The market has not seen any strong move on either side for last one-and-half-month after showing a recovery in April.

The rising cases of new infections, worries over economic and earnings growth due to lockdown, and increasing tensions between US and China continued to worry the market participants.

On the other hand, stable oil prices, fiscal & liquidity measures by RBI and the government, and hope of further opening up of economy saved the market from completely losing ground.

Experts feel the market will remain rangebound in coming months unless there is decline in new infections and US-China trade tensions will continue to weigh on global sentiment.

"Recently the stimulus package of Rs 20 lakh crore gave an emotional uplift to the stock market, however, we believe the Indian stock market will follow the global trend in the medium term," Amit Jain of Ashika Wealth Advisors told Moneycontrol.

This war between USA & China may intensify further & may take ugly shape going forward, which may change World Power Equation post-COVID-19 era, he feels.

Ajay Bodke, CEO & Chief Portfolio Manager (PMS) at Prabhudas Lilladher said in the wake of US and China trade war, markets would be torn between two contrasting sentiments - "Opening up of the economy trade" versus "Global trade wars disrupting economic growth & heightened risk aversion trade".

But experts advised investors to continue to pick quality stocks as lot of them are still available at cheap valuations given their strong pedigree and attractive valuations.

"The COVID-19 hit has generated great opportunities for everyone to invest in quality business models at attractive valuations. This opportunity is being presented to investors after 12 long years and should not be missed. Investors should focus on investing in right Economy, right Sector, right Business models & rightly compliant companies," Amit Jain said.

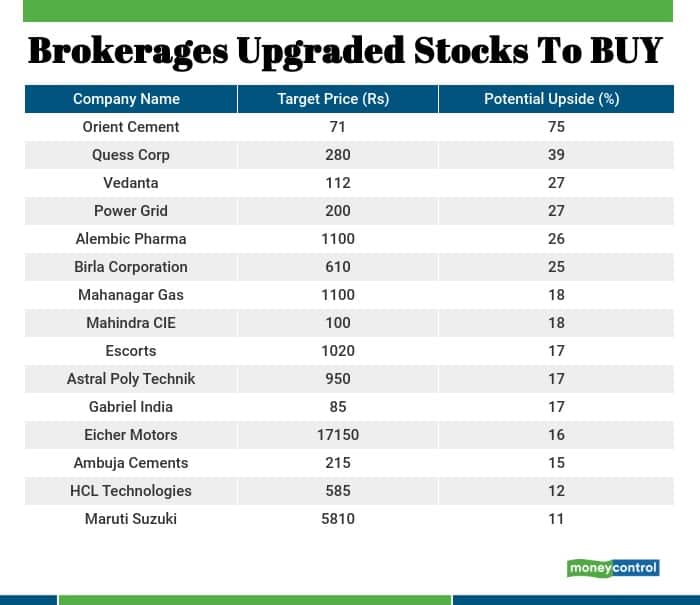

Here are top 15 stocks which got upgraded to buy by brokerage houses in the last one month, expect 11-75% returns in a year:

"Orient Cement currently trades at a replacement cost of Rs 220 crore/mt sharply lower due to the reaction to the current weakness followed by the COVID-19 pandemic which we feel is overdone. We assign replacement cost of Rs 300 crore/mt March 2022E capacities to arrive at a fair value of Rs 71/sh (earlier Rs 72/sh)," said Centrum Broking.

"The discount is still higher (replacement cost of Rs 750 crore/mt) due to risk of regional concentration. New capacity addition is on hold helping Orient Cement to shape its balance sheet better. At our target price the stocks trade at an EV/EBITDA of 5.2x FY22 earnings. We have revised our add rating and upgrade the stock to buy," it added.

Quess Corp"The stock corrected almost around 75 percent from pre-COVID-19 levels on concerns around: a) the severe impact on general staffing and collections, b) liquidity position, and c) the potential legal liabilities in outcome-based businesses, said Motilal Oswal.

"However, given a) industry concerns around manpower shortages / sharp wage increases and b) government orders forbidding lay-offs, we understand the General Staffing segment has not witnessed any material dislocation thus far," the brokerage added.

Accordingly, Motilal Oswal believes the above-mentioned concerns are exaggerated. "A material impact is unlikely going forward as the economy goes into a phased reopening and enterprises try to dodge the supply-side disruption."

Ministry of Finance recently announced that 44 central labour laws are being subsumed into four uniform codes. Reduced labour market rigidity should increase the formality of the workforce, in turn driving demand for flexi staffing. Motilal Oswal expects Quess / TeamLease / SIS Security to be the biggest long-term beneficiaries of these reforms.

In the base case, the brokerage expects 13/15 percent revenue/EPS CAGR over FY20–22E. "Using residual income approach, we arrive at a target price of Rs 280. Encouraging efforts by the new management to address certain investor concerns (e.g., capital allocation and governance) would be a key re-rating driver."

