Neha DaveMoneycontrol Research

Highlights

-Accounting profit dragged down by higher commissions

-Strong premium growth at almost double of industry growth rate

-Combined ratio improved , investment yields moderated

-Regulations supports the sectoral growth

-Premium valuation offers limited upside

------------------------------------------------

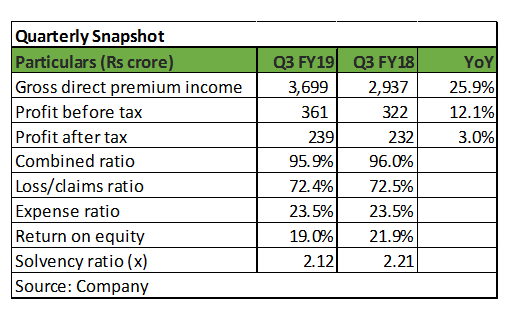

ICICI Lombard General Insurance, India's largest private sector non-life insurer, reported muted Q3 earnings with net profit rising 3 percent YoY to Rs 239 crore in Q3 on higher commission costs and lower investment yields.

However, the insurer's subdued profit growth in Q3 is an optical illusion. As per accounting rules, commissions paid to agents is recognised upfront while premium income is amortized over four quarters. Upfront expensing of acquisition cost incurred to achieve higher business growth dragged down the insurer's profit (referred to as new business strain) in Q3. Overall business growth and operating performance remained healthy.

While there is inherent volatility in its core risk-underwriting business, ICICI Lombard is better positioned in the sector with market share of around 8 percent among all non-life insurance companies, making it a stock worth looking at.

Robust growth in premium

ICICI Lombard reported solid growth of 25.9 percent year-on-year (YoY) in Gross Direct Premium Income (GDPI), as against industry growth rate of 13.6 percent in Q3 FY19, mainly driven by motor insurance. Consequently, it consolidated its position as the largest private non-life player and overall fourth largest player in the general insurance industry.

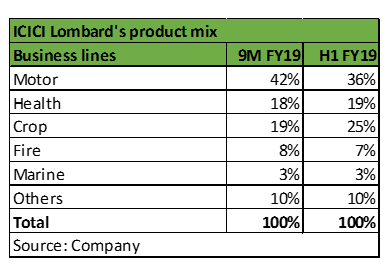

While the insurer maintains a diversified portfolio, mandated longer tenure policy in third party motor insurance by the Supreme Court benefited ICICI Lombard disproportionately, as its presence in the segment is well above the industry average. As a result, share of motor insurance in product mix increased to 42 percent as on end-December as compared to 36 percent at previous quarter end.

Management expects overall premium to continue to grow at 15 percent-20 percent in medium- to long-term. The insurer remains cautious on government related business segments like crop insurance and mass health.

Improvement in operating metrics

The combined ratio, measure of insurance company's profitability, improved to 95.9 percent in Q3 from 101.1 percent in Q2. The insurer’s combined ratio was higher in the last quarter due to higher claims because of Kerala floods.

The overall underwriting performance was dragged by higher losses in the crop insurance with claims ratio at 116.9 percent for the 9M FY19. All other segments reported moderate claims ratio (below 100 percent).

The weak underwriting performance was offset by investment income. Despite the insurer's yield on investment assets declining to 7.3 percent in 9M FY19 compared to 7.7 percent in 9M FY18, investment income grew by 14 percent as investment assets increased by 18 percent during the same period.

Capitalisation is adequate for ICICI Lombard as reflected in its solvency ratios at 212 percent, comfortably above the regulatory requirement of 150 percent.

Huge sectoral opportunities

The general insurance industry in India has witnessed compounded annual growth rate (CAGR) of 17 percent in GDPI from CY01 to CY17. There are several growth levers that will drive high-teen growth over the next few years as well. India continues to be a grossly underpenetrated market with a non-life penetration at one third of the global average in CY17. The insurance density (non-life insurance premium per capita) also remains significantly lower than other developed and emerging market economies.

Progressive regulations to drive growth

Regulations continue to be progressive and supportive of growth in the sector.

For instance, GST rate on third-party motor insurance premium in case of goods carrying vehicles was reduced from 18 percent to 12 percent effective from January 1, 2019. The reduction in tax rate is expected to lower the cost of insurance, thereby making it affordable, which is a positive change for the general insurance industry.

In another circular, the Regulator has unbundled and de-tariffed compulsory personal accident cover.

From September 2018, following the Supreme Court's order, the regulator made third party (TP) insurance cover for new cars and two-wheelers mandatory for a period of three years and five years, respectively. This was a big positive development since it is expected to address the problem of non-renewal of motor insurance in case of older vehicles and drive growth in motor insurance premium.

Competitive advantage aids premium valuations

ICICI Lombard is well poised towards earnings growth with an increase in insurance penetration, focus on profitable segments and improvement in operating efficiency. The stock is currently trading at 7.7 times its trailing book. The current valuation is rich even after considering high return on average equity at over 21 percent.

We have seen that leading companies in the secular growth sector tends to trade at higher multiples for a long period of time. In the absence of suitable and comparable listed peer, ICICI Lombard trades as a proxy for the sector commanding a higher valuation. While the premium valuation will sustain, near term upside in stock price is limited. Nevertheless, investors with long term horizon and wanting to participate in the growth in non-life insurance sector, can consider buying the stock on dips.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!