Neha Dave

Moneycontrol Research

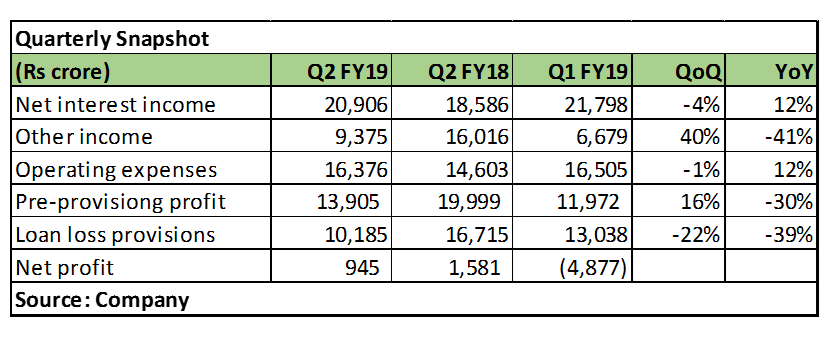

State Bank of India (SBI) reported better-than-estimated earnings, with net profit of Rs 945 crore against street estimate of a loss in Q2 FY19. Profit was mainly aided by a one-time gain from stake sale in general insurance business and lower provisions.

On the asset quality front, lower slippages to non-performing assets and decline in the watch list during Q2 was comforting. Strong pick-up in loan growth, especially corporate advances, was also a positive surprise.

SBI stands out because of its sheer size and relatively better operating performance among public sector banks, which are fast losing their relevance in the financial system. The management’s intention of buying loan assets to the tune of Rs 45,000 crore (Rs 5,000 crore already approved and another Rs 15,000 crore portfolio buyout is in the pipeline) from non-banking financial companies (NBFCs) facing liquidity crunch will further consolidate its market position.

We expect a faster recovery for SBI in contrast to many small-sized public lenders. The management’s guidance of reduced credit cost for FY19 and improvement in return ratios in FY20 is reassuring. With the stock trading at 1.1 times FY20 estimated adjusted core book value, current valuations seems to be pricing in most concerns. Investors should use the consolidation as an opportunity to invest for the long term in the stock.

Quarter at a glance

Net interest income (NII) increased 12 percent year-on-year aided by strong growth in advances book on the back of an uptick in net interest margin (NIM) to 2.88 percent. Margin benefitted due to write-back of interest income on accounts that were upgraded from non-performing to standard category in Q1.

The bank reported de-growth in core fee income due to reduction in charges on maintenance of minimum balance in savings accounts. This along with lower trading income undermined the non-interest income, which dropped by 41 percent YoY.

Operating expenses increased 12 percent, pushing cost-to-income ratio to 56 percent. This was mainly driven by higher staff cost as the bank continued to provide for wage hike and related rise in pension and gratuity expenses.

The bank provided lesser amount for NPAs as incremental slippages were much lesser compared to the last few quarters and also because it anticipates write-back of provisions in coming quarters.

Loan growth accelerates

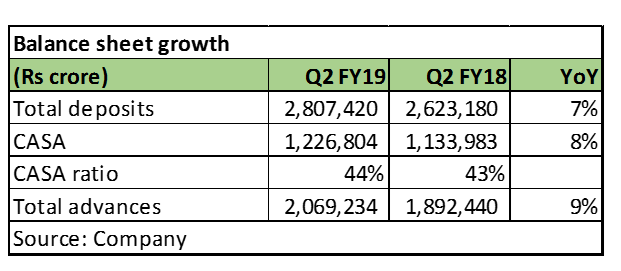

Advances growth was strong (9 percent) as domestic loan book growth at 11 percent was partially negated by flat overseas loan book. The proportion of overseas loans in overall loan book stood at 14 percent as at September-end.

It was heartening to see a pick-up in corporate advances, which increased 14 percent after a prolonged period of cyclical weakness. Growth in retail assets (including SME, agriculture and personal) was 9 percent.

Deposits growth at 7 percent YoY was a tad below growth in advances. Overall performance on the liability front continued to be impressive with low-cost current account-savings account (CASA) deposits around 44 percent of total deposits.

Asset quality improvement continues

Slippages reduced to Rs 10,888 crore in the quarter gone by, which is almost 2 percent of loan book. This, along with higher recoveries and write-offs, led to a sequential decline in gross non-performing assets (GNPA). Bulk of the slippages accrued from non-corporate assets. Within corporate, 75 percent of slippages were from the watch-list, which is comforting.

In addition to GNPAs, stressed asset loan pool, popularly known as watch-list, is key to its future asset quality. The bank’s watch-list declined to Rs 20,359 crore (0.98 percent of loan book) from Rs 24,633 crore (1.2 percent of loans) quarter-on-quarter. The bulk of watch–list consists of power sector-related assets and this remains a key monitorable. SBI’s exposure to Infrastructure Leasing & Financial Services (IL&FS) is around Rs 4,300 crore, much of which is at the special purpose vehicle (SPV) level.

We are most enthused by SBI’s higher provision coverage ratio (PCR) of 71 percent. PCR on corporates undergoing resolution through the National Companies Law Tribunal (NCLTL) list I and II stood at 66 percent and 81 percent, respectively, as at September-end. Resolution of NCLT cases will lead to lower GNPAs and better margin. It could lead to possible write-back of provisions as PCR on these cases is healthy. For instance, the management expects a provision write-back of Rs 6,000 crore from resolution of NCLT I accounts.

Best positioned to play the asset cycleWhile reported earnings were modest, we are encouraged by the improving outlook. While some asset quality pain might persist for a couple of quarters, the end seems certainly near. We expect earnings to gain traction as credit cost trends downwards over the next two years and the management leverages capital for loan book growth.

Last quarter, the management articulated its strategy, which it endeavours to achieve by March 2020. It aims to deliver consolidated return on asset (RoA) of 0.9-1 percent, reduce GNPA to below 6 percent, and maintain provision cover above 60 percent by March 2020. With much lower slippages expected for FY19 at 2 percent, which will result in normalisation of credit cost, the target looks achievable. Capital could be a constraint in delivering the target, but a successful equity raising in the near term will be an added trigger.

With a potential improvement in return ratios, the current valuation of 1.1 times FY20 estimated adjusted book for the core business looks undemanding. With a turnaround in sight, investors looking to play the asset recovery and resolution cycle should buy into the stock for the long term.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!