Vedanta"Vedanta has corrected over 50 percent from its 52-week high, in line with the correction in other metal stocks due to the impact of COVID-19. However, with the recovery in China in nascent stages, we believe commodities are passing through trough pricing," Emkay Global said.

The brokerage feels the pandemic will lead to a reduction in both demand and prices for most of the commodities in FY21; however, it expects a revival in FY22 and normalization of demand in FY23, driven by fiscal stimulus implemented by most of the large economies globally.

The announcement of delisting comes at cyclical lows, said Emkay which believes at a significant discount to the fair value, especially when oil, zinc, aluminum, lead all have taken a beating due to the pandemic and greenshoots of recovery have started emerging in China.

The brokerage upgraded to buy from sell with a target of Rs 112 (Rs 134 earlier) based on SoTP.

Power Grid CorporationJM Financial upgraded Power Grid to buy while maintaining target of Rs 200 and estimates given the sharp correction to prices without any changes in the stock’s core fundamentals.

"Despite a slower capex driven deceleration in profit growth (from 25 percent past to 9 percent in future), we find Power Grid earnings to be most resilient to demand slowdown. Additionally PGCIL does not have any overhangs of ESG or threat of renewables given all power (regardless of source of generation) has to be transmitted," said the brokerage.

Alembic PharmaYes Securities upgraded Alembic Pharma to a conviction buy with a revised price target of Rs 1,100, the highest on the street, as it raised multiple to 25x FY22. "We reckon market would reward stocks with visibility of revenues and profits and such companies would trade at a wide premium to sector averages. This is evident in pharma where, despite recent rally, few stocks still command a premium to sector valuation as earnings visibility remains robust."

"Alembic trades at a discount to peers like Torrent and Dr Reddy's Labs even as earnings comfort in the medium term remains high. Company is set to monetize Rs20bn worth of capex over next 3 years as filings commence from new facilities. This would drive a 20 percent CAGR surge in ex-Sartans US revenues to touch $450 million in FY24," said the brokerage.

"Moreover, domestic business has bottomed out in FY20 with our confidence based on robust performance in Q4 to end FY20 on a strong note. While we remain cognizant that gross margins would give up recent gain as Sartans opportunity recede, EBIDTA would pick up pace especially beyond FY22, as filings gain scale and approval," it added.

Birla Corporation"Birla Corporation reported a healthy Q4FY20 performance. While the ongoing expansion may increase the debt burden in the medium term, the company’s healthy asset utilisations, healthy margin profile remain key positives, which will help the company to ride this medium term challenges," said ICICI Direct which upgraded the stock to buy with a revised target price of Rs 610 per share.

Mahanagar GasMotilal Oswal upgraded Mahanagar Gas to buy considering its cheap valuations (at Rs 1,100 valuing it in line with global peers at 16x FY22E EPS). "The company trades at over 50 percent discount to IGL's P/E, P/B and EV/EBIDTA (despite enjoying the highest EBITDA/scm), offering the highest dividend yield among CGDs at around 2.5-2.8 percent. All of these attributes make Mahanagar Gas an attractive value-play in the CGD space."

Despite being categorized as CGDs, the model of operation differs significantly among the three incumbents, i.e. the industrially inclined - GUJGA (with over 75 percent of PNG-Ind volumes) and CNG inclined – Indraprastha Gas and Mahanagar (with over 75 percent of CNG volumes), said the brokerage, adding also, while Gujarat Gas has potential volume triggers from the NGT’s recent directive, IGL and Mahanagar Gas play a limited role in the same.

Mahindra CIE AutomotiveICICI Direct feels the Mahindra CIE Automotive's (MCI) current market price bakes in much of the negatives and present valuations look attractive from a medium to long term standpoint.

Accordingly, the brokerage house upgraded MCI to buy with a revised target price of Rs 100, valuing it at 5.5x CY21E EV/EBITDA (implied 10x P/E of CY21E EPS). "The company’s track record of consistent CFO and FCF generation combined with strong MNC parentage and purchase of additional 0.03 percent stake by parent group CIE lend us additional comfort in our stance," it said.

EscortsEscorts is a prominent tractor player domestically with market share in excess of 11 percent. The company’s brand of tractors is particularly strong in the northern as well as the eastern belt of India. With rural India relatively less impacted due to Covid-19, record food-grain procurement by government agencies as well as expectation of normal monsoon 2020, we expect the tractor industry to outperform the larger automobile space in FY21 with Escorts a key beneficiary, ICICI Direct feels.

On the balance sheet front, Escorts is a net cash company thereby holding surplus cash on books (around Rs 1,000 crore as of FY20) and also realises healthy return ratios matrix (RoCE at around 20 percent in FY20), thereby making a compelling case for an upgrade to buy, with a target of Rs 1,020 per share, said the brokerage house.

