stores will be added in each fiscal year. Kiosks, experience centres and personalised customer services should help the company attract more footfalls. Women’s ethnic wear is a fast-growing segment too.

Margin drivers: Contribution of the company’s own brands to total sales is likely to increase to 30-35 percent by FY20 from 10-15 percent at present. Scaling up of omnichannel operations should normalise marketing expenses (as a percentage of sales). The product mix is moving in favour of branded beauty products, where margins are usually better than apparel. Repayment of long term borrowings in entirety is on the cards as well.

Trent

Revenue drivers: About 30 outlets will be added every year under Westside and Star Market formats, which deal in clothing and grocery products, respectively. Zara/Zudio outlets will be opened to capitalise on growing demand for high-end/value fashion, respectively. Tata CLiQ, the company’s online arm, is also being developed further.

Margin drivers: Private label products, which constitute 90-95 percent of Westside sales, should help achieve high same-store sales growth. More brands may be launched in this space. Medium-sized grocery stores will be opened in a cluster format to keep operating costs low. Landmark stores, that cover books and stationery, have managed to break-even after facing years of losses.

V2 Retail

Revenue drivers: Store rollouts will be undertaken, primarily in northern and north-eastern India, to add 2 lakh square feet of retail space by FY19-end, thus taking the total to 1 million sq ft. The company is setting up a B2B platform to tie-up with mom-and-pop stores in rural India.

Margin drivers: To improve supply chain processes, distribution centres are being established to reduce dependence on external warehousing. The share of owned brands is slated to rise to 30-35 percent over the next two years from 20 percent at present.

V-Mart

Revenue drivers: Early onset of winters in northern India, the largest market for the company, should lead to an uptick in winter/thermal wear volumes. Most of the top-line growth will be volume-based to address the requirements of value-conscious clothing buyers. Adequacy of rainfall, an increase in minimum support price for food grains and pre-election activities will be critical in determining the rural demand trajectory. Store additions in eastern and north-eastern India are lined up too.

Margin drivers: In the kirana segment, the focus is shifting to high-margin products such as personal care, deodorants, chocolates and hand sanitisers. Economies of scale through bulk sourcing are being prioritised. The contribution of private labels is expected to increase from the 60-65 percent mark in FY18.

Outlook

Q3 will be a better quarter sequentially (ie. vis-à-vis Q2) for the sector as a whole because of festive and wedding season sales. Network augmentation is anticipated to accelerate in H2 FY19 to cash in on this demand rush.

Owing to a large population base, higher disposable income and deeper penetration of organised retail into smaller cities, we see India's consumption story remaining intact in the years to come. So, revenue visibility shouldn’t be a cause of concern for any retailer, even though some degree of seasonality may be seen in a few quarters.

The main differentiator, however, will be margins. Operating leverage, rationalisation of fixed overheads, quicker operationalisation of new outlets and closures of loss-making stores/segments are among the key objectives that retailers would want to focus on in a bid to boost their bottom-line.

Additionally, a lot would depend on how risks associated with sluggish sales in the offseason, high competitive intensity and rising rent costs for commercial properties are addressed.

Which stocks should you pick?In spite of market volatility, retail stocks continue to trade at fairly demanding valuations.

DMart has been priced to perfection for long. To command such high valuations over extended periods of time, the company will have to deliver industry-leading top-line growth and superior margin consistently. This could be difficult considering the management’s impetus towards sales growth, even if it results in some bit of margin moderation. In our view, better entry opportunities may be available at a later stage.

Notwithstanding the disappointment in Q2, V-Mart is one of the best performers in the Indian retail space. The company’s ambitious expansion plans and healthy fundamentals appear to be incorporated in the price. This, coupled with the stock’s steady rally in recent months, leaves little on the table for new investors at present.

ABFRL and Trent’s steep valuations suggest that prospects of a major upside are pretty remote, at least in the foreseeable future. Nevertheless, we don’t see any significant downside from current levels either since these stocks, despite the volatility in markets, have been fairly range-bound. Both names are investment-worthy.

While Shoppers Stop is expected to be a big beneficiary of the tie-up with Amazon and also has a large customer loyalty programme coverage, V2 Retail aims to improve profitability by strengthening its retail coverage in semi-urban and rural India. Since both stocks are trading close to their 52-week lows at this point, investors may consider taking advantage of the price correction.

Future Retail, by virtue of its diverse pan-India network and stake sale agreement with Amazon, is already a big force to reckon with. Consolidation of the business structure through phasing out of non-core segments should unlock value. The stock may be considered for the long-term.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!