Historical analysis shows volatility is expected to fall after today’s election result event, also known as an IV Crush. Historically, volatility built up for major events such as elections sees a steep fall after the event day.

“This week, we expect a reduction in volatility, technically referred to as a volatility crush. Typically, a market-impacting event leads to an irrational increase in implied volatilities (IVs) of options. This primarily occurs due to the fear and uncertainty surrounding the event's outcome,” said Sahaj Agarwal, Head of Derivatives Research at Kotak Securities.

According to Agarwal, “High implied volatilities are attractive for option sellers and provide momentum for option buyers. The transition back to a low IV regime is often drastic, making risk management crucial. As the event progresses and certainty sets in, IVs collapse and return to normal levels.”

“To put things in perspective, India VIX made a low of 10 and is currently trading around the 24 mark, having peaked at 26. The previous 15-month average for India VIX is observed at 13-15. Therefore, expect an IV crash and a sudden drop in options premiums, along with the impact of the underlying movement, referred to as delta,” said Agarwal.

“Volatility index INDIAVIX has witnessed a sharp cool-off after exit polls. It has tumbled by nearly 15 percent and ended below the 21 mark. On a daily scale, it has formed a sizeable bearish candle. Going ahead, any sustainable move below the level of 18.50 will lead to a sharp decline in India VIX,” said Sudeep Shah, DVP and Head of Derivative and Technical Research at JM Financial.

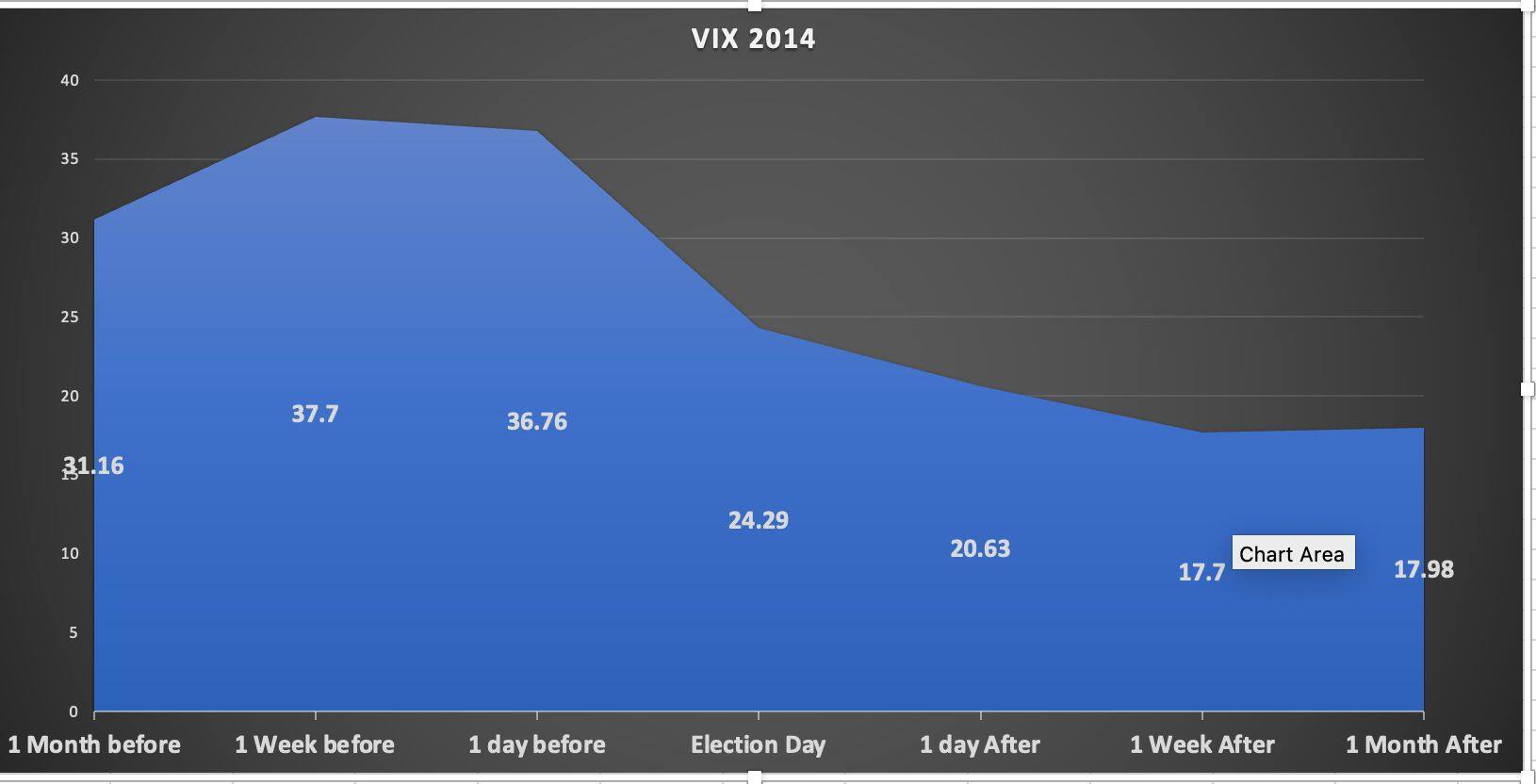

In 2014, when the NDA came to power, Nifty rallied 13 percent in two months, but on the day of the election result, no big surprises or movements occurred. The next day, this resulted in a huge IV crush in options data, and VIX dropped significantly post-event.