Astral Poly Technik'Despite a substantial volume loss witnessed in March 2020 due to nationwide lockdown, Astral Poly Technik is possibly witnessing a phase of meteoric rise in its margin trajectory. The all-time high Q4FY20 EBIDTA margin, which the management clarified was without any one-offs, is largely attributed to strong gross margin expansion in both the product segments – which were led by the company’s backward integration drive, decentralisation efforts and increasing share of VAPs," ICICI Direct said.

"Besides the rising margin trajectory, the sustained focus on strengthening the balance sheet and likelihood of the company being one of the biggest beneficiaries of market share gains in the plumbing pipe segment, Astra’s recovery in earnings could be much earlier than anticipated," said the brokerage which upgraded the stock to buy (from add) with a revised target price of Rs 950 (earlier: Rs 1,096).

Gabriel IndiaGabriel India (GIL) reported a relatively healthy set of Q4FY20 numbers. ICICI Direct expects sales, EBITDA, PAT to grow at a CAGR of -0.7 percent, 3.5 percent, -2.8 percent, respectively, over FY20P-22. The brokerage likes GIL for its domestic-oriented, debt-free, capital efficient business model (double digit return ratios) and a track record of strong CFO and FCF generation (present CFO yield around 10 percent).

GIL's 2-W slant is an added positive in present times, although reduction on OEM reliance would substantially bolster structural strength, it said. Post the recent sharp price correction, the brokerage believes GIL offers an attractive risk-reward play. Thus, it upgraded the stock to buy, valuing it at Rs 85.

Eicher MotorsEicher Motors (EML) is the undisputed leader in the domestic premium motorcycle (>250 cc) segment through its established Royal Enfield (RE) franchise that has a strong product portfolio comprising popular models such as Classic, Bullet and Himalayan.

"The stock price of EML, however, saw a sharp fall in recent months tracking expectations of further pressures to be exerted on income levels & consequent purchasing power in the COVID-19 aftermath," said ICICI Direct which feels valuations have climbed down adequately, with the company now trading at 20x FY22E EPS against average two year forward P/E multiple of around 30x over last five years.

The brokerage feels EML presents an attractive risk-reward opportunity post steep price correction; with its undiminished brand loyalty seen acting as a catalyst for an eventual recovery once pandemic effects subside. "We value EML on SOTP basis (24x P/E on FY22E RE EPS, 15x FY22E VECV EPS) to arrive at a target price of Rs 17,150 and upgrade the stock from hold to buy."

Ambuja CementsJM Financial valued Ambuja Cements on the basis of SOTP valuation (based on replacement cost), valuing the standalone business at a replacement cost of Rs 750 crore per million tonnes and arriving at a target price of Rs 215 (Rs200 earlier).

Ambuja Cements' clinker capacity addition will address its current clinker shortage issues, said the brokerage which expects savings from better operating leverage (around Rs 50 per tonne) following capacity utilisation improvement.

"The loss of incentives (from Q1CY20) will be offset by new capacity commissioning in around Q1CY21. Additionally, cost savings measures with captive coal block and new railway siding in Rajasthan will only boost/maintain earnings (even in challenging times). Healthy balance sheet (cash of Rs 9,000 crore CY21E) and debt free status only adds comfort," said JM Financial which upgraded the stock to buy from add rating earlier.

HCL TechnologiesHCL Tech reported a healthy quarter (Q4FY20) from the perspective of margin expansion, said ICICI Direct which expects the company to see near term revenue and margin pressure led by COVID-19 pandemic.

"However, in the long-term, considering opportunities in cloud consumption, cyber security, automation, app modernisation, we remain optimistic on its revenue trajectory. Additionally, easing of seasonality pressure in the products & platforms business within IBM driven by renewals would ensure growth," said the brokerage.

"In addition, HCL Tech is also looking at captives, acquisition and vendor consolidation as revenue drivers, going forward. Further, we expect various cost rationalisation measures of the company to bear fruit in FY22E. This, coupled with reasonable valuation of 11x, prompt us to upgrade the stock to buy recommendation with a target price of Rs 585 per share," it added.

Maruti SuzukiHDFC Securities upgraded Maruti Suzuki to a buy with a target of Rs 5,810 as it believes that the OEM is expected to gain market share in the current downturn, given its dominant position in the entry level/compact car segment, where the company has a market share of 65 percent (versus 51 percent overall).

"Maruti will benefit from its gasoline driven portfolio as the breakeven for diesel vehicles has further increased after the introduction of BSVI variants. As the company has a robust balance sheet, with cash reserves of around Rs 40,000 crore (around 25 percent of market cap), we expect the industry leader to withstand the downturn due to its scale and robust balance sheet," said the brokerage.

Disclaimer: The views and investment tips expressed by investment expert on Moneycontrol.com are his own and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.