The initial public offering (IPO) of Ujjivan Small Finance Bank, the subsidiary of Ujjivan Financial Services, will open for subscription on December 2.

This would be 12th company launching main board IPO in the current financial year 2019-20. The issue will close on December 4.

Kotak Mahindra Capital Company, IIFL Securities and JM Financial are book running lead managers to the issue. Equity Shares proposed to be listed on the National Stock Exchange (NSE) and Bombay Stock Exchange (BSE).

Here are 10 key things to know before subscribing the issue:

Company profile

Ujjivan Financial Services (UFSL) received the Reserve Bank of India (RBI)'s in-principle approval to establish an Small Finance Bank on October 7, 2015, after which it incorporated Ujjivan Small Finance Bank Limited as a wholly-owned subsidiary.

UFSL, subsequent to obtaining RB's final approval on November 11, 2016 to establish and carry on business as an SFB, transferred its business undertaking comprising of its lending and financing business to bank, which commenced its operations from February 1, 2017.

The bank included in the second schedule to the Reserve Bank of India Act, 1934 as a scheduled bank on July 3, 2017.

Promoter, UFSL commenced operations as an NBFC in 2005 with the mission to provide a full range of financial services to the ‘economically active poor’ who were not adequately served by financial institutions.

The bank continued to focus on lending to micro banking customers with deposits from its micro banking customers constituting 6.75 percent of its total deposits as of September 30, 2019.

Issue details

The company launched the IPO with a price band of Rs 36-37 per equity share, a premium of Rs 26-27 over its face value of Rs 10 each.

The issue includes a reservation of Rs 75 crore worth of shares for subscription by eligible shareholders of Ujjivan Financial Services. They will get shares at a discount of Rs 2 per share.

Minimum bid lot is 400 equity shares, and in multiples of 400 equity shares thereafter.

Fund raising

The company is aiming to raise Rs 750 crore through this public issue.

The lender has already raised Rs 250 crore through pre-IPO placement of 71,428,570 equity shares.

Objects of the issue

The bank has proposed to utilize the net proceeds from the issue towards augmenting its tier – 1 capital base to meet its future capital requirements.

Further, the proceeds from the issue will also be used towards meeting the expenses in relation to the issue.

Shareholding and management

Ujjivan Financial Services (UFSL) is the promoter of the company, holding 1,44,00,36,800 equity shares (representing 94.40 percent of paid-up equity capital). It also included one equity share each held by Samit Kumar Ghosh, Carol Furtado, Sudha Suresh, Rajat Singh, Ittira Davis and Premkumar G, as nominees on behalf of UFSL, who is the beneficial owner of such equity shares.

Samit Kumar Ghosh is the Managing Director and Chief Executive Officer of the bank while Sunil Vinayak Patel is the part-time Chairman and independent director.

Jayanta Kumar Basu and Mona Kachhwaha are non-executive directors while Chitra Kartik Alai is the non-executive nominee director.

Sachin Bansal, Biswamohan Mahapatra, Prabal Kumar Sen, Nandlal Laxminarayan Sarda, Vandana Viswanathan, Mahadev Lakshminarayanan and Luis Miranda are independent directors.

Strengths

> The bank has deep understanding of mass market serving unserved and underserved segments.

> It is a customer centric organization with multiple delivery channels.

> The bank has pan-India presence, providing services in 24 states and Union Territories encompassing 232 districts in India as of September 2019.

> It has technology driven operating model with advanced digital platform.

> It has established robust risk management framework to identify, measure, monitor and manage credit, market, liquidity, IT and operational risks.

> It has professional management, experienced leadership with focus on employee welfare.

> It has strong track record of financial performance.

Strategies

> The bank targets to diversify product offerings to enable multiple customer relationships.

> It continues to focus on technology and data analytics to grow operations.

> It aims to strengthen liability franchise and focus on increasing retail customers base.

> It wants to expand distribution network to increase customer penetration.

> It aims to focus on developing responsible banking behavior for unserved and underserved segments.

> It targets to diversify revenue streams.

Financials and peer comparison

The bank has grown in a sustainable manner. Its gross advances (including securitization/ IBPC) have grown from Rs 6,383.98 crore as of March 31, 2017 to Rs 11,048.59 crore as of March 31, 2019 and were Rs 12,863.64 crore as of September 30, 2019.

Its deposits have increased from Rs 206.4 crore as of March 31, 2017 to Rs 7,379.44 crore as of March 31, 2019 and were Rs 10,129.85 crore as of September 30, 2019.

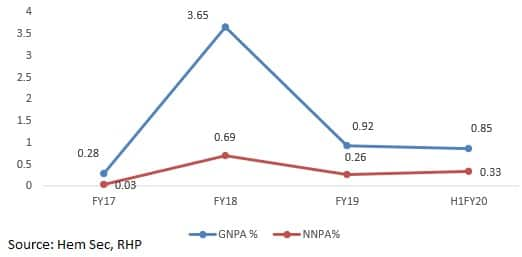

As of September 2019, bank's percentage of gross NPAs to gross advances was 0.85 percent while its percentage of net NPAs to net advances was 0.33 percent.

The bank's profit after tax as restated for fiscal 2018 and 2019 was Rs 6.86 crore and Rs 199.22 crore, respectively while for the six months ended September 2019, its PAT was Rs 187.11 crore.

Further, its long term bank facilities have been rated A+; stable by CARE Ratings, its certificate of deposits have been rated A1+ by CRISIL.

Asset products

On the liability side, bank offer savings accounts, current accounts and a variety of deposit accounts. In addition, it also provide non-credit offerings comprising ATM-cum-debit cards, Aadhaar enrolment services, distribute third party insurance products and point of sales (POS) terminals.

The bank's focus on the financially unserved and underserved segments enables it to comply with RBI’s requirements that: (i) small finance banks locate at least 25 percent of their banking outlets in unbanked rural centres (URCs), and (ii) at least 75 percent of adjusted net bank credit (ANBC) be made to 'priority sectors', which includes micro loans and were able to comply with such guidelines within the first year of its operations.

As of September 2019, 25.54 percent of USFB's banking outlets were located in URCs and its 'priority sector advances' net of PSLC and IBPC were 77 percent of ANBC.

It had the most diversified portfolio, spread across 24 states and union territories as of March 31, 2019, as per a CRISIL report. As of September 30, 2019, it served 4.94 million customers and operated from 552 banking outlets that included 141 banking outlets in unbanked rural centres and additionally operated four asset centres.

As of September 2019, it had a network of 441 ATMs (including 18 ACRs), two 24x7 phone banking units based in Bengaluru and Pune, and a mobile banking application.

Risk factors

The bank has a limited operating history as an SFB. Its future financial and operational performance cannot be evaluated on account of its evolving and growing operations. Accordingly, future results may not be reflective of its past performance.

Further, bank cannot effectively compare its financial statements for fiscal 2017 with its financial statements for fiscal 2018 and 2019 due to non-comparable reporting periods.

The bank has a lack of collateral back up in case of some MSE loans.

It has competition from other SFBs, NBFCs, MFIs and cooperative banks.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.