Follow our live blog for all market updates

The day after the result, VIX crashed another 15 percent. So, in just two days, VIX crashed more than 45 percent, leading to erosion in premium prices. Option sellers who played with risk-defined strategies during this time period would have made good profits.

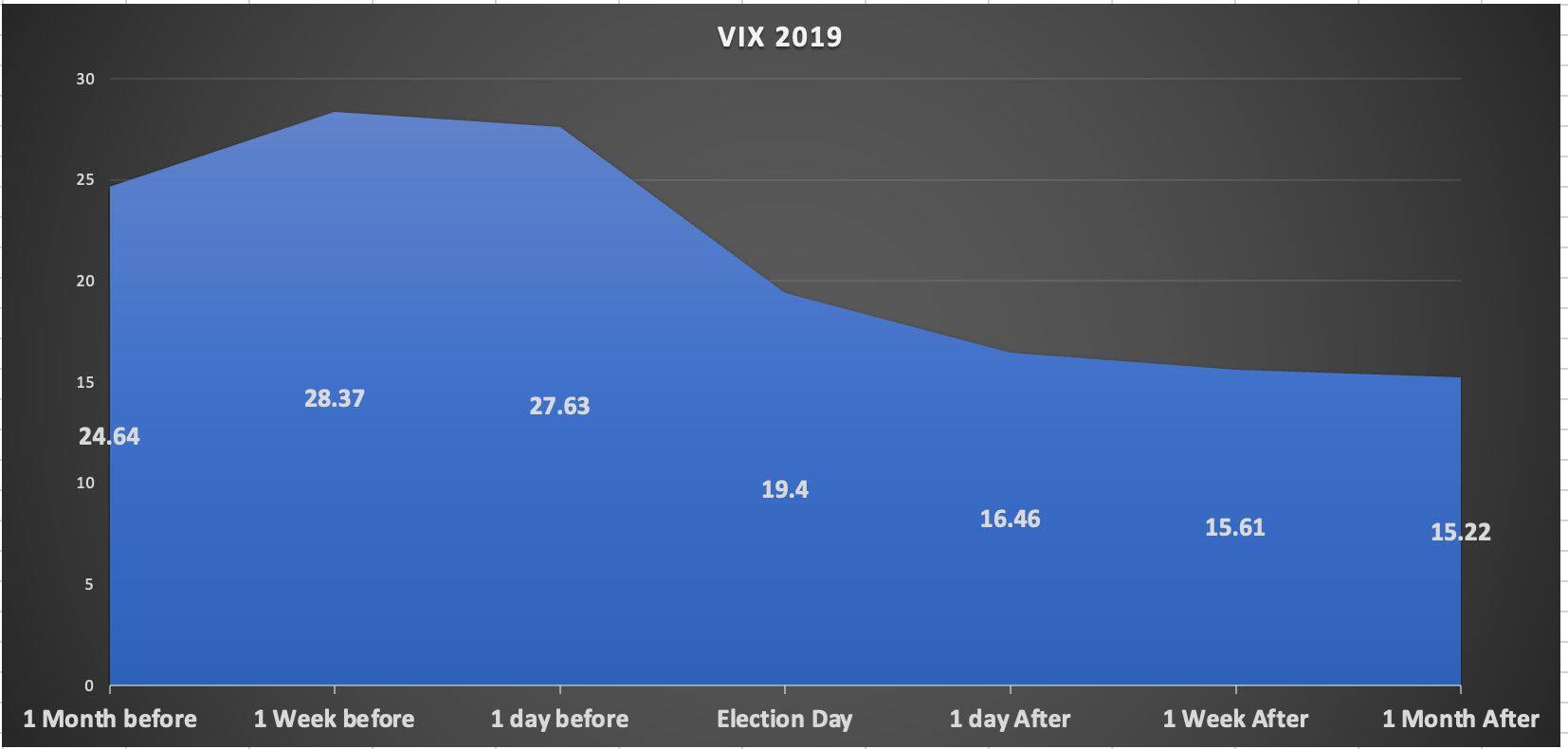

In 2019, VIX crashed 30 percent on the day of the result. The next day saw an additional 15 percent crash in VIX, another episode of premium erosion in options. A more than 45 percent crash in VIX resulted in good profits for option sellers who took positions just one day before the result.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.