Jitendra Kumar Gupta

Moneycontrol Research

HG Infra Engineering, which is into the construction of roads and highways, is one of the very few high quality smallcap companies in the construction space. To put things in perspective, the company earns close to 15-16 percent operating margin and core return on equity (RoE) in excess of 35 percent, which is the best among its peers. Moreover, if we factor in balance sheet strength, cash in the books and ultra-low debt-to-equity of 0.3 percent will mirror a strong franchise like FMCG.

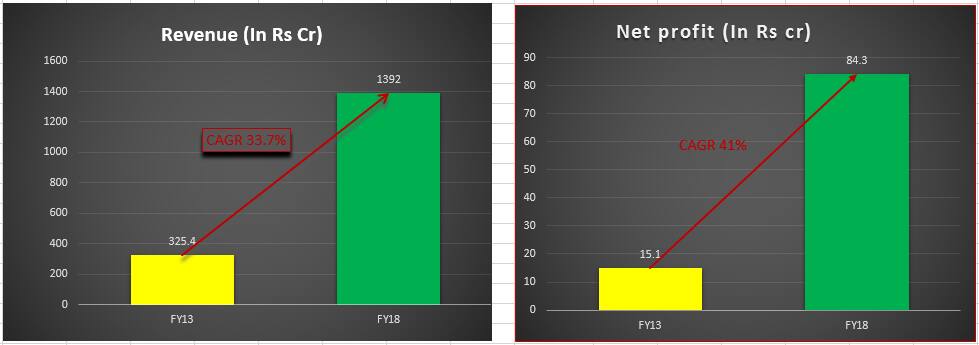

This indicates how prudently the business is run, with a strong focus on balance sheet without compromising on growth. Over the last five years, it has delivered an annual sales and profit growth of 34 percent and 41 percent, respectively.

Source: Company

An efficient business model

The company was largely a subcontractor, but gradually it has moved up the value chain and today it bids for projects as a main contractor. As it has worked as subcontractor in the past, it owns majority of the construction equipment.

Adjusting for cash, fixed assets form 60 percent of the balance sheet. Having its own equipment brings in a unique advantage in terms of cost. It makes the company most competitive in the market, which is also a reason why the company’s project-win (bid-to-award) ratio is one of the highest in the industry. Since it has its own equipment, its execution cycle is low. Also, strong control over its working capital needs reduces its dependence on borrowed funds.

Strong growth visibility

Its business advantages reflect in its growing order book. Over the last five years, its order book has seen a compounded annual growth rate (CAGR) of 45 percent. It is currently sitting on a strong order book of close to Rs 6,850 crore, which is close to five times its FY18 annual revenue, providing strong revenue visibility for the next three years.

A year back, the company raised closed to Rs 300 crore through an initial public offering (IPO). This has expanded its capital and resources, enabling it to speed up execution without straining its balance sheet. With the expansion of capital, its ability to bid for larger projects has increased.

Attractive valuationThe stock has recently corrected from Rs 350 to Rs 270 levels at present, which is near the upper end of its IPO price band. The counter is currently trading at 10 times its FY20 estimated earnings, which is quite attractive. The company is also sitting on a large amount of cash in its books and delivers earnings growth in excess of 30 percent, led by a strong order book. Besides, its strong return ratios and low debt-to-equity should support valuations.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!