Highlights:

- Strong Q1 FY20 performance driven by growth coming in from export markets

- Business outlook weak for short term, positive for long term

- New avenues for growth and diversification across geographies

- Attractive valuations

Despite slowdown in the automobile industry both in India and abroad, GNA Axles posted a strong set of numbers for the first quarter of FY20. It registered a very strong growth in its net revenues and witnessed operating profit margin expansion, led by cost control measures and a fall in raw material prices.

GNA’s dominant position, robust clientele, new avenues for growth and encouraging Q1 FY20 quarterly finance performance coupled with reasonable valuations (7.4 times FY21 projected earnings) make this worth buying for the long term.

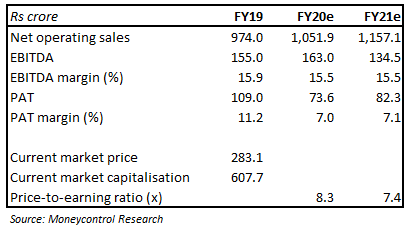

The quarter at a glance

Key highlights

Despite slowdown in domestic commercial vehicle (CV) segment and in Class 8 truck demand in North America (NA), GNA posted a very strong year-on-year (YoY) growth of 21 percent in its net revenues in Q1 FY20. The growth was primarily due to the traction coming in from the NA market where GNA got new business from its existing customers. The growth from India, on the other hand, has been subdued.

In terms of operating profitability, GNA posted a 31 percent YoY growth in its earnings before interest, tax, depreciation and amortisation (EBITDA). EBITDA margin witnessed an expansion of 113 bps, led by cost control measures and higher margins that GNA fetched from exports.

Outlook

Industry outlook – Sluggish in the near term

Subdued demand for Class 8 trucks in North America has not yet affected the growth for GNA as it continues to have a strong order pipeline and win new orders from the clients. The management indicated that the order book is strong for the next two quarters and expects to have a run rate of Rs 250 crore. However, growth from European markets is expected to be muted at 3-4 percent.

GNA’s strategy to expand its footprint by targeting other geographies such as Australia and South America is expected to help de-risk the business from significant dependence on North America and Europe.

The management’s outlook on Indian market is not very encouraging. The demand for commercial vehicle is slowing on the back of weakening macroeconomic environment. The demand from tractors has also peaked last year and is expected to be down in the current fiscal.

The outlook continues to be weak for the short term, but we believe long-term outlook is promising on the back of infrastructural development, increasing economic activity, rising rural income levels and lower penetration. In the short term, what could lend support to CV demand is upcoming BS VI emission norms, to be implemented from April 2020. The new emission norms are expected to lead to pre-buying as BS VI compliant vehicles would be more expensive than the current vehicles.

Overall, the management has guided 8-10 percent revenue growth in FY20, much lower than 21 percent growth it registered in Q1 FY20.

On a new turf

To further fuel growth and diversify from CV and off-highway segments, GNA has started entering SUV and LCV axle shaft segments. The company has chalked out plans to set up a manufacturing facility with initial capacity of 600,000 units. It's focusing on acquiring customers from North America, Europe and India in that order. The commercial production of this facility is expected to commence from March 2019.

Attractive valuationsThe company is trading at 8.3 and 7.4 times FY20 and FY21 projected earnings, respectively, which is very attractive.

For more research articles, visit our Moneycontrol Research page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.